Global| May 17 2016

Global| May 17 2016Euro Area Trade Flows Implode! Egad!

Summary

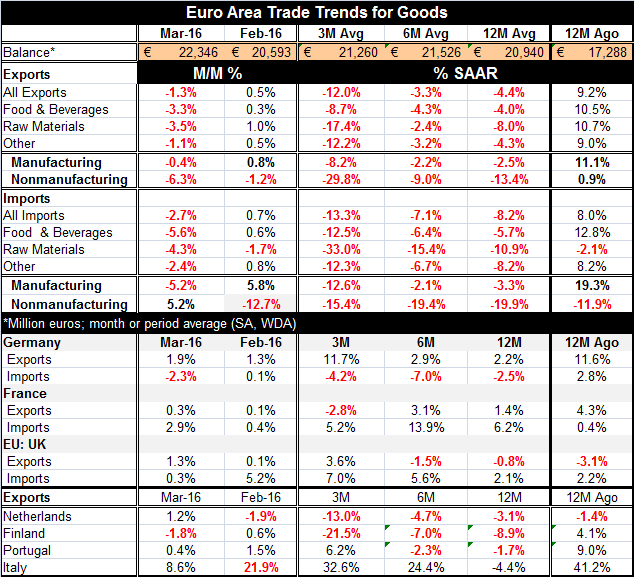

Are EMU exports and imports the brothers Grim? It's a grim picture that trade has painted in this month's EMU trade report. Yes, for the EMU, the result is `positive' as the trade surplus is getting even larger. At 22.3 billion euros, [...]

Are EMU exports and imports the brothers Grim?

Are EMU exports and imports the brothers Grim?

It's a grim picture that trade has painted in this month's EMU trade report. Yes, for the EMU, the result is `positive' as the trade surplus is getting even larger. At 22.3 billion euros, the surplus was last larger in December 2015 and in a handful of months back to 2014. But it is large, and bigger than a bread box.

Exports speak of global weakness

EMU exports are falling across all commodity classifications in March, over three-months, six-months and 12-months. Manufacturing exports are falling and nonmanufacturing exports are falling. When trade flows are so widely imploding, it's a bad sign about the state of demand globally. And since export and import flows generally are stronger than GDP growth, the message is extra ominous.

Imports speak of weak EMU domestic demand

On the import side, all the same statements hold again with only one exception. Nonmanufacturing imports did pick up month-to-month in March after a 12.7% decline in February. But after that, there is weakness everywhere else in March and well as across all the key horizons as flows implode on a very broad horizon with astounding depth. The import weakness is for manufacturing as well as nonmanufacturing products. There is no silver lining unless you want to say that the improved trade balance is the silver lining. Weak imports speak to weak domestic demand. And this import weakness does not speak to any sort of economic revival in the EMU. Meanwhile, in German there are court filings to try to stop the ECB from taking steps to revive the EMU-region's economy. What a shameful display of self interest in Europe's most solid economy.

Country by country, there are some bright spots

We provide some information for early reporting key countries in Europe and there we see some sporadic growth for exports and imports as German exports look strong in this environment while France and the U.K. are more uneven. Yet, German imports are unequivocally weak, adding nothing to global demand but both French and U.K. imports are showing either strength or acceleration.

More weakness

For a second group, we look at export flows alone: The Netherlands, Finland, Portugal and Italy. The Dutch and Finns show weak and decelerating exports with flows contracting. Portugal shows export declines interrupted by a gain over three-months. Only Italy shows export flows turning more strongly positive over six-months and twelve-months. But Italy reported a sharp drop in its imports in March to go along with it.

A message from the universe? Message in a trade flow?

On balance, we have trade flows with such weakness and on such a broad scale that it should raise eyebrows. Remember that the euro is still quite weak and this region should be competitive at these exchange rates. The OECD leading index for the EMU has clung to values above 100 for this region which has scored as one of the stronger regions among the various global metrics of the OECD. Yet, there continues to be profligate weakness in EMU trade flows and trends. In a world where central banks have been putting the electric cattle prod repeatedly to lethargic economies, how could this be? Has demand gone dead? How can global demand still be so weak after all this prodding? Should we scale back expectations even further? The trade flows leave us little in the way of a positive reality to give grip to.

The chart shows some but not much lift in the Baltic dry good index, a trade barometer.

The chart shows some but not much lift in the Baltic dry good index, a trade barometer.

What happens in Las Vegas Stays in Las Vegas but not so in D.C.

As these weak numbers are issued, the Fed in the U.S. is apparently more -not less (!)- conflicted with a number of very vocal members saying that based on what `they see' the time is ripe for a U.S. rate hike. Can you feel the international repercussions from such a move? Are the tectonic plates already shaking? It may be that what happens in Las Vegas stays in Las Vegas, but what happens at the Fed spreads like a wildfire in Canada and does so globally.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief