Global| Jun 23 2009

Global| Jun 23 2009Europe Continues to Make a Turn Higher: Sector Results Turn Mixed in June

Summary

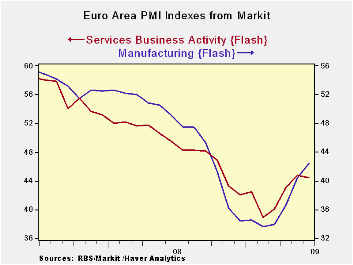

Markit PMIs composite index rises - The Euro Area FLASH PMI for MFG rose in June but that happy event was partly offset by a decline in the region’s services survey. The composite index comprised of both MFG and Services rose to 44.4, [...]

Markit PMIs composite index rises - The

Euro Area FLASH PMI for MFG rose in June but that happy event was

partly offset by a decline in the region’s services survey. The

composite index comprised of both MFG and Services rose to 44.4, its

highest reading since September of 2008. The composite index stood at

44 in May.

In Manufacturing

In Germany the country level index for MFG rose to 40.5 from

39.58 in May, its highest level since October of last year.

In France the MFG index moved up to 45.5 from 43.32 in May,

reaching its highest point since August of 2008.

The moving averages for MFG show levels are still below those

of 12 months ago but the EMU trend has been improving and the current

level of the MFG index is above the 12-mo 6-mo and 3-mo moving

averages. That is very good for momentum.

The Service Sector

The services gauge for all of EMU fell in June but remains

above the level for April having only seen backsliding for one month’s

worth of gains. The same is true of the services slippage in France and

in Germany; each lost only one month’s worth of gains. Still, in

Germany the service index stands at 44.3 in the just the 15th

percentile of its historic range. For France the index is at 47.5 and

stands in the 32nd percentile of its range. In contrast Germany’s MFG

index stands in the 31st percentile of its range, not nearly as low as

for services; France’s MFG index stands in the 47th percentile of its

range also superior to its relative reading for services. For all of

EMU the services index stands near the 25th percentile of its range

compared to a standing at the 34th percentile for MFG. The

manufacturing sector is now beginning to be more of an engine of growth

after the services sector had provided the role of support when the

economic scene was unraveling in Europe.

A note on MFG/Services comparison

Note that absolute reading for services is superior to that

for MFG but that for MFG the current reading is at a higher percentile

in its range. The percentile reading is a better gauge to use to

compare one index to another since MFG indices span a broader range of

values and since the Services index has higher reading on average. The

services reading average nearly FOUR points higher than the MFG

readings. So on several bases the MFG index now is relatively stronger

than services despite the higher absolute monthly reading for services.

Over comparable periods the standard deviation of the MFG index is 5.41

compared to 4.72 for services making the MFG sector some 14% more

variable than services and 20% more volatile relative to its mean. The

service index is relatively sluggish compared to the MFG index, as we

well know. Not surprising then that MFG is the best DIRECTIONAL index.

Fortunately it is moving UP now.

Perspective

Manufacturing is now on the strongest rising gradients for

EMU. The service sector index has paused and lost some momentum. Still

the overall picture and trend remains positive.

Another sign of progress this morning came from the Belgian

National Bank index which trimmed its negative reading to -23.6 in June

from -27.6 in May. For that index it is the best reading since November

2008.

In terms of these index readings, we see in the Markit PMIs

the best MFG and Services (for services based on the May reading)

readings since August – October of last year and in the Belgian series

the best reading since November. On balance it is looking like a

reasonably well balanced rebound is taking place across the Zone in

these countries and across their various sectors, at least as judged by

the measures presented here. Of course, all the respective measures

still point to continuing losses. But these indices speak to the fact

that the speed of the loss has been cut sharply from the lows showing

that the pace of decline is back to the pace last seen in early Q4 or

late Q3 of 2008.

The MFG ands Services PMIs each were last above 50 in May of

2008. The Belgian bank index was last positive in May of 2008 as well.

How soon we get back there depends on quickly this incipient recovery

traces its own steps. For now it is on the right path and the pace of

recovery is a good one, service sector (perhaps) excepted.

| FLASH Readings | ||

|---|---|---|

| Markit PMIs for the Euro Area | ||

| MFG | Services | |

| Jun-09 | 42.37 | 44.49 |

| May-09 | 40.68 | 44.82 |

| Apr-09 | 36.83 | 43.76 |

| Mar-09 | 33.93 | 40.95 |

| Averages | ||

| 3-Mo | 37.15 | 44.10 |

| 6-Mo | 35.55 | 42.29 |

| 12-Mo | 39.92 | 44.22 |

| 127-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| % Range | 32.8% | 22.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief