Global| Feb 04 2021

Global| Feb 04 2021Euro Area Retail Sales Make Minor Rebound

Summary

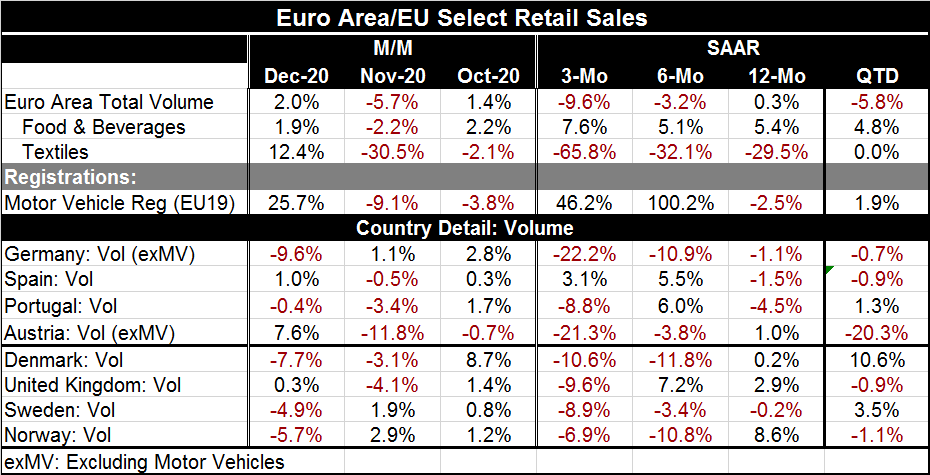

Retail sales rose in December but did not gain back all the ground lost in November’s drop. December brought a month-to-month gain in sales volume of 2% in the wake of November’s 5.7% monthly drop. In fact, retail sales growth rates [...]

Retail sales rose in December but did not gain back all the ground lost in November’s drop. December brought a month-to-month gain in sales volume of 2% in the wake of November’s 5.7% monthly drop. In fact, retail sales growth rates have become progressively weaker from 12-months to six-months and from six-months to three-months.

Retail sales rose in December but did not gain back all the ground lost in November’s drop. December brought a month-to-month gain in sales volume of 2% in the wake of November’s 5.7% monthly drop. In fact, retail sales growth rates have become progressively weaker from 12-months to six-months and from six-months to three-months.

Food and beverage gains have held up on that timeline. Textile sales volumes have progressively weakened on that timeline.

The graphic depicts the EU Commission retail sector surveys; these extend through January 2021. That graphic shows all depicted countries with a retailing index below that of February 2020 just before the virus struck and spread. All countries show a dive in retailing, a sharp rebound, and then a phase of peaking and easing lower again. Spain is the only country in graphic that looks like it is maintaining steady retail confidence and it is doing that at a much reduced level compared to early last year. Germany is showing a sharp recent drop off related to its ongoing lockdown to contain the virus.

Motor vehicle sales have been quite volatile over the last year. Sales rose very sharply over six months then they halved that growth rate over three months but still managed to post a large leap in sales. Despite all that, vehicle sales are still lower by 2.5% year-over-year.

Country level retail sales show a rather consistent pattern. Of the eight countries in the bottom panel of the table, all but Spain show retail sales declines over the three months ending in December. Germany and Austria show declines with double-digit growth rates. The United Kingdom, Sweden and Portugal log annualized declines of more than 8%. There is widespread weakness over the most recent three months. Over six months, results are more mixed as five countries show sales declines and three show gains. There are three countries with double-digit drops in sales and none with double-digit gains. Over 12 months, the split is even with four countries reporting sales declines and four reporting sales gains. The year-on-year results simply show a mix of outcomes with no real themes; other than that EMU member countries show sales declines in three of the four EMU member reporters compared to a decline in only one reporter among four in the non-EMU group.

These are December results so the QTD (quarter–to-date) column provides the quarter-over-quarter annualized growth rates for Q4. The euro area as a whole shows sales volumes falling at a 5.8% annual rate in Q4. Motor vehicle sales are up at a 1.9% pace. By country, five show sales declines in Q4 compared to three with gains (Portugal, Denmark and Sweden). At the extremes, Denmark shows a 10.6% annual rate of gain in Q4 compared to Austria’s -20.3% annualized drop. Sweden logs a gain at a 3.5% pace with Portugal up at a 1.3% pace. Germany, Spain, the U.K. and Norway all have percentage drops in the narrow range of -0.7% to -1.1%.

On balance, retailing in EMU looks troubled. Of course, it is a sector that is punished when there are lock downs… and there are lockdowns. Germany and Spain have been having lockdowns. Portugal in February is still having some real problems with virus spread- enough that Germany has sent them medical help. Sweden continues to muddle through imposing as few constraints on the economy as possible, but a few more than they were employing in the early rounds of dealing with the virus. The U.K. is engaged with the most serious lockdown and that is continuing. Obviously the outlook has a lot to do with how lockdown restrictions are dealt with in the coming months and that will have a lot to do with vaccination progress. That has become a tired old disclaimer by this point. But it is still true.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief