Global| Nov 12 2008

Global| Nov 12 2008Euro Area Production Tanks in September

Summary

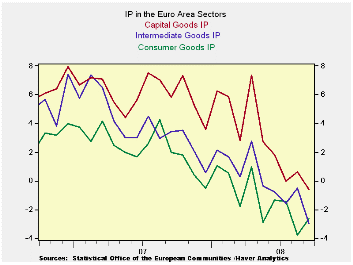

Euro Area industrial output (IP) fell sharply in October dropping by its largest amount in over five years. In Sept MFG IP is dropping across all major product groupings just as it did in August and nearly did so in July. In the EMU [...]

Euro Area industrial output (IP) fell sharply in October

dropping by its largest amount in over five years. In Sept MFG IP is

dropping across all major product groupings just as it did in August

and nearly did so in July. In the EMU the drop in IP has become

intense, widespread and persistent. Across the largest EU/EMU countries

IP also fell in Sept with the exception of Spain where numbers are more

volatile than resilient. Spain in fact has the deepest decline in IP

for Q3 at a -14% annual rate. Indeed, Germany, France, Italy and the UK

all have drops in IP in Q3 as well. It is pretty clear that with

declines of this magnitude (apart from Spain’s larger drop) ranging

from -2.7% to -5% these economies are in recession or heading there

soon.

In Germany the wise men issued a statement urging more public

spending to boost the economy and urged the ECB to cut rates as much as

it could see its way to do. They predict a recession in German for

2009, based on a wide variety of metrics. .

Similarly the Bank of England in a statement issued on the day

said that the UK economy has probably entered recession in the second

half of 2008. It does not see GDP growing until the second half of

2009. It sees inflation falling relatively rapidly.

Assessments of the economy in Europe are being cut rapidly.

Evidence on the economy is that growth is fading fast. In this

environment oil prices are sliding on the weakness in global demand

even with some OPEC output cuts having been announced and with China

having unveiled a better-than one-half of one trillion dollar stimulus

plan. China further announced that as part of that plan it would

implement export tax rebates and cut taxes on some export items. In

July the government had implemented some export tax breaks for the

garment industry. While China portrays some of these as factors to

‘stimulate domestic demand’ it seems that these really are efforts to

keep getting a chunk of foreign demand at a time that the size of that

pie is shrinking or at least growing more slowly. China’s ‘stimulus’

may not be as helpful to the rest of the world as it thinks.

| Euro Area MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | 3-Mo | 6-mo | 12-mo | ||||||

| Euro Area Detail | Sep 08 |

Aug 08 |

Ju 08 |

Sep 08 |

Aug 08 |

Sep 08 |

Aug 08 |

Sep 08 |

Aug 08 |

Q-3 |

| MFG | -1.7% | 0.8% | -0.2% | -4.5% | 1.9% | -4.5% | -2.5% | -2.3% | -1.1% | -3.4% |

| Consumer Goods | -0.4% | -0.5% | 0.0% | -3.5% | 0.5% | -2.7% | -3.9% | -2.6% | -3.7% | -2.9% |

| Consumer Durables Goods | -2.5% | 1.2% | -1.0% | -8.9% | 3.1% | -6.2% | -5.2% | -6.2% | -6.7% | -- |

| Consumer Nondurables Goods | -0.4% | -0.3% | -0.1% | -3.5% | 0.9% | -2.8% | -3.2% | -2.3% | -3.0% | -- |

| Intermediate Goods | -2.6% | 1.4% | -0.3% | -5.9% | 3.7% | -5.3% | -1.6% | -3.0% | -0.5% | -3.6% |

| Capital Goods | -1.8% | 1.4% | -0.4% | -2.8% | 3.1% | -2.1% | -2.1% | -0.6% | 0.6% | -3.8% |

| Main Euro Area Countries and UK IP in MFG | ||||||||||

| Mo/Mo | 3-Mo | 6-mo | 12-mo | |||||||

| MFG Only | Sep 08 |

Aug 08 |

Jul 08 |

Sep 08 |

Aug 08 |

Sep 08 |

Aug 08 |

Sep 08 |

Aug 08 |

Q-2 Date |

| Germany: | -3.8% | 3.3% | -1.8% | -9.4% | 8.4% | -7.1% | 0.2% | -2.0% | 2.0% | -4.8% |

| France: IP excl Construction | -0.5% | -0.4% | 1.3% | 1.6% | 0.4% | -4.2% | -5.4% | -1.9% | -2.6% | -2.7% |

| Italy | -2.3% | 0.4% | -1.3% | -12.1% | -2.1% | -8.0% | -4.1% | -5.7% | -4.3% | -8.4% |

| Spain | 3.1% | -10.1% | 12.1% | 16.7% | -16.2% | 14.8% | -25.4% | -4.4% | -11.2% | -14.0% |

| UK | -0.8% | -0.6% | -0.2% | -6.0% | -4.9% | -5.1% | -4.7% | -2.2% | -2.0% | -5.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.