Global| Oct 12 2016

Global| Oct 12 2016Euro Area IP Gains

Summary

There has been a noticeable lull in manufacturing over the past year. It is not just Europe or just the United States. The Markit PMI data confirm a global slowdown with low PMI readings being endemic to the global economy. Global PMI [...]

There has been a noticeable lull in manufacturing over the past year. It is not just Europe or just the United States. The Markit PMI data confirm a global slowdown with low PMI readings being endemic to the global economy. Global PMI data have been sluggish for the past year with only a very modest uptrend in place for the global system. However, there is evidence in the PMI data that manufacturing and services are now starting to mount a very gradual revival from their weakest recent readings. IP has been languishing at weak growth readings since 2011 with only fits and starts of any strength exhibited. In the EMU, this month manufacturing shows signs of a developing breakaway (see charts).

PMI data vs. IP data

The PMI data are easy to read because their evolution has been gradual and the trends are clear. The IP data are harder to read because they are volatile and sectors as well as countries show divergent trends.

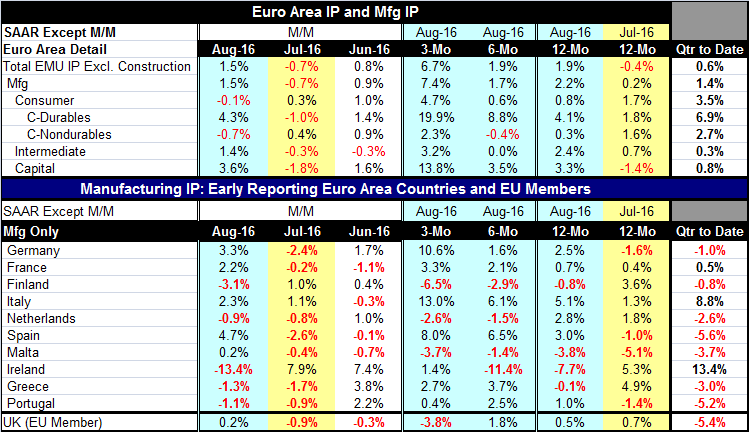

Sharp recoveries

In the EMU, there is a sharp recovery developing in IP from Italy and Spain. Unfortunately, the two large EMU economies have the most variability in their IP among the big-four EMU economies (Germany, France, Italy and Spain) and the U.K.

Consistent growth and emerging Q3 growth

Italy and Spain have three-month growth rates of IP at a 13% annual rate and an 8% pace, respectively. Germany's advance over three months is similarly strong at over a 10% pace. Germany, France, Italy, Spain, and Portugal each have logged consistent positive output increases on all key horizons in the table (three-month, six-month and 12-month). But in the quarter-to-date (two months of data are in for the third quarter), the annualized pace of growth is positive only for Ireland, Italy and France. Only Italy shows a strong gain. France shows a weak 0.5% pace of increase as it has a gain in output preceded by two drops. Ireland's recent performance is bizarre with back-to-back month increases of more than 7% month-to-month followed by a month-to-month drop of 13.4% (ironically the same pace as its annualized quarter-to-date gain).

Divergent monthly data

Output is falling in August in half of the reporters in the table; it is falling in 7 of 10 countries in July and in four of ten in June. Country level signal remain tenuous.

EMU data show consistency

Pooling the data together in the weighted format for the euro area brings more consistency and even strength to the report. All EMU sectors show quarter-to-date gains. Only consumer goods output falls in August and that is generated by weakness in nondurables. July was a weak month with overall EMU IP which fell by 0.7%; there was also a 0.7% drop in manufacturing and weakness in all three major sectors. Output in July fell for consumer goods, intermediate goods and for capital goods. Capital goods output is rebounding strongly in August with a drop in July sandwiched between two sizeable monthly gains. Capital goods output is advancing at a 13.8% annual rate over three months, a strong accelerating gain from a previous firm path that shows growth had been running at about 3.5% pace over 6 months and 12 months. However, even these comparisons are not well entrenched as in June the year-on-year pace for capital goods output was a drop of 1.4%.

Capital goods

The capital goods sector is an important one; with global slack, there has been less need for capital investment in this expansion. Germany, a key capital goods producer, has seen its capital goods output falling two of the past four months. German output and industrial order growth both have stayed at a year-over-year growth rate of 2.6% or less over the past year. The capital goods sector in Italy has been gaining strength while in France capital goods production is declining on all horizons.

Growth is the key

Global growth will be the key to the improvement of manufacturing and especially to the revival of capital goods output. What is hard to see right now is what will drive that revival. Germany seems to be affected less by any competitiveness issues than it is by special factors or just 'bad luck.' Germany is a highly competitive economy and capital goods is a traditional sector of strength. Germany is more likely being affected by being at the wrong place at the wrong time. The oil sector has been cutting back, China has slowed and Russia has been red-lined because of sanctions related to its military hostilities. Add to that the ongoing global weakness and still relatively low rate of capacity utilization and there it is, your formula for weakness in Germany.

Is a sustainable revival underway?

The global PMI data suggest that revival already is underway and perhaps we could call the cause of it 'organic' growth as there does not seem to be any special stimulus behind it. Central banks are pushing to provide all the monetary stimulus they can and without any real noticeable effect to date. Financial institutions are poor intermediaries as many have impaired balance sheets. Elsewhere where banks are in better shape regulators are hovering over them subjecting them to stress tests and increasing the load of capital they must carry. Fiscal policy has for the most part been held in abeyance. This could be critical time for manufacturing. If this global revival can be nurtured it could be growth saving. If it fails to endure it could lead to our next downturn and perhaps another period of great difficulty since central banks' tools have been so blunted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief