Global| Nov 28 2016

Global| Nov 28 2016Euro Area Money Supply and Credit Growth Are Not Behind the Excitement

Summary

After looking at all the monetary stimulus and special lending programs that the ECB has unleashed then turning to look at these charts, you have to wonder if money even matters. Clearly to some, such a statement is anathema. But such [...]

After looking at all the monetary stimulus and special lending programs that the ECB has unleashed then turning to look at these charts, you have to wonder if money even matters. Clearly to some, such a statement is anathema. But such a lack of response from an extraordinary outpouring of monetary stimulus in recent years would have been impossible to predict in advance and if that does not cause you to re-inspect what you believe you are simply a dyed in the wool dogmatist.

After looking at all the monetary stimulus and special lending programs that the ECB has unleashed then turning to look at these charts, you have to wonder if money even matters. Clearly to some, such a statement is anathema. But such a lack of response from an extraordinary outpouring of monetary stimulus in recent years would have been impossible to predict in advance and if that does not cause you to re-inspect what you believe you are simply a dyed in the wool dogmatist.

Central banks pulling back...holding off?

Still, it is no wonder that globally monetary authorities seem to be pulling back from their largesse. Despite the fruitlessness of their labors, central banks understand the monetary excesses they have put into the system and now are starting to be wary of the lagged impact of all that liquidity. When the economy is in poor shape, it is understood that monetary policy can have all the impact of 'pushing on a string.' The question at some point will turn to how the liquidity gets used as conditions normalize.

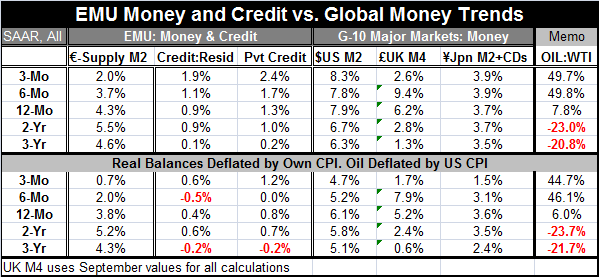

Money and credit growth trends do not excite

What we see in the data is weak-to-stable money growth in the EMU as well as globally. Real money and credit balances are weak to stable as well. Credit growth in the EMU has ticked up on some horizons or remains flat on longer comparisons. But the operative word is 'ticked' as growth has barely moved higher even where it has moved higher.

New day dawning?

I don't know how significant this will turn out to be but the OECD has just lifted its OECD area growth rate outlook as well as its global outlook for 2017 and 2018. The OECD sees fiscal stimulus as the catalyst. It seems to have 'give up' looking for added monetary stimulus as having any effect and moved over to embrace the dark side forces (fiscal policy). In any event, the uptick in its forecast breaks a long string of every forecasting agency cutting outlooks. It is not yet clear how many will fall in line behind the OECD's new-found optimism or even if that optimism is correct. But markets are reacting as though it is correct. They are optimistic. And yet there are plenty of obstacles still to be surmounted.

New day or new daze?

The election of Donald Trump in America and his pledge to make America great again is built on the back of promises to cut taxes and engage is fiscal stimulus. Elsewhere globally fiscal stimulus is being urged as well. Firming oil prices are bringing back some oil-field investment demand in the U.S. and stabilizing what have been cutbacks globally but OPEC is still struggling to get a grip on oil prices so that is still a major uncertainty not just for the U.S. but for all of OPEC and for any oil producer. For the record, lower oil prices did not seem to produce much in the way of net stimulus. Should they reappear, they may not be all that helpful. Also on the 'daze side' of the leger, there is the working out of risk and policy under Brexit which will create winners and losers and disruption. Potentially more damaging is the impact of the one-week away Italian referendum that could bring a separatist party to power if the referendum fails and Italian politics unravel. Italy's Five Star movement wants to exit the euro although most of Italy does not. There are also the potential for trade clashes as Donald Trump has pledged to claw back some advantage for already-signed trade deals. That could be disruptive. On the eve of a more aggressive U.S. trade policy, however, the WTO has struck its own blow saying the U.S. airframe giant Boeing has been receiving illegal subsidies. Let the games begin! Trade wars! The best defense is a good offense.

Banks as the roach motels of liquidity

Will deregulation save the day or mortgage the future?

One thing that has kept monetary stimulus from being effective has been the ceaseless move to step up regulation especially on banks. It's one of the reasons banks have been turned into monetary roach motels where the liquidity goes in but does not come out. Mr. Trump is going to scale back regulation in the U.S. and that could give banks control of their liquidity again- although the Fed still has its draconian stress tests. I wonder if there will be a broader global move to less bank regulation, and if so, that could reignite lending more than any central bank stimulus program.

Handicapping the future

Handicapping the future has never been more of a minefield. There are simply too many possible and very different scenarios to feel that one can have a good grip on what will happen especially at a time when so much that has been happening has fallen in the spectrum that ranges from unexpected to unimaginable. Political change is afoot in France as well. It would appear that in Germany Angela Merkel will remain entrenched. But the Middle East is a mess with Syria finally making inroads on Aleppo. Russia is meddling in the Middle East, stonewalling OPEC and still a source of uncertainty in Eastern European affairs. Turkey, having weathered a coup attempt, is showing new anger against the EMU for its exclusion and the West's unwillingness to extradite the people it wants to prosecute. Of course, I don't want to leave out Asia and its topsy turvy nature as China struggles to change gears and to develop domestic demand and to assert its beliefs on the world stage. Japan struggles to ignite any demand and inflation. India grapples with a self-administered monetary shock in the wake of its new currency 'reforms' that are proving very disruptive to small business in what is still largely a cash economy. The final 'BRIC' country on this list, Brazil, also is struggling. If anyone thinks they can see the future, it must be because they have a clear crystal ball or a good set of tarot cards because we know economic models are useless. Someday they will be back on track, but we have no idea when that will come. We face a great deal of uncertainty. But that it is not new. What is new is that we face it and markets have hope that things will be better. And that is the biggest shift of all.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief