Global| Mar 14 2013

Global| Mar 14 2013EURO REALITY: Jobs Situation Worsens in EMU

Summary

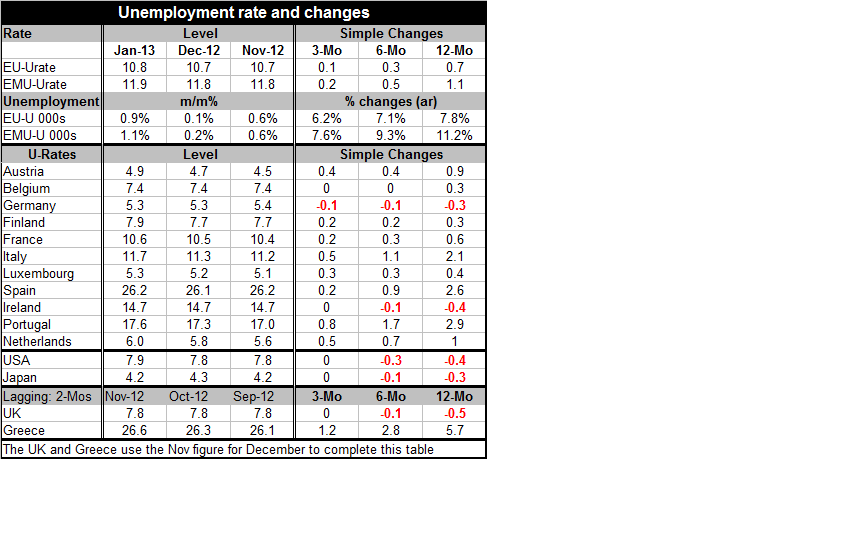

European employment trends show that employment in the Zone is at a seven year low. Even with stagnant population growth this is not a good development. Over the last year the unemployment rate for the Zone has gone up by 0.7 [...]

European employment trends show that employment in the Zone is at a seven year low. Even with stagnant population growth this is not a good development. Over the last year the unemployment rate for the Zone has gone up by 0.7 percentage points while the rate for the US has fallen by 0.4 percentage points and Germany's rate has fallen by 0.3 percentage points.

European employment trends show that employment in the Zone is at a seven year low. Even with stagnant population growth this is not a good development. Over the last year the unemployment rate for the Zone has gone up by 0.7 percentage points while the rate for the US has fallen by 0.4 percentage points and Germany's rate has fallen by 0.3 percentage points.

Overnight in Bulgaria one austerity dissident lit himself on fire in front of the Bulgarian parliament building in Sofia. It is the fourth time in the past month self-immolation has been used as a protest method in Bulgaria.

The Euro-politics (Euro, as in European) of control are breaking down. This sort of protest is quite a serious thing.

In the UK David Cameron has tried to argue that his program of higher taxes and spending cuts do not have lower growth consequences. He was corrected by his own forecasting team in public. In Italy the political maestro Silvio Berlusconi has rehabilitated himself by championing opposition to austerity and by lampooning the technocrat government that brought it. The upstart five-star political party too has gained on an anti-austerity and secessionist platform. In France President Hollande's economic plan has gone badly off-track and has upset many of his campaign promises. He has suffered one of the sharpest declines in popularity ever of a new French leader. As a result he has swerved France from its deficit cutting target but that has not brought much relief, or restored his popularity, but it has incurred the wrath of German's for loosening its commitment at a time Germany has been looking to harden the core of the euro. As for Germany is has just enacted spending cuts and is aiming at a balanced budget. After a dozen years of EMU, does any of this sound like unity?

The problem with austerity as a policy is that there is confusion about whether it is a goal or tool. To conservatives, lower deficits per se may be the target and goal and for them achieving that result may be enough. But to elected officials, to the labor force and to businesses, results matter.

But the only result that Europe is getting from austerity is less growth and more unemployment. Inflation performance has been OK but not terrific. Inflation is 2.2% over the past year even with all that terrible growth. Austerity will not cure cancer; it might not cure the huge competiveness divide that has erupted in Europe since the EMU was formed and since the single currency was launched. Undeniable huge differences in national inflation rates not compensated by productivity changes mark these early years of EMU. The ECB had to hit an inflation target that was output-weighted which meant that German inflation mattered most. Inflation is some of the smaller countries hardly mattered- at least not to the ECB. There were no regional inflation obligations or mechanisms to deal with those differences. As a result, we come to blame local fiscal policy for the differences in national inflation rates within EMU. But the problem is broader than that.

Had the ECB been shooting at an inflation target that was one-country one-weight the union might have worried more about high inflation in its the periphery. Still, that focus would only lift 'average' EMU inflation to 2.3% from 2.1% since its inception using the inflation rates only of the first 12 members.

What is clear to me is that Europe was not well-enough integrated when the currency union was formed. Theoretically that is not a problem. But practically it is. Because once formed the 'union' was not a whole-hog free-trade area. Many laws. procedures and codes eventually were harmonized but a number of rigidities remained. National fiefdoms were protected. As a result the forces of competition could not flood the Zone and even-out that which was uneven. Instead, pockets of very different sorts of economic behavior developed and became codified. This was ignored even when tipped off by structurally higher rates of inflation INSIDE THE ZONE. Ignoring them was the ultimate denial for Europe which has from the start wanted to be 'One' but has wanted to retain national identities too. This sort of schizophrenia, paired with denial, at the policy level can only lead to trouble... And it has.

Whether policy failed (as popular legend would have it) because of lack of a binding fiscal commitment or because of lack of a broader commitment (my preference) does matter, however. Diagnosis speaks to solution. If you have a bicycle tire with two holes in it and you only fix one, you will not be satisfied with the result.

Europe's integration at first moved slowly and carefully using a trial exchange rate system (the snake; the snake in the tunnel, etc) before it locked exchange rates together for good. But Europe was not so careful to harmonized laws before the rate lock. Competition in the Zone has been uneven and it has been more uneven than what you could explain by language and cultural differences. Europe did not harmonize 'competition' to smooth out these bumps. They meant to protect (and therefore 'preserve') the less competitive -and they did, but then they never stopped.

Still cultural and social policy differences run deep. It is very hard to integrate Germany, a country that is now pushing for a balanced budget, in with others like France, that is trying to postpone hitting a much higher deficit to GDP target. There is no denying that the appetite for fiscal redress will be directly proportional to the state of GDP growth. Even so across nations some may not -even in good times -want to redress much. But when economic performance diverges the taste for austerity will diverge too. With the fiscal crisis and recession, the standard deviation of growth within the community is up by about 50%. And of course it is among the weakest and most divergent countries where austerity is being applied most aggressively-and is making things even worse. But, to what end? TO WHAT END?

Increasingly this is the problem with austerity. If 'the people' could be told that after 'X' years of this policy 'everything will be fine,' 'you will have jobs and your life will resume.' Then there might be support for such a policy. But no one can make that promise. What is clear is in fact the OPPOSITE! Countries had used the euro-scheme to live beyond their means and they are not going back there- to those living standards- maybe not ever. So here's the plan: tighten up your belt AND get used to it! It's not very alluring is it?

The need to put the toothpaste back in the tube means that wages must be cut in real terms in many nations and that will reverberate though 'factor prices.' One thing that means is that property values will have to fall to accommodate lower incomes. Other shifts in relative and absolute prices will be needed too. This is a complicated, devastating, wrenching process. Austerity is a blunt tool to try and get this process in motion but it is very painful and only works through the fiscal side and does not bring a quick remedy to private sector excesses that have developed. Those problems which are now the biggest impediments to prosperity will be attacked by the second-round effects of austerity, not the primary effects. That may mean that the primary effects of budget squeezing may have to be even more austere in order to do their job.

Crushing fiscal austerity can do this by bringing deflation for which there is now a euphemism called 'internal devaluation.' They call it this because everyone knows how bad deflation is, so they give it a new name. But these policies do not impact the problems that have developed in a clear way, the problem of lost competiveness. Austerity is a blunt tool.

Some countries, like Greece, have come to have almost no manufacturing. Indeed, one argument against Greece leaving the euro and refloating the Drachma is that it has no manufacturing sector to benefit from enhanced competiveness. But if that is the argument then how does Greece survive INSIDE the euro-system? To see a remedy you have to see a changed future. IF Greece were to leave the euro and to devalue it would then become cheaper to invest in Greece. In exchange rate adjusted terms Greek wages would be lower. Presumably these factors would attract business and yes manufacturing. But it's not prices alone it is also the nature of the work force. And Greece is still a very socialist country. So in the end when we look at the euro Zone and when these factors cause some to argue its nations can't succeed outside the Zone, how do they think they will ever succeed inside it? What will change and what will force change?

Either the eurozone needs to implement the tough love of ejection from the Zone to get its various members on the same page as far as competiveness levels and work ethics are concerned, or the Zone, if it continues to patch itself together, to quell the Italian uprising, to mollify the French, will need a system of transfer payments to support its ongoing inefficiencies. It is far from clear to me that the 'rich' countries will want to pay for this. It not clear that even if they agreed 'for a time' to limited transfer payments mixed with ongoing austerity that such a plan would create a Zone that could become stable. What austerity has shown is that when push comes to shove Europe does not band together in times of adversity.

Germany is not trying to 'feel Spain's pain' or to admit the role its banks played in financing the excesses in the Zone. Germany is blind to its role. It had offered up the 'Japanese lunch box plan' for fiscal policy where there would be no transfers and each country would have to hits its own targets and maintain specified deficit-to-GDP ratios or pay fines. Germany has, as other nations have struggled, clamped down even harder on its own deficits. Germany is making it harder for the other members of EMU to keep pace with it. Germany is not meeting them half way. And until or unless Europeans think more like Europeans instead of like members of their own individual countries these problems not only will not get fixed, they WILL GET WORSE.

And it is getting worse, slowly. That is Euro-reality.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief