Global| Sep 27 2016

Global| Sep 27 2016Euro Area Money and Credit Growth Bump Along

Summary

Throw in the kitchen sink, Mario The euro area remains largely unresponsive to all the central bank's efforts to revive it. Mario Draghi in his address to the European parliament's Economic and Monetary Affairs Committee noted that [...]

Throw in the kitchen sink, Mario

Throw in the kitchen sink, Mario

The euro area remains largely unresponsive to all the central bank's efforts to revive it. Mario Draghi in his address to the European parliament's Economic and Monetary Affairs Committee noted that the ECB would use all the instruments available within its mandate and urged others to do their share as he included comments about structural change and fiscal policy. This seems to echo remarks made by BOJ Governor Haruhiko Kuroda who just one day ago noted that Japan will use every available tool to hit its inflation target. This approach is far from being a new international theme, however, as the U.S. is preparing to pack some of its tools up into its tool kit and to declare success even as it is clear that its rebuilding project is not yet done.

Still in a world of hurt

Draghi emphasizes in his remarks that low rates are a result of poor growth and a poor recovery from the financial crisis. Italian banks are still not repaired and Germany's Deutsche Bank is seeing its shares pummeled to new lows on concerns about its capital adequacy as it faces a potentially large fine in the U.S. Clearly, it is still a very touchy environment; if the banks, the main financial intermediators, are still hobbled, it is going to be hard for ECB stimulus to work by acting through them.

Fresh data

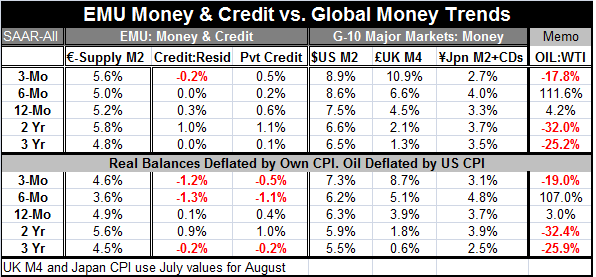

The fresh August money and credit data from EMU are telling. Nominal money growth (M2) has ticked up to 5.2% year-on-year, its best growth since March of this year but by a very small margin (5.3%). At 0.3%, year-on-year private credit growth is stuck at its July pace and it is below the near 2% growth rate it managed near the end of last year. Total private credit has ticked up to 0.6% from 0.5% (both year-on-year) But is also below the 2% pace it had been able to manage near the end of last year.

Short circuited?

On shorter horizons of three-month and six-month nominal money growth is slightly stronger and nominal credit growth is mostly steady to lower. Recalibrated as real balances money growth is flat to lower and credit growth is contracting on these horizons as well as being weak year-over-year. Stimulus is simply not getting through to end-users.

Other major monetary centers

In the other major monetary center countries of the U.S., the U.K. and Japan, the picture remains the same mixture it has been. Despite the U.K.'s Brexit fears, nominal U.K. money growth is accelerating. Of course, the BOE has taken some extra steps to provide stimulus as it is worried about the impact of Brexit on the U.K. economy. In the U.S., money growth has clearly stepped up over a series of horizons as well. Real balance growth in the U.S. and in the U.K. also shows acceleration. These results contrast with Japan where deflation continues to take root and where money growth simply has not been able to pick up. M2's year-on-year growth rate is the weakest in five months for both nominal and real balance growth in Japan. Trying as they might, the ECB and the BOJ have been unable to affect their respective financial environments as desired. Economic performance continues to suffer.

The oxymoron: Policy and Brexit

Draghi has weighed in on the Brexit issue, urging EU negotiators to keep Britain from having single market access unless it accepts freedom of movement. Of course, the U.K. just opted out of the EU because it wanted to control its borders. Draghi has aligned himself with a hardline group in the EU, but it is still not clear what 'no single-market access' will mean. And if the EU wants to damage its own growth prospects being as hard as possible on the U.K. is a good way to accomplish that goal. Draghi and the EU find themselves in a very difficult position. The central bank hardly seems likely to be successful in stimulating growth if it is going to use all its increasingly feeble monetary tools to stoke growth but is going to endorse a growth busting stance against one of the blocs largest trading partners, the U.K. Angela Merkel has sounded more conciliatory toward the U.K. than has Mario Draghi.

An increasingly hostile environment

There are international regulatory issues potentially spinning out of control as the EU is seen as targeting U.S. firms for taxes by nixing tax deals that U.S. firms have struck with EU members. Apple is the latest to be caught in that web. The U.S. is after Deutsche Bank for its role in the U.S. mortgage crisis and the U.S. justice department is reported to be trying to figure out how large a fine it can impose on Volkswagen without putting it out of business (for its emissions cheating). There is also a new U.S. Justice Department probe launched at Standard Chartered Bank for potential bribery activity in Indonesia. All of these things add up to more hostilities. It is not clear that the U.S. and Europe have some sort of tax and fine of tit-for-tat competition, but one could make a case for it. In any event, the environment is somewhat poisoned and that is not going to be good for growth.

Speaking of growth

The WTO has just cut its projection for world trade growth and for the first time in 15 years it expects global GDP to grow faster than global trade. Trade has been an important engine for growth although it has been a two-edged sword for some countries as so much activity has migrated to Asia where costs are lower away from G7 members. The environment clearly continues to shift in various ways. While trade is slowing, more trade deals are being proposed and there is more opposition to them. Not only is GDP growth slowing, making conditions less friendly for trade, but the geopolitical and regulatory environment both are more hostile. National tensions have arisen even among strong trade partners and traditional allies. It is perhaps a much more dangerous period than many investors seem to realize.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief