Global| Aug 03 2007

Global| Aug 03 2007Euro Area Services Sector Points to Slow Down but Slower Slow Down

Summary

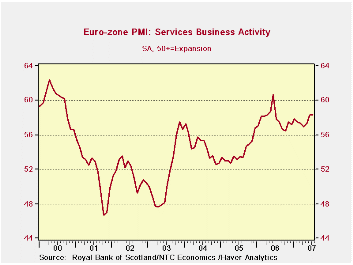

Service sector in clear slow down as the index drops from its peak. The slowdown in the services sector indicated by the NTC service sector index is, in its character, much like that in the MFG sector with only some small shifts in [...]

Service sector in clear slow down as the index drops from its peak.

The slowdown in the services sector indicated by the NTC service sector index is, in its character, much like that in the MFG sector with only some small shifts in the date of past cycle peaks. Like the MFG sector report, the service sector shows that a slowdown is in train. Also like the MFG report the services sector slowdown is at a slower pace than it has been in the past. Indeed on the chart the hopeful sign is that after its retrenchment services may once again be back in the growth channel and growing.

Right now the Euro area economy is 13 months past it service sector peak for this cycle. At this point the index is lower by 3.8%. In the previous three cycles at the 13 month mark the services index would have been down by 9.5% from that peak. That is to say that the slowdown would have been more severe by about one third. Although some of the past cycles peaked at a high point than this one has, due to the slower erosion of the service index, the current index not only has fallen by less, but it stands at a higher point than for any of the past cycles 13-months past their peak.

The UK continues to break the mold and to part company with EMU members as the drop in the UK service sector brings it to its lowest level since Sept of 2006. Most EMU countries are seeing the service sector rebound over the past two months; for the UK it’s been erosion. For the main EU countries their services indexes were last lower in May or June of this year, very recently. So the rebound is very tentative.

Still, based on the range of values since early 2000 it is Germany with the relatively strongest service sector. Its 58.47 reading for the service sector is still in the top 15 percentile of its values over the period. As an individual country, the UK would be the second highest in its range for the grouping in terms of its service sector rank within its range, but for the whole of EMU the services index stands in the top 22 per cent of its range, above the UK on this score. In terms of raw services readings the UK reading of 57.0 is not strong, but comparisons across countries are better done with reference to each countries’ own range since variability characteristics are not standardized across countries.

Hold that pose - our picture of Europe. The picture we get of Europe is that the MFG indexes are sliding and so are the services measures. But the pace of slippage is less than what it has been in the past. At the same time employment conditions (unemployment) are improving. The labor market always lags activity so this is not telling yet. The interesting question for Europe is whether this slide will stop the improvement in unemployment or whether it is a minor meltdown that will permit unemployment progress to continue. If unemployment progress continues, there is some chance to pull the retail sector into the recovery it has not yet joined and to thereby extend the expansion.

Right now the performance of Europe is remarkable given the strength of the euro (and the pound) as those currencies have still been edging higher this year from already high levels. With exporters more ‘up against it’ for competitiveness reasons, an improvement in domestic demand based on the consumer supported by a still improving job market is just what Europe needs. However, it is not clear if that is attainable especially with the ECB and BOE worried over inflation trends and with each block poised to hike rates. Lurking in the background, should recovery slip, is the pressure, right now emanating from France, to press more on China over trade issues. Protectionism is always more compelling when domestic growth weakens.

| Jul-07 | Jun-07 | 3-Mo | 6-Mo | 12-Mo | Percentile* | |

| Euro-13 | 58.34 | 58.33 | 57.98 | 57.63 | 57.42 | 78.5% |

| Germany | 58.47 | 58.88 | 58.27 | 57.90 | 56.91 | 85.8% |

| France | 58.93 | 58.98 | 58.61 | 58.77 | 59.40 | 60.7% |

| Italy | 58.46 | 57.92 | 57.64 | 56.18 | 55.81 | 71.8% |

| Spain | 56.33 | 55.31 | 55.95 | 55.91 | 56.94 | 68.4% |

| Ireland | 56.19 | 56.93 | 56.00 | 58.37 | 59.49 | 47.9% |

| EU only | ||||||

| UK | 57.02 | 57.74 | 57.31 | 57.36 | 58.06 | 75.2% |

| *Percentile is over range since May 2000 | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief