Global| Mar 11 2021

Global| Mar 11 2021Euro Area Manufacturing Is in Recovery Mode

Summary

Twelve of the earliest EMU members had reported IP for January. Only three of them showed a decline in January output month-to-month (Germany, Spain and Portugal). Sweden, a non-EMU country, also had an output decline. In December [...]

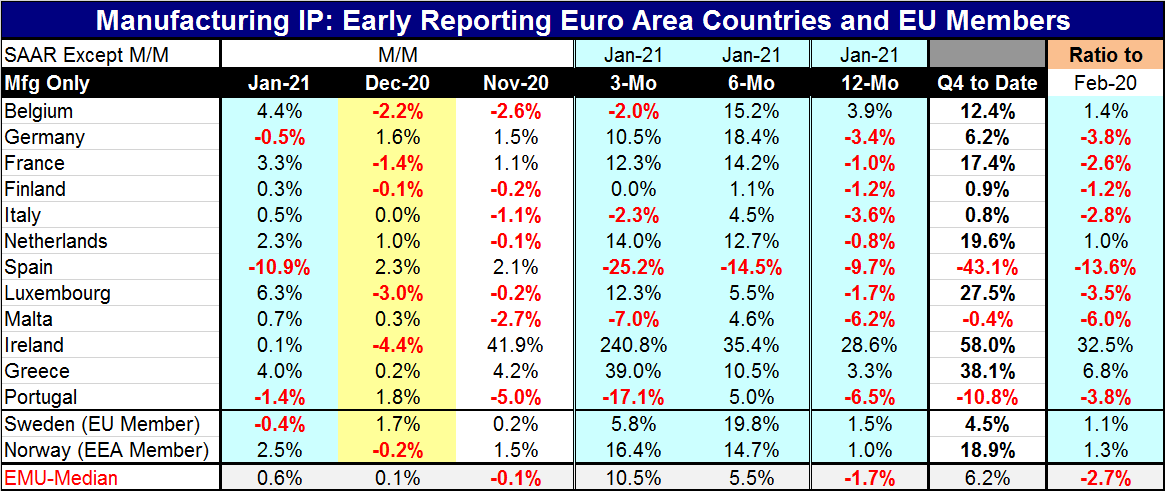

Twelve of the earliest EMU members had reported IP for January. Only three of them showed a decline in January output month-to-month (Germany, Spain and Portugal). Sweden, a non-EMU country, also had an output decline. In December five EMU members saw output fall; in November seven logged output drops. There has been steady progress in the manufacturing sector despite the fact that the virus has lingered and there are ongoing lockdowns in the EMU- policies vary by country, of course. The EMU rollout of vaccinations has been slow. Still, the median monthly gain of IP in the EMU has increased month-by-month.

Twelve of the earliest EMU members had reported IP for January. Only three of them showed a decline in January output month-to-month (Germany, Spain and Portugal). Sweden, a non-EMU country, also had an output decline. In December five EMU members saw output fall; in November seven logged output drops. There has been steady progress in the manufacturing sector despite the fact that the virus has lingered and there are ongoing lockdowns in the EMU- policies vary by country, of course. The EMU rollout of vaccinations has been slow. Still, the median monthly gain of IP in the EMU has increased month-by-month.

Looking at a broader timeline for 12-months to six-months to three-months, the progression shows the median change has improved from a -1.7% change over 12 months to a gain of 5.5% annualized over six months to 10.5% annualized over three months.

Over three months five EMU members log output declines, over six months there is only one decline, over 12 months there are nine declines. Over 12 months only Ireland, Greece and Belgium have output increases. Recovery from the Covid-19 shutdown is still a work in progress for most EMU members.

It is early in Q1 2021. With one month's data in hand, output is growing at a 6.2% annualized rate from the Q4 base according to the median of EMU members. Spain, Malta and Portugal are logging output declines early in Q1. Greece, Ireland, Luxembourg, the Netherlands and Belgium are logging increases in double digits; the small countries are posting some really elevated numbers. The largest EMU economies Germany (6.2%), France (17.4%), Italy (0.8%) and Spain (-43.1%) show varied performance.

Manufacturing continues to be the mainstay of recovery. And the virus continues to keep countries off balance. Fortunately, the manufacturing sector has been able to make progress in the face of virus outbreaks. But getting beyond that is going to be difficult and impossible without getting the service sector back on line and that brings us back to a discussion of vaccinations which are going slowly in Europe. Often the manufacturing sector is the harbinger of growth. But this time it is pulling a heavy anchor which is the still-restricted service sector.

The outlook is for continued growth. OECD has just upped its outlook. But a lot of that is on the back of the U.S. stimulus program that may be working by helping foreign economies as much as it helps the U.S. as U.S. consumers are going to be forced to channel most spending through the goods sector. The situation in the U.S. is the same as in Europe: jobs are in the service sector, recovery is in the manufacturing sector, and the service sector is still being restricted except in a few states that are opening up faster than the CDC would like (Texas, for example).

For what it's worth, health officials in the U.S. warn of a fourth wave of infection even as the U.S. vaccination program building on Operation Warp Speed is making great progress. There is uncertainty about whether the variant strains can trump or undo the progress being made by vaccination. The variants are loose in the U.S. and in Europe. It is hard to tell if health officials are just trying to scare people to keep them cautious or truly worried that the variants could trump all the progress that has been made. For now Europe is hampered by not having enough vaccine and seems still highly at risk to infection and to the variants. Recently we have seen squabbling and finger-pointing about virus availability and sharing in Europe. This is still only verbal and has not blown up beyond that. We are not done writing about the virus, unfortunately.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief