Global| Sep 02 2016

Global| Sep 02 2016Euro Area PPI Ticks Higher Month-to-Month

Summary

The euro area PPI rose in July, ticking up by 0.1% as it fell by 2.9% year-over-year. Capital goods prices rose by 0.1% in July as consumer goods and intermediate goods prices each rose by 0.2%. Year-on-year capital goods prices are [...]

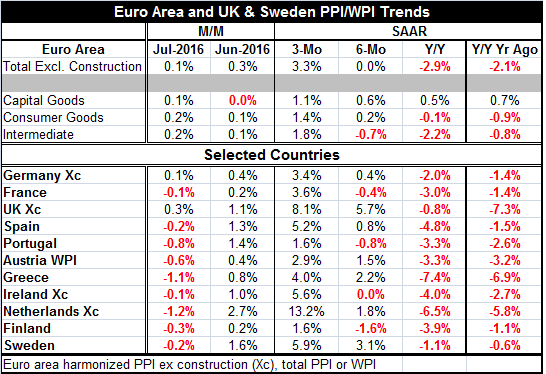

The euro area PPI rose in July, ticking up by 0.1% as it fell by 2.9% year-over-year. Capital goods prices rose by 0.1% in July as consumer goods and intermediate goods prices each rose by 0.2%. Year-on-year capital goods prices are higher, rising by 0.5% while consumer goods prices are lower by a skinny 0.1% and intermediate goods prices still are lower by 2.2%. All sectors show inflation, having begun to accelerate from 12-month to six-month and from six-month to three-month.

The euro area PPI rose in July, ticking up by 0.1% as it fell by 2.9% year-over-year. Capital goods prices rose by 0.1% in July as consumer goods and intermediate goods prices each rose by 0.2%. Year-on-year capital goods prices are higher, rising by 0.5% while consumer goods prices are lower by a skinny 0.1% and intermediate goods prices still are lower by 2.2%. All sectors show inflation, having begun to accelerate from 12-month to six-month and from six-month to three-month.

Country-level data, however, show more price weakness in July as 9 of the 11 countries in the table show June-to-July price drops. Germany and the U.K. are exceptions with prices increasing month-to-month. For the U.K., the PPI sped ahead by 0.3% on the month.

Still, if we look at sequential growth rates at the country level from 12-month to six-month and from six-month to three-month, we find that prices are accelerating on all those horizons for each county in the table. Inflation at the PPI level is accelerating on a broad front in the EMU and in the two EU members in the table. Dutch inflation is actually galloping ahead at a 13.2% annual rate over three-months.

The chart shows a clear bottoming tendency for prices in the main EU sectors. The downturn in prices has slowed and country by country there is a shift underway.

Whether this is the final turning point or not will depend a lot on oil. Oil prices continued to be fickle and their ability to `stick' at a higher level will also depend on growth. The global manufacturing PMIs released yesterday were not encouraging on that score, especially not the U.S. ISM manufacturing PMI which dipped below 50 yet again.

At the IMF, Christine Lagarde is talking about cutting forecasts again and she is urging countries to take forceful steps to escape the pull of weakness. Economic weakness can be like a black hole with its own gravitational force pulling an economy back into the abyss. Sometimes something is needed to more clearly signal that ways of weakness a being put behind and that growth lies ahead. Unfortunately, in this cycle there is little left to be done to create such a clear signal or illusion. There really is nothing left up my sleeve. Monetary moves have been made so often that what monetary policy has left to offer may chill the spine more than warm the heart. Such are negative interest rates. The game is still on.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief