Global| Aug 21 2015

Global| Aug 21 2015Euro Area Makes Some Progress; Flash PMIs Advance

Summary

The euro area showed some progress for its private sector in August. The EMU PMI advanced to 54.1 from July's 53.9. It's hardly a rousing gain, but it keeps some sense of upward momentum in the indicator. In August the EMU [...]

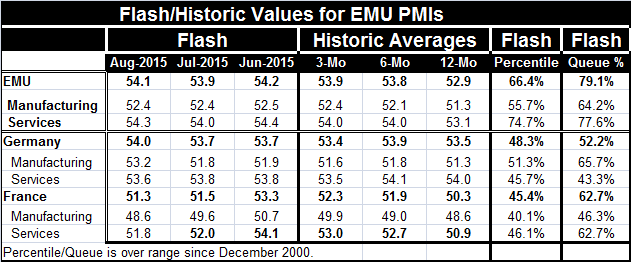

The euro area showed some progress for its private sector in August. The EMU PMI advanced to 54.1 from July's 53.9. It's hardly a rousing gain, but it keeps some sense of upward momentum in the indicator. In August the EMU manufacturing reading was flat at the July level while the services sector progressed by rising three ticks from its July level. Both sectors show activity is advancing as both have diffusion values above 50. The queue percentile standing for the overall private sector gauge is 79.1% with a manufacturing reading at 64.2% and a services reading at 77.6%. Note that the private sector standing is higher than either of its two components. This means that the combined strength of the two sectors is somewhat unusual.

The euro area showed some progress for its private sector in August. The EMU PMI advanced to 54.1 from July's 53.9. It's hardly a rousing gain, but it keeps some sense of upward momentum in the indicator. In August the EMU manufacturing reading was flat at the July level while the services sector progressed by rising three ticks from its July level. Both sectors show activity is advancing as both have diffusion values above 50. The queue percentile standing for the overall private sector gauge is 79.1% with a manufacturing reading at 64.2% and a services reading at 77.6%. Note that the private sector standing is higher than either of its two components. This means that the combined strength of the two sectors is somewhat unusual.

The chart shows overall that EMU manufacturing and services diffusion gauges, after being tightly linked since at least 2011, parted ways in 2014 and since have stayed on substantially separate paths. But both sectors appear to be on a gradual crawl to higher levels. Upward momentum, weak as it is, is still in place.

This is good news with China's manufacturing sector backtracking to a 77-month low in August. Japan's manufacturing PMI rose this month despite its strong economic connection with China. But the message on world markets is clear. Stock markets are falling and oil prices are falling. Markets are wary of the weakness in global demand.

Within the EMU we see mixed conditions in its two largest economies. Germany's private sector composite PMI stands at a diffusion value of 54.0 and in its 52nd historic queue percentile. France, with a lower PMI level at 51.2, has a higher queue standing at 62.7%. In this divergence, we see that while Germany is stronger in its raw diffusion gauge, it is still weaker than France relative to historic norms. Generally, Germany would be even stronger than France. The 62.7 French percentile standing does not mean that France is doing better than Germany. It means that it is doing better relative to its own history which is a much weaker history than Germany's history. French manufacturing diffusion is still below 50 at 48.6, signaling that manufacturing contraction is still in train. The French services sector at 51.8 is advancing. But both sectors are weaker on the month. Germany only saw improvement in manufacturing this month; services in Germany also weakened on the month. Clearly, from the data, we have in hand the upward momentum in the EMU remains a very mixed bag of ingredients.

The PMI view of the world remains a very subdued one. Europe has some progress in train, but even with Germany's composite doing better, the German GfK consumer confidence index for the month ahead, September, shows a backtracking. It also sports the weakest level for confidence since March of this year. Germany, Europe's leading economy, is still having issues and this is in a world where the euro weakness imparts a huge competitiveness gift to an already highly competitive economy with a huge current account surplus. Global demand is so weak that even Germany's economy is showing a feeble manufacturing sector. So the EMU has an uptrend. But it is weak and the trend is not impressive. Is it also vulnerable? And is Greece really on the mend or is it still an accident waiting to happen?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief