Global| Jul 23 2008

Global| Jul 23 2008Euro Area Orders Drop Sharply in May

Summary

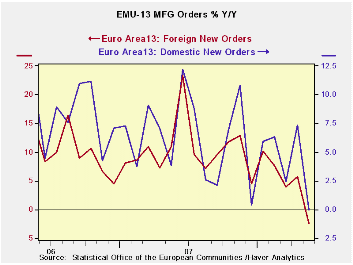

The domestic and foreign orders trend lines now both have discernable downtrends. Growth rate calculations over the key sequential periods also show that declines are becoming more intense in both sectors. Over three months, for [...]

The domestic and foreign orders trend lines now both have

discernable downtrends. Growth rate calculations over the key

sequential periods also show that declines are becoming more intense in

both sectors. Over three months, for example domestic orders are

dropping at an 11% pace while foreign orders are dropping at an 18%

pace. Yr/Yr domestic orders are flat while foreign orders are off by

2.5%. Sales trends are losing momentum as well but only for

intermediate goods is the trend negative over three months (flat Yr/Yr).

The Euro-Area result is the weighted average of the country

results. All thee of the largest Zone countries have orders lower over

three months: Germany France and Italy. Yr/Yr France is down the most

followed by Italy with German orders still up over 12-months but by

less than one-percent.

The slowdown in the e-zone is now undeniable and with orders

turning negative Yr/Yr the potential for something deeper than a

slowdown is in the works. The IMF’s John Lipsky has said that the euro

is now overvalued. The EMU community is being squeezed by a too –strong

euro rising interest rates high inflation (due to just a few items with

spiking prices however) and a slowing global economy. Through all of

this, EMU growth has been supported by strength in capital goods

output. That is now fading. Consumption remains weak. Thus there is

little to cushion the economy from the slowdown emanating from the

capital goods side. Europe’s weakness and slippage is a real phenomenon

and it is echoed by earlier surveys form Zew and the IFO.

| Euro Area and UK Industrial Orders & Sales Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | % m/m | May 08 |

May 08 |

May 08 |

May 07 |

May 06 |

Qtr-2 -Date |

||

| Euro Area Detail | May 08 |

Apr 08 |

Mar 08 |

3Mo | 6mo | 12mo | 12mo | 12mo | Saar |

| MFG Sales | 0.6% | 0.4% | 0.1% | 4.2% | 8.2% | 5.1% | 6.4% | 7.9% | 4.9% |

| Consumer | 0.2% | 0.1% | 0.0% | 1.3% | 1.6% | 2.4% | 6.4% | 7.9% | 1.2% |

| Capital | 0.2% | 0.3% | 0.3% | 3.4% | 5.3% | 5.2% | 4.3% | 4.0% | 3.9% |

| Intermediate | -5.5% | 4.6% | -1.9% | -11.4% | -8.9% | 0.0% | 8.3% | 7.1% | 3.4% |

| MFG Orders | |||||||||

| Total Orders | -3.5% | 2.0% | -1.0% | -9.8% | -8.3% | -1.0% | 8.2% | 12.1% | -2.2% |

| E-13 Domestic MFG orders | -5.5% | 4.6% | -1.9% | -11.4% | -8.9% | 0.0% | 3.8% | 11.3% | 2.8% |

| E-13 Foreign MFG orders | -3.9% | -0.4% | -0.7% | -18.3% | -14.7% | -2.5% | 10.9% | 15.2% | -13.6% |

| Countries: | May 08 |

Apr 08 |

Mar 08 |

3Mo | 6mo | 12mo | 12mo | 12mo | Qtr-2 -Date |

| Germany: | -1.3% | -1.0% | -0.8% | -11.8% | -9.2% | 0.7% | 12.5% | 13.3% | -10.3% |

| France: | -4.6% | 4.5% | -6.6% | -24.6% | -9.2% | -4.5% | 8.8% | 4.5% | -8.8% |

| Italy | -3.1% | 0.5% | -0.9% | -13.4% | -8.2% | -1.1% | 6.9% | 13.6% | -4.4% |

| UK (EU) | -9.3% | 20.6% | -14.1% | -22.1% | -5.5% | 4.8% | 3.9% | 3.1% | 1.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief