Global| Aug 02 2017

Global| Aug 02 2017Euro Area PPI Shows Broad Based Weakness...Sort of

Summary

The year-on-year inflation rate has been pushed up in recent months for all three main PPI components as well as for the headline. Yet, year-over-year inflation for most countries peaked in the early months of 2017. From one year and [...]

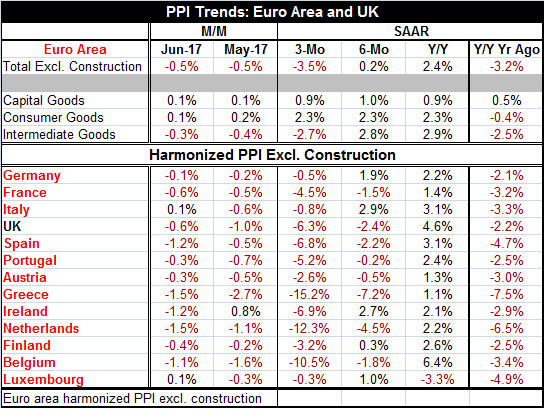

The year-on-year inflation rate has been pushed up in recent months for all three main PPI components as well as for the headline. Yet, year-over-year inflation for most countries peaked in the early months of 2017. From one year and shorter, the push to higher prices already is unwinding. Three-month inflation is less than six-month inflation and six-month inflation is less than 12-month inflation: this is true of the headline PPI and for intermediate goods prices as well as for the 12 EMU nations listed in the table as well as the U.K. Only Ireland and Luxembourg are exceptions to this pattern. However, by sector we see essentially steady capital goods inflation at or just below the one-percent mark. Sequential consumer goods inflation is stuck at 2.3% for three-months, six-months and 12-months. Intermediate goods prices display the result we see as so robust across countries that PPI inflation is decelerating steadily.

The year-on-year inflation rate has been pushed up in recent months for all three main PPI components as well as for the headline. Yet, year-over-year inflation for most countries peaked in the early months of 2017. From one year and shorter, the push to higher prices already is unwinding. Three-month inflation is less than six-month inflation and six-month inflation is less than 12-month inflation: this is true of the headline PPI and for intermediate goods prices as well as for the 12 EMU nations listed in the table as well as the U.K. Only Ireland and Luxembourg are exceptions to this pattern. However, by sector we see essentially steady capital goods inflation at or just below the one-percent mark. Sequential consumer goods inflation is stuck at 2.3% for three-months, six-months and 12-months. Intermediate goods prices display the result we see as so robust across countries that PPI inflation is decelerating steadily.

The main point about that trend is that the PPI itself is substantially about oil prices. The chart "EMU PPI vs. Brent Oil Price" shows that the PPI follows closely the same sort of pattern sketched out by Brent oil prices. This explains both the widespread result across countries and the fact that intermediate goods prices are the ones that create most of this sympathetic effect with Brent in the PPI. The PPI does not well translate into 'what's next' for the HICP

That brings us to the second point, which is that the PPI while a near slave to the twists and turns of Brent oil prices is not a harbinger for consumer prices (HICP). The PPI does tend to signal where HICP highs and lows will be reached, but the PPI is a substantial exaggeration of those trends compared to the CPI. The PPI often makes its clear bottoms and tops ahead of the HICP. Right now the PPI is rolling over from a recent peak and the HICP is showing that it too has put its recent peak behind it. This is interesting because the ECB targets HICP inflation and the HICP after a long period of underperforming is still below its target and yet it is turning even lower while the ECB - a central bank with only an inflation target for its mandate- is looking to put an end to its period of extraordinary accommodation. Will it? Can it?

Allegedly 'data dependent' central banks with an agenda

The European Central Bank is experiencing the same problem encountered by the Federal Reserve in the U.S. Both have inflation running below target and both central banks have run super accommodative monetary policies for a period so long that some members on their respective policymaking boards are simply nervous that it is time to reverse course even without any good reason from current data. But the ECB's policy mandate is solely about inflation; thus, making it hard for the ECB to make policy without a reason from inflation. In the U.S., the Fed has a dual mandate and while inflation is still 'too low,' it is widely believed that the economy is too strong as evidenced by the too low unemployment rate. Yet, the Fed has created a mythology to give it a freer hand in policy. It argues that if it sees or forecasts a higher inflation rate that is good enough to justify policy changes. The Fed has found a way to release itself from the shackles of reality to make policy based on its own judgment which has not been very good these days. And while the unemployment rate in the U.S. is widely acknowledged to be too low, it is not creating much wage inflation and that reflects badly on those arguing that the unemployment rate is in fact too low or unsustainably low.

Policy is what policy does

So the EMU region and the U.S. continue to make policy with this sort of oddity in the background- or the foreground. While central banks often tell us that economic expansion does not die of old age and that we should not be concerned about oncoming recession just because the expansion is long in the tooth, central bankers themselves seem to have run afoul of their own advice as they act as though their business cycle inflation alarm clock is ringing loudly. All we can do is to watch and wait. Central bankers will have to make some sort of policy and with it they will be throwing their lot in with one theory or the other. It is not clear what these two banks will do, but markets are increasingly sure that both are getting ready to tighten policy. Further rate hikes from the Fed are expected while the ECB is expected to make its start soon by dismantling some policies in support of accommodation. Meanwhile, the Bank of England is caught in a trap caused by its own actions. Past strong stimulus has weakened the pound and sent a chill of import price inflation though the economy yet with Brexit coming on there are negative economic events in train that might obviate the need for the BOE to undermine its own stimulus soon. The monetary policy committee there is visiting that argument. In Japan, very little seems to be happening. Inflation has not picked up and growth is surviving but not flourishing. Central banks are at their wits ends and mostly kicking the same old can down the same old road. The Fed is kicking new can down a new road, but its GPS still is not working.

Monetary policy: is it just nostalgia?

While monetary policy seems to have passed its point of peak usefulness, the lingering question is whether that means it's time to step away from it and to treat other aspects of the economy - like interest rates - to normalcy? It is not clear that just because there is no longer a clear link from monetary policy to stimulus and growth that taking away monetary stimulus will not have an impact. And while growth currently seems more solid, it is still modest in the U.S., Europe and Japan as well as globally. Central banks act as though they are walking on thin ice. And in reality they are having a hard time handicapping the risks; are they underfoot or somewhere else? There seems to be a good deal of uncertainty and internal dispute about just exactly what the real risk is at the moment. Welcome to the New Normal!

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief