Global| Jun 05 2013

Global| Jun 05 2013Euro Area Services Edge Higher in May

Summary

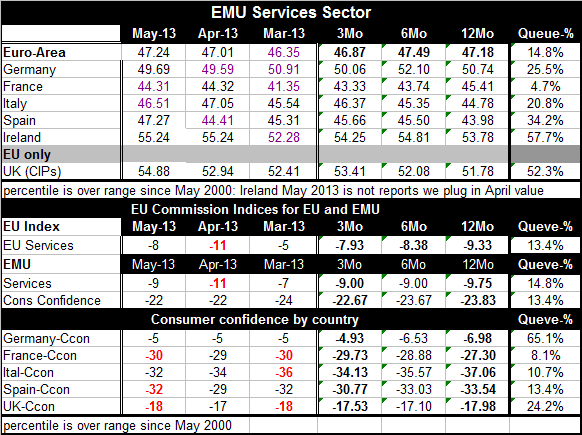

In the European Monetary Union (EMU) the services sector improved to a reading of 47.24 from 47.01 in April. The rise in the May reading is minor and it still leaves the service sector in a contracting position in the Eurozone. [...]

In the European Monetary Union (EMU) the services sector improved to a reading of 47.24 from 47.01 in April. The rise in the May reading is minor and it still leaves the service sector in a contracting position in the Eurozone. Eurozone service sector has now been in a declining mode for 16 months straight.

In the European Monetary Union (EMU) the services sector improved to a reading of 47.24 from 47.01 in April. The rise in the May reading is minor and it still leaves the service sector in a contracting position in the Eurozone. Eurozone service sector has now been in a declining mode for 16 months straight.

In May the German service sector also declined on balance. It showed a small pickup relative to April. In France the service sector decline continued at about the same pace as it did in April; April had recovered somewhat from a low in March. In Italy, the services sector contracted at an expedited rate compared April but still isn't as bad off as it was in March. In Spain, the index improved significantly from its April value but still shows a substantial degree of decline. Ireland has not reported a value for May we insert the value for April into the May slot in order to accomplish the other calculations the table. In the UK the service sector moved up rather smartly and shows strong expansion. Among the countries highlighted the table only the UK and Ireland show net expansion and that's only if the April figure stands up on its final release for Ireland, as we using the April value for May in Ireland.

The German service sector has declined for a two months in a row following a string of increases which is preceded by an irregular series of expansions and contractions for the sector. France's service sector has posted its 10th straight contraction. Italy has logged its 24th straight contraction for its service sector. Spain has logged 23 straight months of contractions in its service sector. Again, if Ireland's expansion is confirmed at about its April level it will log the 10th straight month of expansion. The UK an EU member, not a member of the single-currency union, has five straight increases, a decline, and then a string of 23 straight increases. It service sector has been quite resilient despite its economy being in and out of recession.

Service sectors throughout the Eurozone continues to be relatively impacted. Eurozone itself lies at about the 15th percentile of its historic rank, implying that it's been worse than the May reading only about 15% of the time. Ireland, using the April value, is stronger only about 43% of the time while Spain is weaker only 34% of the time Germany is weaker only 25% of the time and Italy is weaker about 20% of the time. France's is in the league of its own right now with it service sector weaker only about 5% of the time.

In the table we present for comparison over the same time the ranking of the euro services sector according to the European Commission indices. We find that its rank standing at about the 15th percentile is exactly the same as in the market survey even though the two surveys use a different method of presentation.

At the bottom of the table we also present some of the figures from the European commission on consumer confidence and we see that the consumer confidence readings are roughly in parallel with the sorts of readings that we see the services sector particularly with France at the lowest level on consumer confidence.

On balance we do see some evidence of bottoming in this report. However, the service sectors across the Eurozone continue to be quite week. The best that we can say is that the pace of decline for the most part seems to be slowing. There still is a gap before these indices are going to signal expansion. Only one country in the table, or two, if we include Ireland based on its April value, are showing actual expansion in their respective service sectors. Other than that the next highest reading comes from Germany which may be on the verge of a turning point for the service sector as its metric at 49.69 is already close to break-even at 50. Other than that the best reading comes in Spain, a 47, in Italy around 46, and these are still relatively weak levels.

It's not clear whether there is that much momentum in Europe's sector. In addition to the region's internal strife, several countries in the euro-Zone are going to be dealing with some very difficult flooding issues which could impact their economic data in the coming months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief