Global| Jan 15 2020

Global| Jan 15 2020Euro Area IP Is Weak; Germany Logs Its Weakest GDP Growth In Six Years

Summary

EMU area IP remains weak EMU area output gained just 0.2% in November after a 0.9% decline in October. Total output has negative growth rates over 12 months, six months and three months. The rate of decay of IP is not progressing, but [...]

EMU area IP remains weak

EMU area IP remains weak

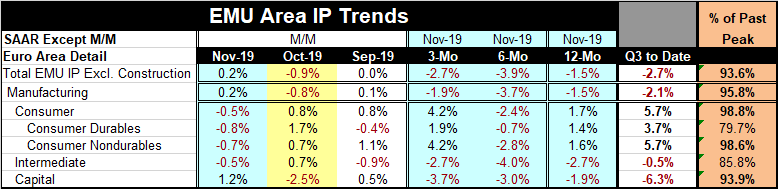

EMU area output gained just 0.2% in November after a 0.9% decline in October. Total output has negative growth rates over 12 months, six months and three months. The rate of decay of IP is not progressing, but it is continuing at a substantial pace. The three-month rate of decline is greater than the year-over-year rate of decline, but it is not as severe as the pace of the drop over six months. That could be a signal that the process of decay is abating or it could just be the result of uneven performance in a still-weakening economy. The growth rates for manufacturing alone show different growth rates than for the headline, but essentially the same pattern is evident with the same conclusions. The manufacturing profile is slightly less volatile than the headline profile.

QTD trends

Quarter-to-date both headline and manufacturing output are falling at a rate of greater than two-percent annualized. These are substantial declines. Current output is 93.6% of its peak value while manufacturing is 95.8% of its peak value.

Sectors by month

The composition on the decline in manufacturing output shows all sectors except capital goods declining in November after all sectors except capital goods advanced in October. September that shows a one tick gain in manufacturing output also had mixed sector results.

Broad sector trends

Consumer goods output is the only real strength in manufacturing. The output of consumer goods is up over three months and over 12 months with a decline over six months. The output of both the consumer durables and nondurables sectors shows an increase over 12 months and three months against a six-month decline. Intermediate goods and capital goods output in contrast both show declines on all three timelines: 12-months, six-months and three-months. Capital goods show a sequential output decline that is accelerating.

Sectors QTD

Quarter to date the sectors show consumer goods output and both consumer sectors growing strongly at rates from 3.7% to 5.7% annualized. Intermediate goods output is falling at a -0.5% annualized rate and capital goods output is falling at a substantial -6.3% annualized rate.

German GDP

Germany has just reported out its GDP for Q4 and it is the weakest German growth in six years. German GDP is up by just 0.6% from a year ago when it was growing at a 1.5% pace. However, this gain in output marks the longest string of GDP growth since Germany was unified. The current 0.6% growth rate compares to a ten-year average of 1.3%. In Germany, as with EMU IP, growth was driven by consumption. While capital formation in Germany was a positive factor in GDP, investment in plant and equipment in Germany was weak, echoing the weakness we see in EMU-wide capital goods output.

EMU-wide output trends

EMU-wide output trends

Year-on-year growth rates show that the big three EMU economies have tracked together in recent years until late-2018. At that time there came to be separation in their paths. From late-2018 French IP has performed the best in this group and currently has sustained an increase in output over 12 months. Italy recovered from extreme output weakness at end-2018 and is now logging only a modest decline in its year-on-year growth. Germany also experienced a great deal of output weakness at end-2018; it made a feeble recovery in early-2019 and then suffered a second round of weakness, leaving German output still severely impacted with a substantial decline in output year-over year in November, weaker than both Italy and France.

EMU trends

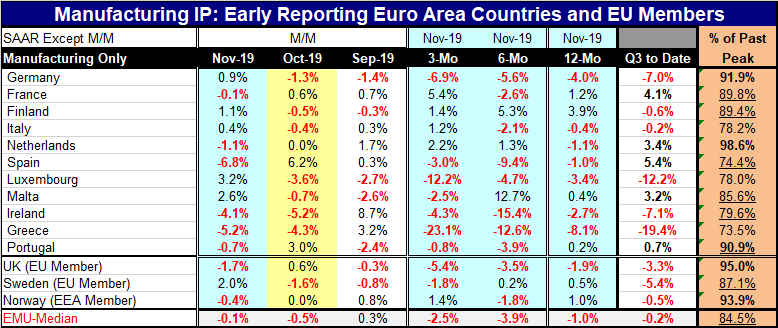

Across the EMU and several selected non-EMU nations, output has faced challenges. In the EMU, seven of 11 countries show year-on-year drops in output. EMU members France, Finland, Malta and Portugal manage year-on-year output increases. Seven countries show output declines over six months and three months. Among EMU members, Germany, Spain, Luxembourg, Ireland and Greece show output declines on all three timelines. Only Finland shows advances in output on all three timelines. For other Europe, the United Kingdom show declines in output over all three periods and its patterns show that its declines are deepening. In the EMU, only Germany, Luxembourg and Greece demonstrate a pattern of persistently weakening rates of growth. The Netherlands shows sequential improvement as a year-on-year decline is followed by progressively stronger six-month and three-month expansion rates.

EMU members QTD

For the quarter-to-date, there are six EMU nations with negative growth rates in progress; all three non-EMU nations in the table also show output contracting QTD. As we saw with reported German growth, the fourth quarter is going to be a difficult one.

EMU members in recent months

In the recent months, the patterns of weakness have continued with six EMU members showing declines in output in November, seven in October and five in September.

Overall assessment/outlook

On balance, this is still a picture of weak growth. In its GDP release today, the German statistical agency pointed to lessening pessimism and gains in orders as positive forces in its outlook. However, orders are fickle and for Germany manufacturing real orders actually fell in November and have negative growth rates (diminishing negative growth rates, yes…) from 12-months to six-months to three-months. German surveys from ZEW and the IFO have turned up and the Markit manufacturing PMI for Germany is up off its lows. But Germany shows only a flicker of improvement. German consumer confidence also remains off peak. And consumer confidence in Italy and France has been slipping.

Will trade be a positive in 2020?

Many hopes seem to be pinned to the expectation of positive collateral benefits from the U.S.-China trade deal that Donald Trump is signing today. While that deal represents more hope and a diminution of fears and tensions, there is not a lot of stimulus in that deal and there remain a lot of issues for the U.S. and China to sort out. The U.S. has recently announced that there would be no more tariff reductions until the U.S. elections are concluded in 2020. In this world, good news is where and when you find it. We may find some in 2020. But for now, there is a lot of reason to be wary and a good deal of danger in the air.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief