Global| Mar 12 2020

Global| Mar 12 2020Euro-Area IP Goes Whistling Past the Graveyard Are There Broader Lessons Here?

Summary

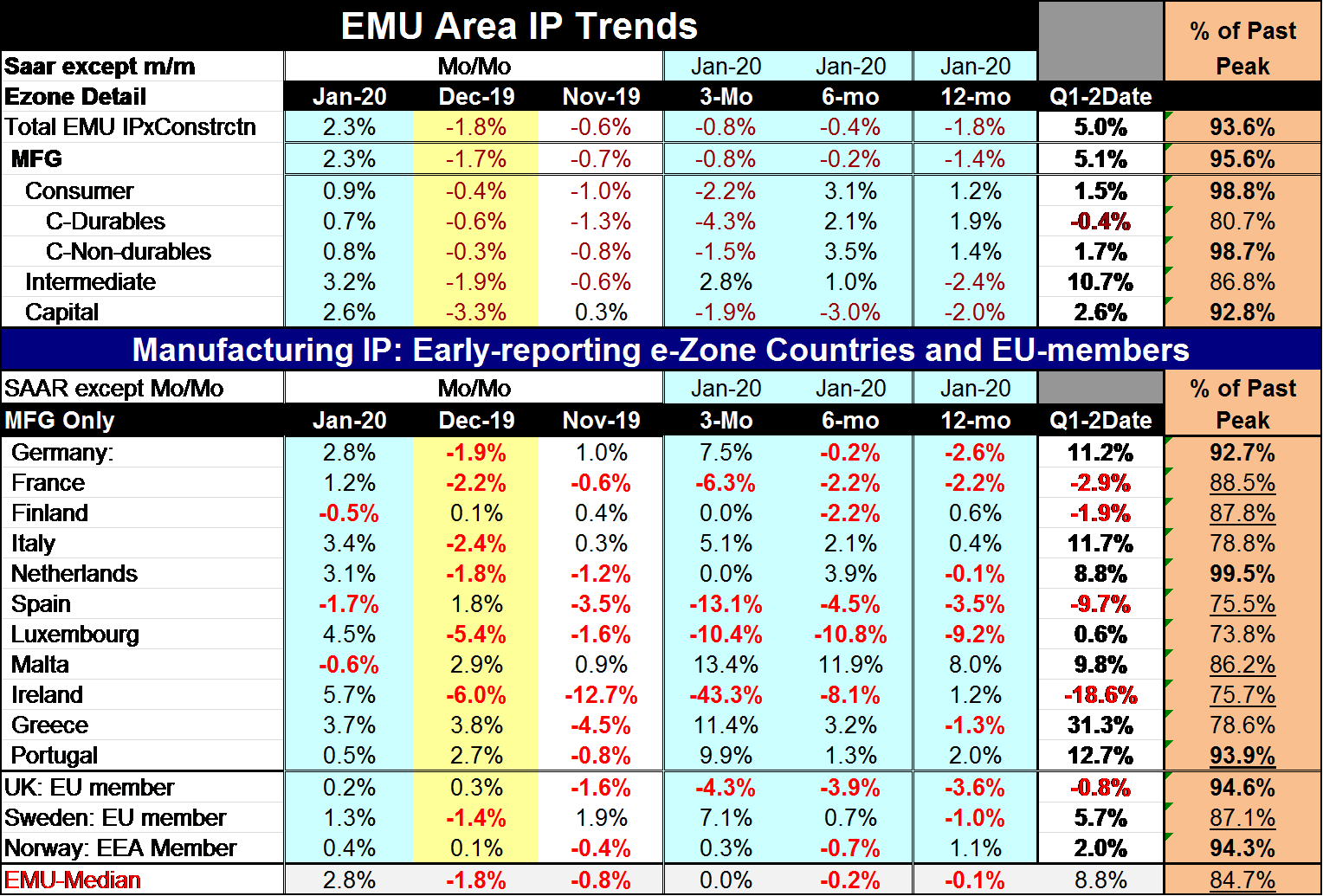

The EMU IP index rose by a sharp 2.3% in January; its first increase since September. Output gains registered across all major sectors… And they are not apropos of a trend. This is yet another report that has showed a pick-up in [...]

The EMU IP index rose by a sharp 2.3% in January; its first increase since September. Output gains registered across all major sectors… And they are not apropos of a trend. This is yet another report that has showed a pick-up in activity in January just before the coronavirus began impacting activity and affecting the outlook. While output is higher in January it is not a harbinger of things to come. Some reports even from February have remained solid or strong.

The EMU IP index rose by a sharp 2.3% in January; its first increase since September. Output gains registered across all major sectors… And they are not apropos of a trend. This is yet another report that has showed a pick-up in activity in January just before the coronavirus began impacting activity and affecting the outlook. While output is higher in January it is not a harbinger of things to come. Some reports even from February have remained solid or strong.

Growth over the past year

Sequential growth rates for EMU IP show negative growth rates across the spectrum from 12-months to 6-months to 3-months. That goes for manufacturing IP as well. Early in the first quarter with only one third of the quarter's data in, output is rising over Q4 in all major sectors and subsectors except for consumer durables.

Momentum

By sector sequential growth rates show few clear trends. Intermediate goods show output acceleration in gear but that sector stands alone; consumer goods as well as both subsectors for consumer goods have output increases over 12-months against declines over 3-months. Capital goods output is relatively steady with output declines in the 2% to 3% annual rate range.

By country

Of the 11 longest-standing member EMU countries in the table only Finland, Spain and Malta show month-to-month output declines in January; that compares to six declines in December and seven declines in November. Still four countries show net output declines over 3-months, six show declines over six months and six decline over 12-months. In the quarter to date only four countries have declines.

No harbingers here

As we have seen some statistics have even maintained strength through February. The US jobs report and the NFIB small business survey are two of them. Even Italy which we know became hard hit in late February and March shows strong output gains in January. Clearly these country statistics are not good indicators of where conditions are headed.

New world disorder

By now you have to live under a rock to be unaware of the coronavirus or to be unaffected by polices meant to contain it. The US is having a hard time deciding on a policy response. The ECB has taken steps but markets were not impressed with those steps.

Understanding 'the crisis'

However, I see no evidence of the authorities trying to guide opinion to expect that weakness is with us and will be with us for some time as we fight the impact of the virus. Slowing activity is one important way that the virus is fought. Very clearly the wrong thing to do would be to try to rev the economy up and power though the weakness since heating up activity would increase person to person exposure and accelerate spread of the virus. Actions that reduce person to person exposure weaken growth for now…but not the economy itself. The economy is not weakened by these actions- in fact if they succeed in damping the spread of the virus these policies actually strengthen the economy! The economy's ability to produce and expand is there but it is being artificially restricted to fight the spread of the virus. I would very much like to see world leaders emphasize this fact rather than to talk as if they are doing all they can to keep growth going- when clearly they are not, cannot and should not. If everyone were to realize that the global and individual economies are going to pause to deal with the virus and slow its spread - and that it's okay - the prospects of a fuller faster economic recovery would be much better. In the meantime policy needs to focus on helping those who are harmed most by the slowdown.

So this is my preferred way to think of this 'crisis.' There is a strategy. But it is not the usual one. This is not a Mario Draghi 'whatever it takes' moment. This is a moment to spread information and take things one step at a time, slowly, and deliberately.

Are we up to it? Is there any government or central banker anywhere willing to espouse such an approach out loud? Or are we so consumed with the pursuit of growth for the sake of growth that policymakers can only pledge to fight off the weakening effects of virus even though that might be the wrong thing to do?

Lessons while falling off the edge:

Corona meets trade war, oil war, and political acrimony

This is an unusual moment. It comes after an important US-China trade war that still lingers. It comes in the midst of a UK-EU Brexit negotiation. The slack global demand has caused an intra OPEC+ crisis and the Saudis have exploded the oil weapon even as they themselves stand at ground zero since they think that they can withstand the effects better than Russia who they are trying to get on board for output curtailment, ironically meant to raise oil prices. In the US a major four year election cycle is playing out after one of the most acrimonious political years in the US in over a century. The world is discovering that other countries' domestic policies also may harbor global issues; they are not a matter of national sovereignty alone as we can see by China's bungling of the virus that has led to a pandemic. Clearly, a nation's pollution is also a global concern. And these are concepts that just have not before been dealt with before as China and others, even after joining global organizations, have shown they will spurn them when the global decider organizations' opinions are not what they want. This is most famously evident in China's South China Sea grab.

However, China now is angry at the US for blaming it for letting this virus get out of control. But the US criticism is right on the money. We all know it. We saw it happen. We saw China suppress those who tried to sound the early warning. But China now would use its economic power and political might to rewrite history and to bury its role in this. Instead, we need to remember. We need to learn.

There needs to be real rules for fair play and openness. One thing I am watching now is Iran's request for $5bln from the IMF to fight the coronavirus after it derided the disease here, called it a Western hoax and let it spread. The US has been trying to starve Iran of oil revenue to force it to re-negotiate its nuclear deal and to stop its political interference in the Middle East. Will the IMF so easily fork over $5bln and 'trust' that that money will go to the corona virus fight in a country where the leaders have shown not much concern for the welfare of their people and even turned loaded weapons on them when they protested? Keep an eye on that one…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief