Global| Jun 15 2020

Global| Jun 15 2020Euro Area Trade Surplus Nearly Evaporates in a Single Month

Summary

The EMU trade situation saw an extremely sharp deterioration in its surplus in April. The surplus dropped from €25.5bln to €1.2bln in one month! It is by far the sharpest monthly setback on data back to January 1999. EMU experienced [...]

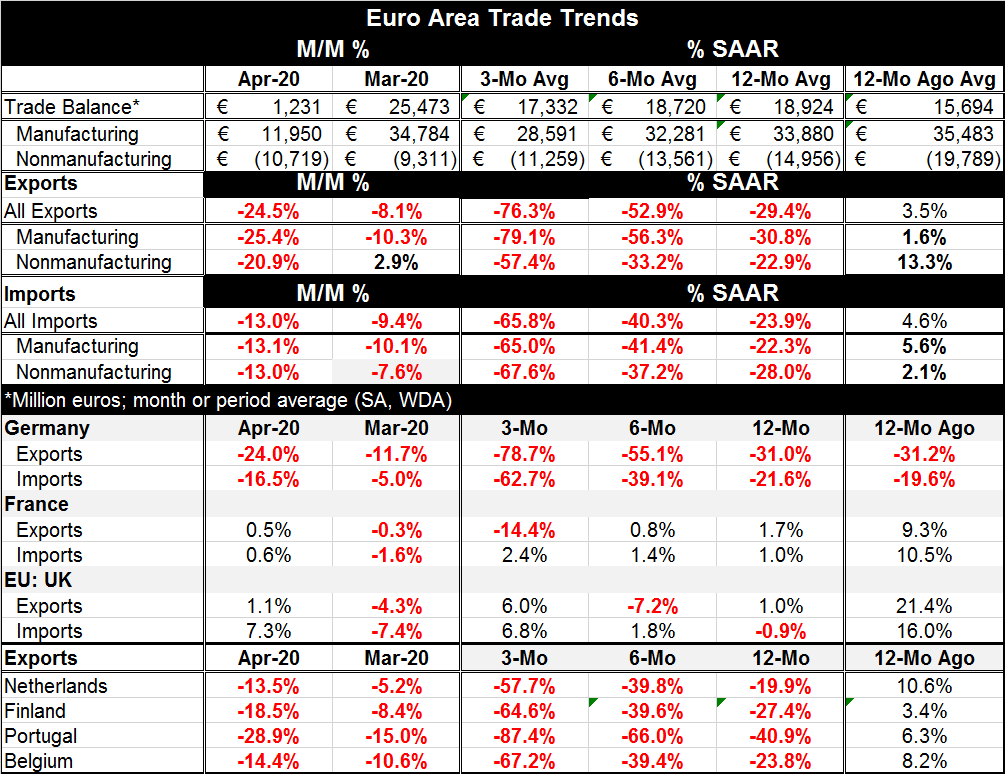

The EMU trade situation saw an extremely sharp deterioration in its surplus in April. The surplus dropped from €25.5bln to €1.2bln in one month! It is by far the sharpest monthly setback on data back to January 1999.

The EMU trade situation saw an extremely sharp deterioration in its surplus in April. The surplus dropped from €25.5bln to €1.2bln in one month! It is by far the sharpest monthly setback on data back to January 1999.

EMU experienced sharp reversals in both manufacturing and nonmanufacturing exports in April. Meanwhile imports of both manufactured and nonmanufactured goods fell sharply but fell by much less than did exports. The drop in exports exceeds the drop in imports over three months, over six months and over 12 months.

The EMU surplus has not been this small since it was in deficit in October 2011.Trade flow growth has slowed very sharply.

The Baltic dry goods freight volume index has been working its way higher.

The Baltic dry goods freight volume index has been working its way higher.

Global trade has slowed sharply putting the hurt to Germany and to the EMU surplus. However, the Baltic Dry index of freight volumes has been up for seven days in a row. And while some of that was still climbing out of a hole, it shows some promise as an indicator of improving international freight volume (although it is still broadly weak).

The table has some specifics for industrial country data of Europe. Germany, the Netherlands, Finland, Portugal and Belgium all show extreme weakness in exports in April and over the preceding horizons. The strongest monthly export growth is the Dutch figure of -13.5% with the weakest as Portugal's -28.9%. Over 12 months the export declines range from declines of -19.9% in the Netherlands to -40.9% in Portugal.

France and the U.K. seem to be on another planet. Both shows small export increases in April and import increase to go with them. Neither mirrors the draconian pattern of negative growth rates seen in the other countries on longer horizons.

On balance, the trade picture is poor. European trends are under pressure. The euro-trade data are not comforting at all. But the Baltic Dry index and its revival offers some hope that trade volumes may be bottoming or near bottoming.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief