Global| Jan 09 2018

Global| Jan 09 2018Euro Area Unemployment: Lowest Since 2009

Summary

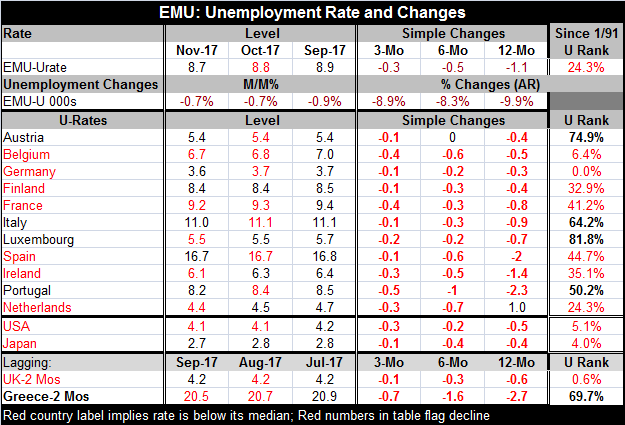

Among the original 11 EMU member countries, only four countries: Austria, Italy, Portugal and Luxembourg have unemployment rates above their median values back to January 1991. Belgium and Germany have exceptionally low rates (vis-a- [...]

Among the original 11 EMU member countries, only four countries: Austria, Italy, Portugal and Luxembourg have unemployment rates above their median values back to January 1991.

Among the original 11 EMU member countries, only four countries: Austria, Italy, Portugal and Luxembourg have unemployment rates above their median values back to January 1991.

Belgium and Germany have exceptionally low rates (vis-a-vis their own individual historic experiences). Germany has a new low in unemployment since reunification. Belgium has a rate that has been this low or lower only 6.4% of the time. The Dutch rate has been lower only 24% of the time. Finland's rate has been lower less one third of the time; in Ireland it has been lower about 35% of the time.

There is considerable progress in the reducing levels of unemployment and in the breadth of unemployment improvement. And improvement is ongoing...This is not being driven by just the large countries.

Over three months, all of the original EMU members show a drop in their respective unemployment rates. Over six months, all countries show drops except Austria whose rate is unchanged. Over 12 months, all show drops except the Netherlands which has its rate higher by one percentage point. On lagged data, the U.K. (an EU country) and Greece show progress is step with these declines. The U.K. has an extremely low unemployment rate. Greece has rate deeply into double digits above the 20% mark; still, it is falling.

Because of the weight of Germany and because of its outstanding performance, the ranking for all of the EMU is slightly exaggerated as it is lower only 24.3% of the time. If instead of using employment weights we looked at the average across countries without regard to size, the EMU measure rises sharply to 47.8% (with Greece) or to 45.5% (without Greece).

The dispersion across the levels of the unemployment rates among the original members is currently at 3.7 percentage points, just below its full period average of 4.0 (back to 1991). From 1998 thorough late-2007, there was a period in which 'super harmonization' took place and the dispersion among unemployment rates of member countries fell to a low of 1.8 percentage points. The all-time greatest dispersion of 6.4 percentage points came in the pit of the financial crisis. Calculations of the norm are distorted by the events of the financial crisis as well as by the excesses in the super harmonization period when growth was being bought in some countries by unsustainable fiscal policies. Still, the current dispersion indicates a degree of harmonization that is better than anything seen before 1998, in the first eight years of integration. On the other hand, evidence also seems to show that the movement to even greater harmony is slowing or may have stopped.

There have been three separate and important trends afoot. Unemployment has been falling; it has been falling broadly; and harmonization among member states has been improving.

Implications for policy In some sense, the ECB is making policy based on the 24.3 percentile standing of the unemployment rate for the whole of the EMU. In another sense, the politics among EMU members, who after all represent countries, are probably a bit more affected by the 45.6 percentile standing of the broader community viewed as a collection of sovereign states. And the EMU has grown even broader in recent years adding a number of members on top of the original ones. There are many more countries whose central banks have representatives at the ECB policy table - a table that is looking increasingly crowded. But those two ranks are illustrative of the sorts of dilemmas the ECB faces as it weighs and balances policy: its overall macroeconomic situation and the circumstances of individual members.

German thinking, methods, and location dominated the ECB until the financial crisis. ECB President Mario Draghi has wrestled some moderation and breadth back from the single-minded Germans as the policy environment simply made it clear the German approach to monetary policy for a while made absolutely no sense. At least the ECB had to consider the risk of inflation that was too low as well as too high. Until the financial crisis, Germans viewed inflation that was too low about the same as some people viewed being 'too rich' or 'too thin.' But as economic conditions 'normalize,' the ECB's mandate remains very much one with a single mandate on inflation. Of course, this is almost always open to some interpretation even though the ECB's target and horizon are quite clear. Some will always want to be more forward-looking than others; if there is overshooting, some will want to attack that more aggressively than others. For now Germany is the country in the EMU with the lowest unemployment rate, the least economic slack and one of the most pressing 'inflation problems' despite the fact that for all of the EMU there is no inflation problem. As growth begins to return, we can expect these realities to bring more disharmonies to policy especially in the EMU. Mr. Draghi's eight-year term will end late in 2019. Draghi is not crippled by this. And for 2018, we should expect that if he is undercut it will be by economic events not by some erosion of power owing to the end of his term closing in.

Inflation

As of November, Belgium (a low unemployment rate country) had the highest year-on-year inflation rate at 2.1% followed by Luxembourg at 2.0%. Germany was tied for the next slot with Spain and Portugal all with HICPs rising by 1.8% over 12 months. This not the sort of 'company' Germany is accustomed to. As of November, the low inflation countries among original members are Ireland (0.5%), Finland (0.9%) and Italy (1.1%). Back to early-1996, the November inflation variation across the original EMU members (plus Greece) has the third lowest standard deviation among the year-on-year HICPs. So while unemployment differences remain and may well be indicators of structural features of the various economies, these features have not prevented inflation rates from converging to an unprecedented extent.

Until 2003, Germany persistently ranked as the lowest inflation country in the EMU. After 2003, there was a shift and the German rank began to slip. From February 1996 until December 2003, Germany's median rank among fellow EMU members was 11th out of 11. Then until September 2012, that rank fell to 9th lowest. Since then from October 2012 to date, the German median rank is five out of eleven. Germany has tended to rank as the fifth HIGHEST inflation country in the EMU (among the group of the first 11 members) since the period of the financial crisis. This was period of very low inflation and it was a period in which some EMU countries saw their price levels decline as they ran negative rates of inflation. But Germany's recent median rank is 5. Its median rank over the past 2 months since conditions have been more stable has slipped back to sixth. It is not clear to me that German policymakers are going to be all that happy with these developments. Germany has used a strategy of being the low inflation country in the EMU to cement its economic leadership and further its competitiveness. It will be interesting to watch Germany and see how things shake out and to see how German national data dove-tail or clash with EMU-wide data trends.

Historically, Germany has been able to remain on top by running an inflation rate even lower than the EMU target. Since the EMU's formation German inflation has averaged 1.5% per year while EMU inflation has averaged 1.75%. Portugal has averaged 2% while Spain has averaged 2.2%. German inflation is currently tied with Spain and Portugal. These are strange bedfellows for Germans.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief