Global| Aug 02 2016

Global| Aug 02 2016Euro Area: The Worm Turns on PPI Inflation With a Big `But'...Oil

Summary

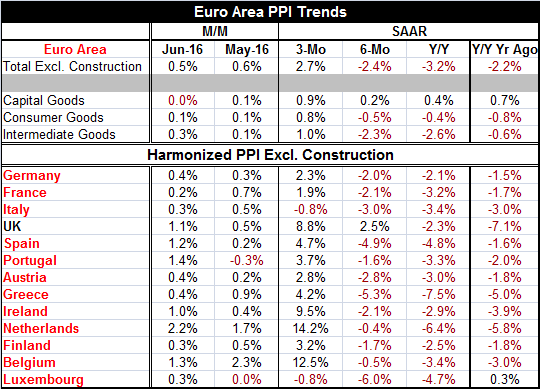

PPI inflation is decidedly higher in the EMU. While its gain in June is less than its monthly gain in May, the three-month pace is at 2.7% compared to -2.4% over six months and -3.2% over 12 months. Sector inflation is rising for [...]

PPI inflation is decidedly higher in the EMU. While its gain in June is less than its monthly gain in May, the three-month pace is at 2.7% compared to -2.4% over six months and -3.2% over 12 months. Sector inflation is rising for capital goods, consumer goods and intermediate goods over three months with positive monthly gains across the board.

PPI inflation is decidedly higher in the EMU. While its gain in June is less than its monthly gain in May, the three-month pace is at 2.7% compared to -2.4% over six months and -3.2% over 12 months. Sector inflation is rising for capital goods, consumer goods and intermediate goods over three months with positive monthly gains across the board.

So PPI inflation is rising, but...the `BUT' in the headline is over energy. While energy costs had been on the rise contributing to this uptrend, they have recently done a sharp about-face and oil prices are now down 20% from their peak with excesses galore for refined products. The question is, therefore, whether this rebound in the PPI will stick when these more recent lower oil prices begin to filter through. Of course, oil prices can't stay down forever. What this rebound does demonstrate is that when oil prices rise there is some push to PPI inflation waiting in the wings. But just how much is there remains a question.

So many countries with the same general trends

The table focuses on all the original EMU members plus Greece and the U.K. For each one, PPI inflation is positive in June and accelerating over three months. Except for Spain and Luxembourg, inflation also is increasing over six months compared to 12 months. For all in the table, three-month inflation is higher than 12-month inflation. The 12-month inflation is still showing negative numbers across the board and over six-month prices are falling (but by less hence the broad acceleration of inflation over six months) everywhere, except in the U.K.

Despite common forces, there are some very different results

It is rare that you can make so many sweeping generalities about price trends even for a group of countries in the same currency zone. But what we see is how macro price pressures are having the same general impact across the board. Of course, there are still `local' differences as the Greek PPI is down by 7.5% over 12 months compared to Germany where prices are down by just 2.1% over 12 months. Actually intra-EMU inflation SIMILARITY on the PPI gauge has been on the decline since mid-2013 when the differences among national rates of inflation in the EMU were at their low. This up-creep may be another sign that the crisis is passing and that a sense of commonality in the EMU is fading. Countries may once again be beginning to feel more disparate national tensions on their domestic price levels.

Europe is still only the sum of different moving parts

We can talk about European heterogeneity all day. But differences persist. There has not been enough harmonization to allow pricing forces to sweep evenly across the EMU. When a common shock like oil prices emerges, there is enough similarly that it washes over most countries with a similar effect, but when that passes, they revert to their national differences. Spain has just reported its lowest number of unemployed in seven years, but it still has the second highest unemployment rate in the EMU. While Spain's unemployment rate has been higher 63% of the time since 1991, Germany's rate has never been lower since German reunification. These are powerfully different structural conditions. And then there are more topical sagas such as the state of the Italian banking sector.

Heterogeneity may become an issue yet

Heterogeneity is about to become a big issue in the EMU again, especially with the U.K. having executed its `jail-break' from the EU. Other countries may start to think that there is more to be gotten from escape than from continued membership. And we know that when that question is put to a popular vote, there is more dissention than what European lawmakers try to pretend. It is hard to know how many Europeans really stand behind the notion of European unity, but we do know that the cost of disassociation will be much higher for any EMU member that decides it wants `out.'

The PPI pick-up: what it does and does not mean

The pick-up in the PPI, even if it sticks, does not necessarily spell the end of inflation tranquility in the EMU. Policy in the EMU is made off of consumer prices and the HICP measure. And while the HCIP and the PPIs do follow the same broad trends, their link is not tight. In 2009 PPI prices fell much more sharply and deeply but recovered more quickly and the HICP gauge barely got to zero and broke through. This time, with a shallower but more protracted fall in the PPI, the HICP has fallen to and through zero hugging the zero line for a longer period of time. The PPI is simply more volatile than the HICP and it peaks at two or three percentage points higher than the HICP. Still, if the PPI is starting to turn, that probably would set the next trend for the HIPC too. Consumer prices in the EMU no longer are falling. And the PPI may be now moving up from its latest cycle low point.

Oil still holds the keys to the inflation kingdom

Where prices stand in the business cycle will depend a lot on oil and on other commodity prices. Central banks still are trying to get inflation in gear so that economies can operate on more normal footing. When inflation becomes normal, interest rates can become more normal and saving once again will have a greater purpose. A lot is riding on what oil prices do next and for the moment that trend is still touch and go. Meantime, central banks continue to try to jump start both inflation and growth and they continue to have little success in getting those two things going. While the U.S. once seemed to have had growth in hand and inflation starting to rise, that whole process is now in disarray. Prices are falling in Japan again and now Japan has a fiscal package. South Korea has a fiscal package. China is taking fiscal steps. But the U.S. and Europe are not. The jury is still out on how successful all this policy action will be. In truth, policymakers still seem to be pretty confused.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief