Global| Nov 04 2016

Global| Nov 04 2016Euro Area PPI Falls As Oil Unwinds Again

Summary

The euro area PPI fell in September after falling in August; it is now dropping by 1.6% year-over-year in September and logged its smallest drop since November 2014. Prices fell month-to-month in five of 13 of the EU countries in the [...]

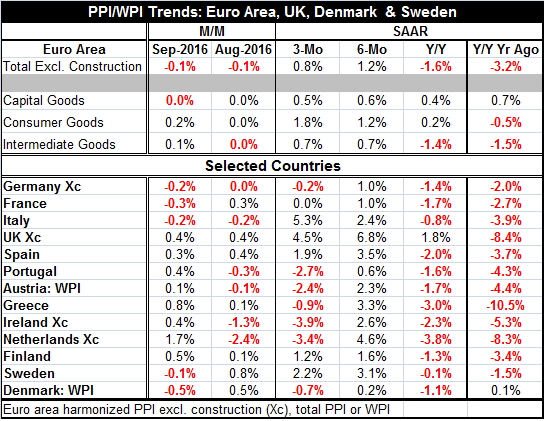

The euro area PPI fell in September after falling in August; it is now dropping by 1.6% year-over-year in September and logged its smallest drop since November 2014. Prices fell month-to-month in five of 13 of the EU countries in the table. Over three months prices are falling in seven countries. Year-over-year prices are falling in 12 of 13 countries (the U.K. is the exception). But over six months prices are higher on balance everywhere even though the monthly PPI is lower month-to-month in each of the last two months. Got all that? Price trends in the PPI are now 'officially' convoluted.

The euro area PPI fell in September after falling in August; it is now dropping by 1.6% year-over-year in September and logged its smallest drop since November 2014. Prices fell month-to-month in five of 13 of the EU countries in the table. Over three months prices are falling in seven countries. Year-over-year prices are falling in 12 of 13 countries (the U.K. is the exception). But over six months prices are higher on balance everywhere even though the monthly PPI is lower month-to-month in each of the last two months. Got all that? Price trends in the PPI are now 'officially' convoluted.

Inflation and the oil market mess

Oil has been the big reason for the drop in the PPI and more recently for its reversal (price rise) and even more recently for the reversal of the reversal (price fall). OPEC is at it again, trying have its cake and eat it too (have high oil prices and pump oil too). It seems to hope to control oil prices using verbal warfare while trying to avoid output cuts. OPEC members simply have a hard time adjusting to the oil market facts of life. Some members act as though they are entitled to high prices and that wish will make it so. But the oil market does not work on wishes. It takes exploration, drilling, pumping, conveyance, inventories and demand to make an oil market. It takes real actions up and down the line. So the future path for oil prices is again in doubt as U.S. firms are drilling and pumping while OPEC firms (and oil-producing friends of OPEC and others) continue pumping. Inventories are all but overflowing while demand is still slow to develop. Add a dash of salt and it's a recipe for weaker not stronger oil prices even with an extra-helping of wishing. Prices are falling again and now Brent oil is down by 14% from its recent highs. You can expect these oil price movements to wreak havoc with trends in the PPI and to find their way to the CPI eventually as well.

Let the convolution begin!

PPI trends which had been starting to reverse their past relentless fall and still show the PPI with net gains over six months, are already stepping back from that pressure. In the most recent three months, inflation is lower than over six months in all countries except Italy. Even with the weakest year-over-year PPI headline in 22 months, three-month trends show that the PPI is starting to push lower again. Weakening oil prices are the culprit. Still, several countries have 'real' inflation rates over three months such as Italy with PPI prices up at a 5.2% pace over three months and the U.K. with PPI inflation up at a 4.5% pace over three months. But those are exceptions as three-month inflation has a negative growth rate of -2% or less in the Netherlands, Ireland Austria, and Portugal. Among the four largest EMU economies, only Germany has prices falling over three months (-0.2% annual rate) but in France prices are flat over three months.

Sector trends seem to show more strength

By sector, capital goods, consumer goods and intermediate goods prices as well as the PPI headline all are showing gains over three months and six months. But only consumer goods prices show true acceleration. Intermediate goods prices are on the cusp of acceleration as they are net lower by 1.4% over 12 months then rising at a 0.7% pace over both three months and six months. Capital goods prices are up by 0.4% over 12 months then accelerate to a 0.6% annualized rate over six months before cooling to a 0.5% pace over three months. Sector trends seem to show more strength than the country level data suggest. That may be because in the country level data some of the greatest price weakness comes from smaller economies. Among the big four economies in the EMU, only Germany has a dropping PPI over three months. That will also mean that the sectors in the large countries have stronger price trends than in the smaller countries and they will, because of the size of their economies, have a greater weight in determining the EMU-sector results.

Summary

The PPI is interesting and we can see it going through some rather complicated cycles right before our eyes. Of course, the PPI influences the CPI (HICP), but those two series also have some very separate trends. The fall off, ramp up then reversal of the PPI has implications for CPI and the suggestion is that the oil price effect is no longer having such a relentless upward push on either the PPI or the CPI sectors.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief