Global| Jun 10 2016

Global| Jun 10 2016Euro Area IP Shows Very Solid Gains in April

Summary

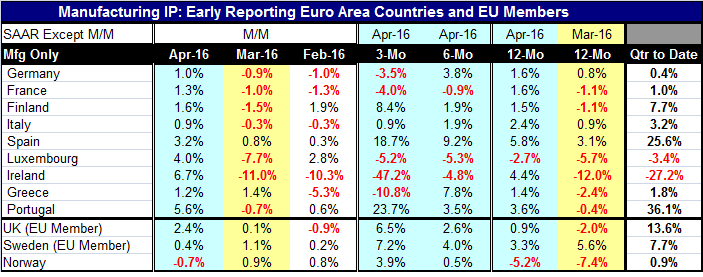

Industrial production rose in April in each and every one of the early reporting EMU members in the table. Month-to-month IP increases range from a low 0.9% rise in Italy to an outsized 6.7% gain in Ireland. These are very sizeable [...]

Industrial production rose in April in each and every one of the early reporting EMU members in the table. Month-to-month IP increases range from a low 0.9% rise in Italy to an outsized 6.7% gain in Ireland. These are very sizeable gains for month-to-month IP increases and certainly outstrip the message that we have been getting from the manufacturing PMIs for the period..but hold that thought.

Industrial production rose in April in each and every one of the early reporting EMU members in the table. Month-to-month IP increases range from a low 0.9% rise in Italy to an outsized 6.7% gain in Ireland. These are very sizeable gains for month-to-month IP increases and certainly outstrip the message that we have been getting from the manufacturing PMIs for the period..but hold that thought.

In part April is a recovery from a very troubled March in which seven of nine of these EMU members posted IP drops where drops ranged from -0.3% (Italy) to -11% (Ireland).

The underlying message here is that IP is not as strong as it seems in April nor as weak as it seemed in March.

Three-month growth rates tell the story of a still very uneven pattern of growth among EMU members. Five of nine countries show (annual rate) declines over three months, ranking from a -3.5% pace (Germany) to a -47.2% pace (Ireland). On the upside, Portugal is expanding over three months at a 23.7% pace, Spain at an 18.7% pace, and Finland at a 8.4% pace. All these countries are tied together in a single currency area. The `one ring to rule them all' would have a hard time controlling this lot. For the real-world ECB, it is a very tough job. But the real question is whether this unevenness with some very strong growth emerging is evidence that ECB policies finally are starting to take root.

Manufacturing PMI data for the EMU remain weak and uneven, but the year-on-year IP growth for April now shows gains in all these countries except tiny Luxembourg. Germany, France, Finland, and Greece show year-on-year increases in the low range of 1.4% to 1.6%. But Italy's 12-month gain is 2.4%, Portugal's is 3.6%, volatile Ireland's is 4.4%, and Spain's is 5.8%. On balance, growth is starting to look more solid. But remember that the PMI data are more topical and do not show this kind of revival continuing. The PMIs do show growth for the most part, but not very strong growth. Also recall that April is taking output sharply higher after March weakness. There could also be some overshooting here relative to trend.

Sequential growth rates patterns from 12-month to six-month to three-month show that French growth is deteriorating, along with Italy's and Ireland's. But growth is accelerating steadily in Finland and Spain. For the rest the group, a patterns show some degree of cross currents.

In the quarter-to-date, there is a small rise logged for Germany, a 1% (SAAR) gain for France, and much more solid gains for five other members. Only Luxembourg and Ireland show IP declines in the current quarter-to-date.

Overnight there were a few other reassuring reports as well. Japan's services sector logged a sharp rebound in April also after weakening in March. U.K. construction sector output rose for the first time in four months.

But there also are cautionary observations particularly about the recent sharp move lower for yields in Germany and the knock on effects these yield drops have had on the U.S. markets where investors are scrambling in to get a piece of high-grade government paper that still carries a positive yield. Make no mistake about it. The negative yields abroad are having impact on the U.S. markets. Any notion that the Fed can conduct a separate set of operations here that will not transmit its effects abroad is foolishly naive. Foreign growth is so weak and bond yields are so low and investor appetites so great that yields in the U.S. simply cannot rise. Of course, this sort of connectedness also means that the U.S. yield curve does not give us the same quality of signal about the U.S. market or economy that it used to. When governments play around with such vigor and presence in the debt markets, the signals get jumbled. You are well advised to remember that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief