Global| Oct 24 2016

Global| Oct 24 2016Euro Area PMIs Surprise

Summary

The early flash PMI readings for the EMU, Germany and France show upside surprises mainly on the gains in the manufacturing indices in October. Perspective on manufacturing The EMU, German and French manufacturing sectors advanced and [...]

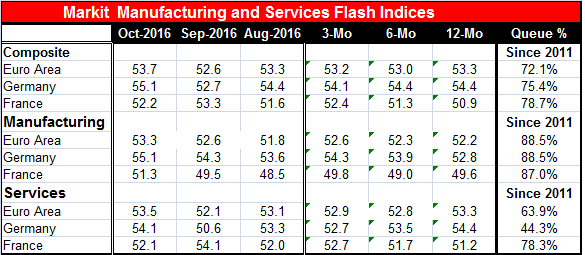

The early flash PMI readings for the EMU, Germany and France show upside surprises mainly on the gains in the manufacturing indices in October.

The early flash PMI readings for the EMU, Germany and France show upside surprises mainly on the gains in the manufacturing indices in October.

Perspective on manufacturing

The EMU, German and French manufacturing sectors advanced and improved in the month and all have standings in their top 15th percentile (or higher) of their respective historic queues of data over the last five and one half years. Of course, this has not been a period of great strength. While Germany has a top 12th percentile standing on a manufacturing diffusion index of 55.1, France has a top 13th percentile standing on a reading of 51.3 not very far above the breakeven value of 50. Still, it is relative progress. The French gauge for manufacturing is above 50 and showing expansion for the first time since February.

Perspective on services

The service sector rankings are much more dispersed. For the EMU, services improved in October with the index rising to 53.5 from September's 52.1 to a 63rd percentile queue standing over the last five and one half years. For Germany the monthly index rose sharply to 54.1 in October from a very weak 50.6 in September and held only a 44th percentile standing over its last approximately five and one half years of data. France backtracked on the month with its services reading falling to 52.1 in October from 54.1 in September. However, France has been so weak that even this lower reading has a percentile queue standing in the top 22nd percentile of its recent historic queue.

Composite trends

However, the trend for the EMU composite index is almost dead flat in terms of its three-month, six-month and 12-month averages (sequential averages). The current reading, however, has jumped up above the three-month average. Germany's average shows a slight progression to weakness, but the current month's 55.1 standing is well above its three-month average reading. France's composite reading shows a progression from 12-month to six-month to three-month that reveals slightly improving strength. That, however, is undone by the October composite which sits below its three-month average. Overall the composite momentum is not impressive and any notion of a pick-up relies wholly with this one month's observation not with any sense of a developing trend.

Manufacturing trends

Manufacturing shows progressions of stronger values for the EMU area and for Germany with each also showing an October reading above its three-month level. That much is encouraging. France, however, shows a mixed picture with all three of these bellwether averages below 50 and with no clear trend but with France's monthly reading for October above its three-month average and also above the six-month and 12-month averages.

Services trends

Once again it is the services sector that is complicated. In the EMU, there is no clear service sector trend, but the current month's reading stands above all the period averages. For Germany, there is a wind down in progress for services across the moving averages, but the sharp gain in October is above at least the three-month and six-month average readings but below the 12-month average. France shows a pick-up in its three-month and six-month averages relative to the 12-month average, but this downshift in October brings its services index back to its 12-month average.

Summary

On balance, there is now a hopeful sign from EMU manufacturing this month. The services sector, however, is still floundering and with very different momentum in different places. In a separate report, UK manufacturers were starting to see orders pick up, but that is in the effect of a great deal of weakness in the British pound sterling in the wake of the Brexit vote. It is far too soon to conclude that there is anything good in train globally that is lifting the manufacturing gauges. However, the gauge for the U.S. from Markit did advance this month, rising to 53.2 from 51.5 but to only a 36th percentile queue standing. Manufacturing, while improving on the month in the U.S., is still at a weak reading, but like Europe, it is showing some steady improvement in its progression of monthly averages with follow-through in this month's observation. Still, the outright manufacturing ranking is much worse for the U.S. than it is for Europe as the dollar has remained relatively strong; in the EMU, the relative rankings are firm but reside at still relatively moderate diffusion reading levels.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief