Global| Jun 12 2015

Global| Jun 12 2015Euro Area IP Slows to a Crawl in April But Holds to Solid Trends

Summary

Industrial production in the euro area has slowed to a crawl as ex-construction output rose by just 0.1% in April after a 0.4% decrease in March. Manufacturing output rose by a stronger 0.3% after a 0.2% March decline. Despite these [...]

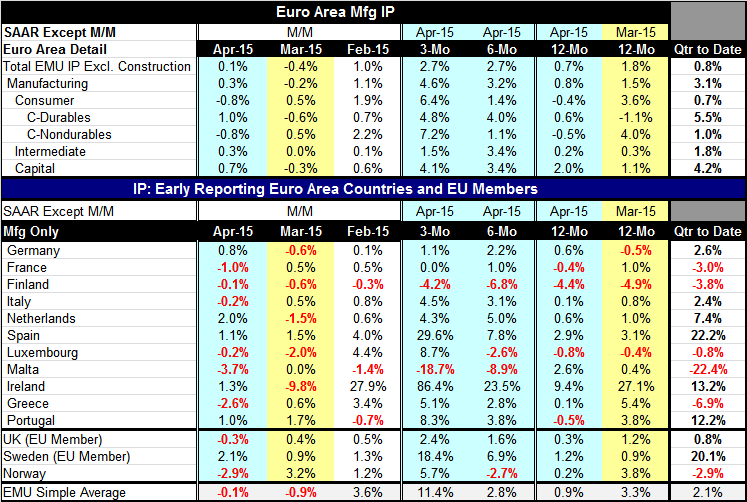

Industrial production in the euro area has slowed to a crawl as ex-construction output rose by just 0.1% in April after a 0.4% decrease in March. Manufacturing output rose by a stronger 0.3% after a 0.2% March decline. Despite these short-term irregularities, the EMU industrial sector appears to be on a solid path with consistent expansion.

Industrial production in the euro area has slowed to a crawl as ex-construction output rose by just 0.1% in April after a 0.4% decrease in March. Manufacturing output rose by a stronger 0.3% after a 0.2% March decline. Despite these short-term irregularities, the EMU industrial sector appears to be on a solid path with consistent expansion.

In the quarter to date, the headline series is rising at a 0.8% annual rate while manufacturing is sprinting ahead at a 3.1% annual rate. Manufacturing in the new quarter is hot despite lethargy over the last two months.

Sequential growth rates show that IP has picked up from growing by 0.7% over 12 months to advance at a 2.7% pace over three months and six months. That is a much steadier picture of Europe's industrial expansion.

In contrast, manufacturing is output is accelerating from growth of 0.8% over 12 months to 3.2% over six months to 4.6% over three months. Consumer goods output of durables and nondurables both are showing progressive acceleration. Capital goods output also is steadily accelerating. Intermediate goods output is growing but not accelerating. These are strong profiles

In the quarter to date, overall manufacturing, consumer durable goods and capital goods output are leading the way higher. On balance, the industrial sector, especially manufacturing, is looking much more solid despite some waffling in the past two months.

Turning to the individual members, there are IP decline in April in six of 11 early reporting members. There were declines in five of these members in March and in three of them in February. In the quarter to date, five of 11 members show IP falling on balance. But the latest quarter-to-date calculation is a thin one as we are only one month into the new quarter.

When we look at the difference between the monthly data and the sequential data (three-month, six-month and 12-month), we see that monthly weakness is really not a good indicator of broader weakness. Over three months, only two of 11 countries have IP declines. Over six months, three of 11 countries have IP declines. Apparently EMU countries have a great deal of variability in monthly IP, but over broader periods IP is steadily rising. And the sequential growth rates show that Finland has negative sequential growth rates across the board. While Malta has IP up over 12 months, it is lower on balance over three months and six months. The sequential weakness among EMU members is dominated by these two economies.

From these trends, we judge the country level data to be supporting the overall EMU reports on IP trends. Despite some very rough monthly numbers, IP in the EMU is steadily advancing. The big four EMU economics are showing the way ahead as of them only France shows a negative sequential growth rate over the last year (for year-over-year growth). The EMU manufacturing sector seems to have found its legs.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.