Global| Sep 16 2016

Global| Sep 16 2016Euro Labor Costs Are Subdued

Summary

Wage inflation is mostly subdued across the euro area. Data through the second quarter show that EMU hourly wage costs are up by only 1% over 12 months and that wage growth is at a slightly slower pace than that over three months [...]

Wage inflation is mostly subdued across the euro area. Data through the second quarter show that EMU hourly wage costs are up by only 1% over 12 months and that wage growth is at a slightly slower pace than that over three months (annualized).

Wage inflation is mostly subdued across the euro area. Data through the second quarter show that EMU hourly wage costs are up by only 1% over 12 months and that wage growth is at a slightly slower pace than that over three months (annualized).

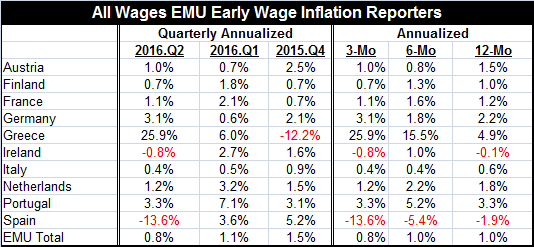

As always, there are country differences and these can become issues if they persist over time or are large and especially if they are not compensated for by productivity. Greece has witnessed some huge wage increases over the last two quarters and it has a substantially higher gain in place than other reporters in the table over 12 months as well. Greece's 4.9% gain tops the list for 12-month gains. But Portugal also has a gain of 3.3% and Germany is relatively high with a gain of 2.2%. Only Spain and Ireland have year-over-year drops in labor costs; Italy has a sub 1% rise.

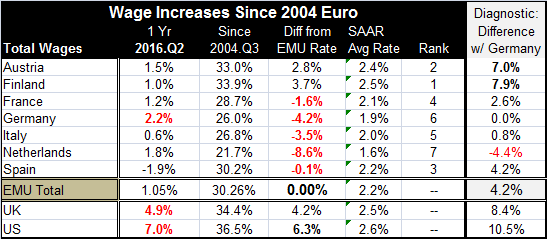

We have labor cost indexes back to 2004 for a group of seven EMU members plus the U.K. and the U.S. Over this period, the Dutch have the smallest aggregate increase in labor costs, followed by Germany, Italy and France, in that order. Finland, Austria and Spain show the relatively largest aggregate gains in that rank order.

Still only Austria and Finland have very different aggregate wage gains compared with Germany. Spain's hourly labor costs have grown by only 4.2% more than Germany's over the whole period and the Netherlands' gains have been of 4.4% less. For the most part, it appears that wage costs have been kept in better alignment than consumer prices. This is important for the sake of preserving competiveness parity across the euro area with its fixed exchange rate. If wage levels get `substantially' out of line, pushing them back into line is a painful process. It is also a process that does not work very elegantly has we have seen in Greece, Italy and Spain where various sorts of austerity programs have been meted out.

Both the U.K. and the U.S. would count as high (the very highest) wage increase countries were they in the euro area. But since they are not and since each has a flexible exchange rate 2.5% to 2.6%, average gains do not impair wage costs in the international area to any significant degree. As far as competiveness goes, there is still the issue of productivity to be taken into account in any event. Even within the EMU, there is some scope for wages to increase at different speeds if productivity differences can offset the increases.

The chart of wage costs for the EMU shows that while there have been some cycles to wage costs since the financial crisis the general trend has continued to point lower. Inflation has stayed low and wages have been contained. Low wage gains support moderate inflation and moderate inflation supports small wage gains. Europe's labor costs are not an issue from the standing point of being an inflation threat. On the other hand, since the ECB is trying to reflate the price level, there is no hint that wages are set to aid in that direction as wage gains have continued to cycle lower, not higher.

Obviously, the issue of wages is an EMU-wide issue along with inflation and fiscal deficits and regulation and so on. With the U.K. opting to leave the EU, that region is having an identity crisis. EU members recognize that there are now some very important divisions on some key issues and that these differences in policy are affecting the region's ability to govern itself. The EU provides a core for policy harmonization which also underlies the EMU region. There what is being called an `informal European summit' underway to discuss the future of the EU. The summit is informal because if a formal one were convened the U.K., which is still an EU member despite its plan to leave, would have to be included. Europe is beginning the task of trying to plan for its future and to deal with some of the larger policy divisions that have arisen including the need to deal with Brexit.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief