Global| Apr 04 2017

Global| Apr 04 2017Euro Area Retail Sales Post February Gain

Summary

Euro area retail sales advanced by 0.7% in February as overall sales rose by 1.8% year-on-year. Nonfood sales rose by 1.1% year-on-year; they rose by 0.7% month-to-month showing steady acceleration with three-month sales at a pace of [...]

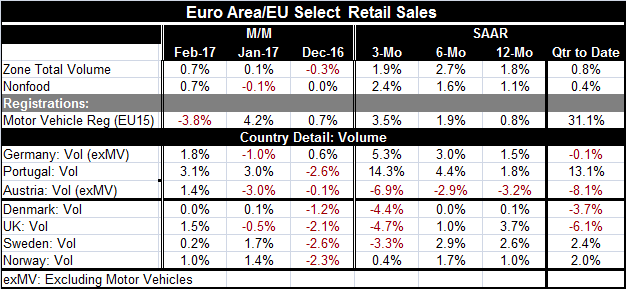

Euro area retail sales advanced by 0.7% in February as overall sales rose by 1.8% year-on-year. Nonfood sales rose by 1.1% year-on-year; they rose by 0.7% month-to-month showing steady acceleration with three-month sales at a pace of 2.4% ahead of the six-month pace of 1.6% which in turn is ahead of their 12-month pace of 1.1%. Motor vehicle registrations in the EU area also are showing the same sort of steady sequential acceleration with year-on-year growth at 0.8% and even with auto registrations in February having fallen by a sharp 3.8%.

Euro area retail sales advanced by 0.7% in February as overall sales rose by 1.8% year-on-year. Nonfood sales rose by 1.1% year-on-year; they rose by 0.7% month-to-month showing steady acceleration with three-month sales at a pace of 2.4% ahead of the six-month pace of 1.6% which in turn is ahead of their 12-month pace of 1.1%. Motor vehicle registrations in the EU area also are showing the same sort of steady sequential acceleration with year-on-year growth at 0.8% and even with auto registrations in February having fallen by a sharp 3.8%.

Quarter-to-date moderation

In the quarter-to-date (QTD), the picture is not so rosy as sales are up at just a 0.8% pace with nonfood sales up at a 0.4% pace. However, QTD vehicle registrations are flying at 31.1% annualized pace. The weak QTD sales trace back to a weak December (negative for total sales; flat for nonfood). That leaves the level of sales with no momentum or worse at the end of Q4. Then in early Q1, total sales edged up by just 0.1% as nonfood sales fell. Against that background, the 0.7% rise in both total and nonfood sales just cannot overcome the early weakness and the quarter-to-date growth rates remain weak for both food and nonfood sales despite the solid February gain.

Elsewhere in EMU/EU

Sales were up across the board for our sample of early retail reporting countries in the table (Germany, Portugal, Austria, Denmark, the U.K., Sweden and Norway). Among them, only Denmark posted flat sales; all the rest logged increases ranging from 0.2% (volume) in Sweden to 3.1% (volume) in Portugal. However, we see the impact of weak December as December saw declines in all counties except Germany. Germany did see a sales decline in January that swamped its December gain. As a result, quarter-to-date sales volumes show declines in Germany, Austria, Denmark and the U.K. Portugal logs a substantial increases at a 13.1% annualized rate as its sales rocketed out of their weak December to score 3% plus gains in each of the next two months. Sweden and Norway followed their December declines with less spectacular but steady gains in sales in January and February to post quarter-to-date growth rates of 2% to 2.4%.

Soft data/hard data

Despite some enthusiasm regarding strength in 'soft data reports' like the PMI gauges, retail sales are another 'hard data' or accounting type 'add it up' data report that fails to score high on the ebullience scale. Trends for retail sales are favorable but not very dynamic. However, retail sales volumes in the euro area are above their precession level of 2008. It has taken so long to restore these sales levels that growth over this nine-year period averages less than 0.2% per year.

Summing up

So there is some recovery in the European retail sale sector. However, it is not strong or bankable. The gain in the nonfood sector has been a little more steady and solid-looking, but it is not dynamic either and not the kind of growth that puts a rubber stamp on the strength we have seen in recent 'soft data' reports. We are still waiting to find hard data evidence that the soft data strength will come to fruition

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief