Global| Jul 29 2016

Global| Jul 29 2016Euro Area Unemployment Rates Steady. Down-trend Remains in Place

Summary

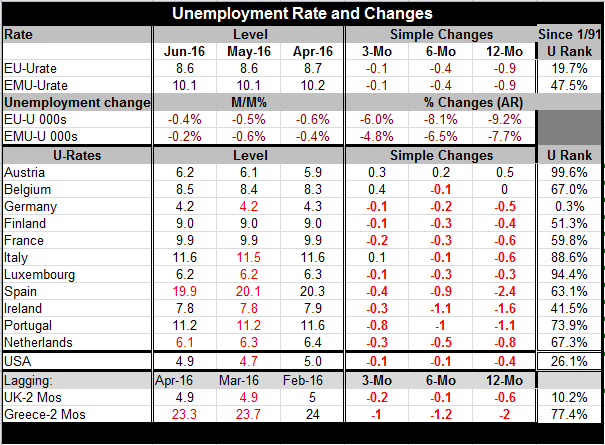

The EU and EMU rates of unemployment were steady in June. Among the earliest EMU members unemployment fell in June in only two of 11 counties, Spain and The Netherlands. The rate also fell in Greece for April which is the most topical [...]

The EU and EMU rates of unemployment were steady in June. Among the earliest EMU members unemployment fell in June in only two of 11 counties, Spain and The Netherlands. The rate also fell in Greece for April which is the most topical observation for Greece.

Despite the hiatus in the unemployment rate dropping in June, rates of unemployment are still falling on a broad front over longer spans of time: three months, six-months and twelve-months.

Still there remains a chasm of difference between Germany's unemployment rate and everyone else's. Germany's rate of unemployment has stayed at a post-reunification low. Apart from Germany, only Ireland has a rate of unemployment that is below its historic median back to 1991. However, Finland is close to its 50% queue standing at the 51.3 percentile mark.

Levels of unemployment are falling for EU and for EMU but the annualized pace of the drop has been slowing. For Luxembourg, Italy and Austria rates of unemployment hover in the top 12% of all rates they have experienced historically since early 1991.For these three countries recovery continues to elude the labor market. Belgium and Austria show signs of some recovery reversal. Belgium has inflation rising and has its rate of unemployment up by four-tenths of a percentage point over three-months. For Austria the unemployment rate is up by three-tenths of a percentage point over three-months and by five-tenths over 12-months.

Growth The early read on EMU GDP has it rising at a 1.2% annualized pace in Q2 and by 1.6% Year-on-year. Both of those rates represent a reduction from Q1 when GDP rose at a 2.2% pace in the quarter and by 1.7% Year-over-year. France's growth rate was reported as flat but the act of compounding its quarterly rate produces a slight contraction in Q2 and a year-on-year pace of just 1.4%. France's PMI data have been floating barely North and sometimes South of the 50 diffusion level for some time. A decline in quarterly French GDP is not surprising in that context.

Inflation The July EMU inflation reading also is on offer today and it shows inflation up by 0.1% Year-on-year with core inflation up by 0.8% Year-on-year. Headline inflation has turned positive again. And three-month compounded rates of inflation are above 2% for the headline but not for the Core. The ECB tends to focus on the year-over-year headline rate with the objective of keeping it just below 2%. Inflation remains well short of that objective, but there is some discernable up-creep.

The global economy news round-up Economic reports remain somewhat confused or in flux. In the U.S. GDP disappointed as corporate investment weakness blunted a sharp pick-up by consumers to hold the Q2 GDP gain near 4% instead of north of 2% as had been expected. In Japan a whole barrage of data showed weaker retail sales, weaker household consumption, dropping prices, a slide in housing and a drop in auto production. There was a pickup in overall industrial production to balance all that negative news. But in the biggest news, the BoJ failed to impress markets with its decision last night to step-up its ETF purchases deciding neither to deepen its negative rate objective nor to resort to ‘helicopter' money. It did double its lending program.

The Outlook Globally economic conditions remain mixed. It is hard to argue whether economic growth rates are really changing speeds or not. Governments and central banks continue to try to take action but nothing has impressed markets. The outlook remains guarded. In the U.S., the Fed is playing it day by day. The IMF has recently reduced its outlook slightly. The aftermath of Brexit overhangs Europe. In its meeting today the BOJ has cut back its expectations for inflation and for growth despite its new policy actions. Global conditions remain in flux with more of the risk seeming to fall on the down-side.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief