Global| Oct 04 2016

Global| Oct 04 2016Euro Area PPI Falls Again As Rising Trend Is Interrupted

Summary

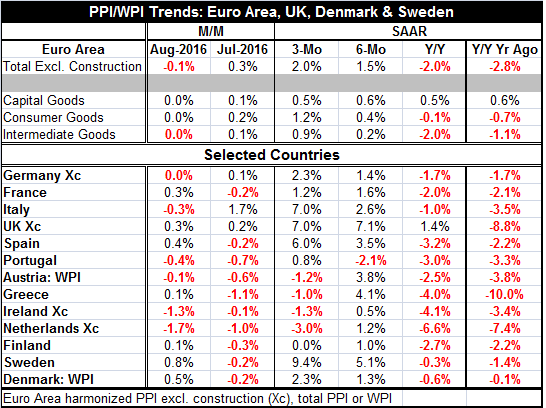

PPI prices are starting to turn higher. At least the downward momentum is shifting and the rate of change is no longer as powerfully negative. Seven of the thirteen monthly PPI movements in the table are positive in August; that [...]

PPI prices are starting to turn higher. At least the downward momentum is shifting and the rate of change is no longer as powerfully negative. Seven of the thirteen monthly PPI movements in the table are positive in August; that compares to only three of thirteen last month.

PPI prices are starting to turn higher. At least the downward momentum is shifting and the rate of change is no longer as powerfully negative. Seven of the thirteen monthly PPI movements in the table are positive in August; that compares to only three of thirteen last month.

However, over three months eight nations show positive PPI gains. Over six months 12 show positive gains, but over 12 months only one shows a positive gain. The actual positive inflation effect is not present in year-over-year data just yet. The headline PPI (excluding construction) is down by 2% over 12 months even as the six-month annualized gain is 1.5% and the three-month pace is 2%. There is overall price acceleration and a shift to a tendency for prices to rise on balance over short horizons. There is rising price momentum in train. But it is also uneven momentum. It appears that upward momentum to some extent speeded up over six months but has slowed down over three months leaving some price divergence in its wake.

While price trends are turning and probably inexorably turning higher as the PPI tracks oil (more on this below), there is also prevarication. We do find fewer prices falling in August across countries than in July. But we also find that in terms of annual rates of change there are only five countries whose pace is accelerating over three months compared to six months while over six months all thirteen are accelerating compared to their respective 12-month paces.

Clear price decelerations for three-month compared to six-month are present for Greece, Austria, the Netherlands, and Ireland; in Finland momentum is negative comparing six-month gains to three-month as price trends went flat over three months. Meanwhile, the pace of inflation is substantially stronger over three months compared to six months (here we look at the change in pace on these horizons) for Italy, Sweden, Portugal, and Spain. Some countries lie in the middle ground, of course.

Interestingly, the U.K., still an EU member but not a single currency participant, shows positive price gains on all horizons. The U.K. shows a sharp inflation gain over six-month compared to 12-month, but its acceleration on that basis only ranks as the fourth most. Inflation is not accelerating sharply in the U.K.; it is just higher. And with sterling today plunging to a 33-year low, we would expect the impact of exchange-rate induced inflation to hit the PPI harder and relatively soon.

What we are seeing is that although Inflation began to turn higher over six months, over three months some countries are showing some backsliding and deflation trends (disinflation trends?) are reigniting especially as we noted above in Austria, Greece, Ireland, and the Netherlands (to a lesser extent in Finland, France and Italy). There has been backtracking.

The chart shows that for the EMU the turn of the PPI trend is broadly called by oil prices. The ability of the Brent oil price swing to presage shifts in the PPI rate of inflation is quite clear and should come as a surprise to no one. Yet, the impact also has to do with the magnitude of the change. Oil prices when they begin moving can move so sharply and so broadly that they clearly do and should affect overall trends, at least initially, as oil prices basically set new Sea changes in place at higher or lower price levels. The percentage changes mark the path, but basically oil is transiting from one price level to another to generate this percentage change. And during this move oil prices themselves can be overshooting their mark and backtracking which will generate a more complex patterns of percentage changes on smaller magnitudes of change. As these oscillations get smaller, the percentage changes get smaller and the knock on effect to the PPI gets smaller, too. What is happening now is that the powerful oil price effects has washed over all the EMU countries and now some aspects of their national differences and different national abilities to deal with energy price shocks per se are starting to show through.

The chart shows that for the EMU the turn of the PPI trend is broadly called by oil prices. The ability of the Brent oil price swing to presage shifts in the PPI rate of inflation is quite clear and should come as a surprise to no one. Yet, the impact also has to do with the magnitude of the change. Oil prices when they begin moving can move so sharply and so broadly that they clearly do and should affect overall trends, at least initially, as oil prices basically set new Sea changes in place at higher or lower price levels. The percentage changes mark the path, but basically oil is transiting from one price level to another to generate this percentage change. And during this move oil prices themselves can be overshooting their mark and backtracking which will generate a more complex patterns of percentage changes on smaller magnitudes of change. As these oscillations get smaller, the percentage changes get smaller and the knock on effect to the PPI gets smaller, too. What is happening now is that the powerful oil price effects has washed over all the EMU countries and now some aspects of their national differences and different national abilities to deal with energy price shocks per se are starting to show through.

It is going to be important to see how much inflation heterogeneity is created in this transition. The standard deviation among the various national PPI percentage changes over 12 months is beginning to rise (inflation and price level divergence). The standard deviation of year-on-year prices changes across EMU member countries now stands at about 2 percentage points, a 53.8 percentile standing on all results since March 1997 (near the median - no alarms yet). But since August 2011, the current divergence has a top 20% standing. Inflation divergence is creeping back into the EMU and price level divergence was the cause of many of the EMU's problems. When prices diverge in a common currency area, all sorts of competiveness issues arise and often are manifested in the budget as policy tries to cushion the shock on the private sector. Redressing competitiveness issues across a common currency area is very painful as Spain and Portugal in particular have found out. Italy and France also have seen some restrictions placed on their abilities to use fiscal policy because of their economic situations expressed mostly in terms of their missing deficit targets or debt to GDP ratio targets or both. As prices (inflation) normalize in the EMU, inflation differences will be something to watch. For now normalization has hit a pot hole as a bit more deflation than expected was introduced in August and now price divergence may be becoming an issue in the EMU again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief