Global| Jun 14 2016

Global| Jun 14 2016Euro Area IP Rebounds with Europe in Turmoil

Summary

Euro area industrial production rebounded by a smart 1.1% in April, more than recovering its loss of output in March but still behind its combined February-March loss. IP is still falling on balance over three months, but the six- [...]

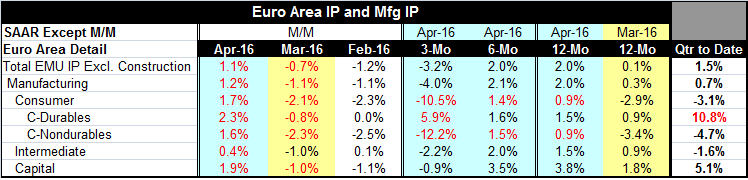

Euro area industrial production rebounded by a smart 1.1% in April, more than recovering its loss of output in March but still behind its combined February-March loss. IP is still falling on balance over three months, but the six-month and 12-month IP growth rate is locked at 2%. In the quarter-to-date, IP is rising at a 1.5% annual rate.

Euro area industrial production rebounded by a smart 1.1% in April, more than recovering its loss of output in March but still behind its combined February-March loss. IP is still falling on balance over three months, but the six-month and 12-month IP growth rate is locked at 2%. In the quarter-to-date, IP is rising at a 1.5% annual rate.

Manufacturing mirrors this sequence of events with output falling by 1.1% in March then rising by 1.2% in April but with a much deeper February-March drop than an April rebound. Manufacturing output is falling at a 4% pace over three months but relatively steady near growth rates of 2% over six months and 12 months.

Consumer goods output rebounded sharply in April after deeper declines in March and February. Consumer goods output as a result is a falling at an alarming 10.5% annual rate over three months but shows 1% or better growth over six months and 12 months. The rebound of output in April is somewhat reassuring looking ahead. Consumer durables output is being better maintained than for nondurable goods. Durable goods output is still expanding over three months while nondurables output is plunging at a 12.2% annual rate. Although IP data are expressed in `real' terms, the ratcheting of oil prices may have something to do with this volatility for nondurables.

Intermediate and capital goods follow these same trends with declines in March and weakness in February followed by a substantial rise in April. Output for both intermediate and capital goods is falling over three months and rising on earlier horizons. Capital goods continue to carry strong growth rates over six months and 12 months while intermediate goods trends remain moderate and expansionary.

These patterns are suggestive of disruptions at yearend that are being redressed in April as output recovers. Still, trends for output gains are no better than moderate. The ISM data are consistent with such a story except they show less of a rebound in train but are fully consistent with this legacy of past weakness.

The most recent data and surveys are showing a great deal of unrest in the most recent weeks as oil prices, the dollar, Brexit and negative interest rate trends are combining to create a potent cocktail of volatility and unrest. A lot of trends are in play that represent interrelationships and that feed off of one-another and seem to have done so in an adverse environment. Maybe we have to get past the period of Brexit vote before market conditions will settle down- if then. Until that happens, real trends are also going to be at risk. Output trends depend importantly on some of the financial variables, like exchange rates and to some extent stock markets and interest rates. Globally, politics and oil developments have taken on a huge degree of importance.

Brexit is simply the culmination of many forces that have come to bear on Europe and on either the EU or EMU as the rapid changes of recent years as well as adjustment tensions have made these sorts of bundled arrangements difficult to maintain. Everyone saw the advantages of the EU/EMU and few envisioned the kind of pain some members have suffered to stay in. Members can now see firsthand the sort of sacrifice and loss of sovereignty that might be required of continued membership. For the U.K. in particular, there is a lot in play, especially with London as Europe's financial center. The U.K. was able to weather the Scottish referendum. The Scotts had their `day in court' and decided to stay. Will the U.K. do the same with the EU or will there be a very different European future in front of us? It is an important question and it has implications for others that may decide to follow in the U.K.'s footsteps should it decide to go. The U.K. is not simply an `issue'; its decision could be a catalyst and that is the aspect putting markets on edge. There are real world real output ramifications. This is not just a financial market event to be handicapped in some betting forum. There are real world consequences at stake.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief