Global| Feb 20 2014

Global| Feb 20 2014Europe's PMIs Bend Lower-What Else Is Bending?

Summary

There has been such ecstasy about Europe turning the corner on growth that little attention has been paid to the slow speed of that turn. If you have been watching figure skating at the Olympics, you have seen the role of speed and [...]

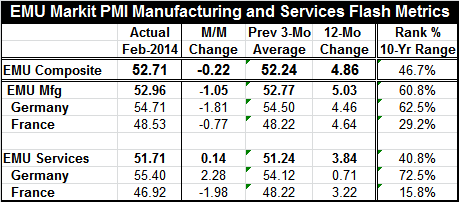

There has been such ecstasy about Europe turning the corner on growth that little attention has been paid to the slow speed of that turn. If you have been watching figure skating at the Olympics, you have seen the role of speed and momentum in assisting participants in making their next move. It's the same with the economy. Lost momentum is lost opportunity; it makes the next step more difficult. This month, we see in the PMI data, a slowing in the manufacturing and in the composite indices for the European Monetary Union (EMU). The two largest economies in the EMU, France and Germany, are both backtracking in February on manufacturing. Germany's service sector has moved ahead smartly while France's service sector has backtracked substantially. The `Union' is less than unified in the way it is progressing and its progress is slowing.

There has been such ecstasy about Europe turning the corner on growth that little attention has been paid to the slow speed of that turn. If you have been watching figure skating at the Olympics, you have seen the role of speed and momentum in assisting participants in making their next move. It's the same with the economy. Lost momentum is lost opportunity; it makes the next step more difficult. This month, we see in the PMI data, a slowing in the manufacturing and in the composite indices for the European Monetary Union (EMU). The two largest economies in the EMU, France and Germany, are both backtracking in February on manufacturing. Germany's service sector has moved ahead smartly while France's service sector has backtracked substantially. The `Union' is less than unified in the way it is progressing and its progress is slowing.

For the community as a whole, manufacturing is lower but the services sector has ticked higher.

The overall assessment continues to be one of weaknesses. The composite ranking for the EMU, at 52.71, standing below the 50th percentile of its historic queue, is at the 46.7 percentile. The Union-wide manufacturing standing is in the 60th percentile of its queue, while Union-wide services stands at a weaker 40th percentile despite its greater gain this month. It has a lot of catching up to do. Like the US, this is the jobs sector of the European economy.

For Germany and France the differences between the manufacturing and services sectors are like night and day. Germany's manufacturing sector stands in the 62nd percentile of its queue, compared to France which stands in its the 29th percentile. German services stand in the 72nd percentile of their historic queue, compared to France with services in the 15th percentile. These are the two largest economics in EMU with a substantial common border.

These differences, among the two largest countries in the Monetary Union, explain why growth in the Union is not about to rocket forward. Countries in the periphery continue to struggle while Germany, for the most part, sits in the cat-bird seat, running the largest current account surplus in the world.

Greece's trade deficit worsened last month on rising imports. Yet, it has posted a current account surplus, the first since 1948. That's 1948, as in 66 years ago. While, on the face of it, that seems impressive, the worsening trade deficit tells us that Greece has not repaired its competitiveness issues. The progress Greece has made is on the tourism side. Greece is once again attracting tourists. Its lower prices make a Greek vacation seem attractive again. Greece is making progress by renting its beaches and its climate. This is an important step for Greece but it alone will not restore Greece to solvency.

The EMU continues to be dogged by those same lingering problems of great differences in competitiveness and substantial differences in the fiscal standing of its members. Because of these things, not only are growth rates very different among monetary union members but prospects for growth are very different as well. Germany continues to give lip-service to the notion that it will shrink its huge trade surplus and become a better citizen that will provide demand for other EMU countries. But as yet that is not happening.

Several countries have crossed the Rubicon from negative growth to positive growth. While that is generally an important step, it's one being taken without a great deal of momentum. As we have seen with Olympic skaters, if you use up all you momentum with your first jump, the second jump is all the harder.

The European Central Bank continues to use the rhetoric of doing more. The International Monetary Fund is urging developed countries to keep their stimulus in place. Meanwhile, developing economies act as though all of their troubles emanate from the developed world. While the United States is dead set on a course of tapering, the IMF appears to be more concerned about the impact of this tapering on developing nations than of the impact of `not tapering' on the US economy. The fact is that you cannot have a healthy monetary system without health in the country that creates the reserve currency. This is pretty much than the lesson that is being taught by Janet Yellen.

While the Federal Reserve tells us that it's tapering is `data dependent', the `fine print' tells us that it will take a lot to take the Fed off its chosen path. Meanwhile, the US economy has been spinning out weak data. Europe's vaunted recovery is slow. China, the 800 pound `invisible' gorilla, remains un-talked about at the Fed meetings even as China's manufacturing sector is showing the second month in a row of contraction. The world economy has lost a great deal of its momentum. Monetary policy in the UK and the US has started to shift toward less stimulus. The ECB is frozen in place. Japan is still outrageously stimulative with little impact.

The Fed's forecast hopes that fiscal stimulus will drive the US economy forward. It looks for recovery overseas. It assumes that state and local governments will be largely unaffected by problems in the municipal securities markets and will spend freely in the months ahead. It ignores the slowdown in housing and vehicle sales, preferring to chalk them up to bad weather. It ignores the inventory overhang from Q4 2013 and the fact that consumer spending already has overshot income growth and that job growth may really have slowed. There are more crossed-fingers in the Fed's outlook than there are well-fitted econometric equations.

For the moment, it appears that no country is holding up his promise of growth. The IMF wants developed countries to commit to specific growth numbers to get global growth higher. The idea is going over like a lead balloon. And that's where we stand in late-February 2014.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief