Global| Nov 14 2016

Global| Nov 14 2016Euro Area IP Falls in September; Year-on-Year Gain Slows

Summary

While manufacturing PMIs have stabilized and showed some growth in the EMU, the industrial production index is lower in September and has fallen in two of the last three months. IP is up on balance over 12 months, but the last 12 [...]

While manufacturing PMIs have stabilized and showed some growth in the EMU, the industrial production index is lower in September and has fallen in two of the last three months. IP is up on balance over 12 months, but the last 12 monthly changes in manufacturing IP are split evenly between showing gains and declines month-to-month.

While manufacturing PMIs have stabilized and showed some growth in the EMU, the industrial production index is lower in September and has fallen in two of the last three months. IP is up on balance over 12 months, but the last 12 monthly changes in manufacturing IP are split evenly between showing gains and declines month-to-month.

PMIs vs. IP

The PMI gauges are indicators from which we draw inferences about how industrial output is behaving and how the factory sector in performing. Those gauges include measures of output, of prices, of the sector employment, circumstances of order delivery lags and order back logs. But the actual output is best measured here by the IP indices themselves.

Manufacturing

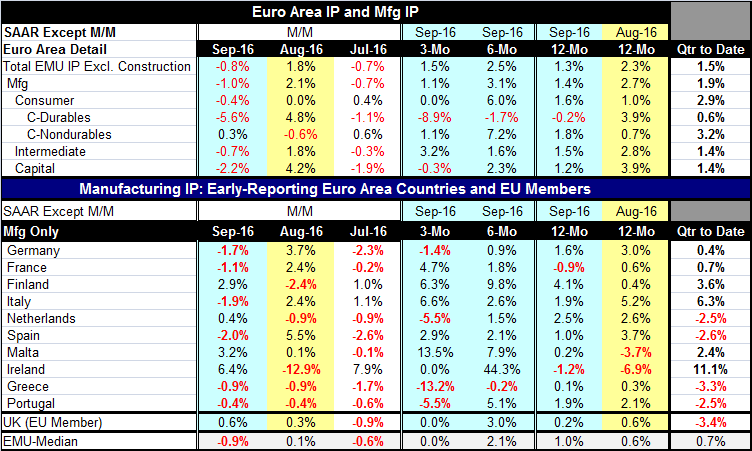

For manufacturing IP is lower on balance in the euro area by 0.8% and output has fallen for the second month in a row. Even so the output gain in August dwarfs the summed two months of declines in the adjacent months of September and in July. Over three months manufacturing output is rising at a 1.1% pace while it is up at a 1.9% annual rate quarter-over-quarter (which means quarter average over quarter average).

Consistent inconsistencies

But output declines are widespread across sectors in both July and in September just as the rebound in the middle month of August is strong across most sectors.

Sector and overall trends

Manufacturing trends are not exactly clear with output up by just 1.4% over 12 months and at a weaker 1.1% annual rate over three months but hopped up to a 3.1% pace over six months. Consumer goods show that same lack of consistent trend. But for consumer durable goods, the pattern is clear and there is a substantial weakness and erosion in output with its three month drop at a -8.9% annual rate. Consumer nondurable output gains 1.8% over 12 months, is at an even slower 1.1% expansion over three months but pops to a stronger growth rate over six months, just like the headline for IP. Intermediate goods show a steady escalation in growth rates at 1.5% over 12 months, rising to a 3.2% annualized pace over three months. Capital goods show a 1.2% gain in output over 12 months and accelerate to a 2.3% pace over six months then slow to show a 0.3% annual rate contraction over three months. On balance, the sector still looks like it is struggling. It is certainly not very encouraging that intermediate goods alone are the sector that shows that momentum is building since intermediate goods have to be used elsewhere and capital goods and consumer goods trends are both at loose ends.

Q3 shows modest gains

In the just completed third quarter, output gained at a 1.5% pace led by consumer goods which in turn are helped by nondurable goods usual the noncyclical component. Intermediate goods and capital goods each are up at a 1.4% pace in Q3.

Ongoing growth evaluated

If we evaluate sector performance over the past six years, consumer durable goods show the weakest performance standing at only the 89th percentile of their six-year range of values, nearly 11% off the peak. Manufacturing IP is at its 99th percentile, one percentage point off its peak. Consumer nondurables output is about 2% off its peak while intermediate and capital goods each are about 2.5% off their respective six-year peak values of output. The sector shows the greatest weakness in consumer durables, and if times were improving, we would expect that sector to lead not to lag so badly.

Recent country by country trends

The results by country are similarly disappointing. Looking at the performance of the 10 early EMU members plus the U.K., we find six declines in output in September after seeing five of 11 countries post output declines in August. Over three months, only five show increases of any kind as two show output is flat and four show output is lower on balance over three months. In line with the aggregate EMU data over six months, most countries demonstrate stronger performance and output gains with the only decline coming from Greece. Over 12 months, IP is lower on balance in France and in Ireland with a weak 0.1% gain in Greece and another weak 0.2% gain in the U.K.

Ongoing trends for countries

On longer trends, Ireland, Greece and Italy are the most lethargic with IP levels in September that are 10 percentage points or more below their respective six-year peaks. France, Finland and Spain have output levels that lag their six-year peaks by 5% of more. Portugal, Germany and the Netherlands are each within 2.5 percentage points of their respective six-year peak production index.

Summing up: still mixed and lethargic

On balance, the EMU sees a great deal of variability in recent momentum as well as in ongoing performance among members. While Germany has strong ongoing performance, there is nothing in its recent momentum that stands out. The Netherlands, Portugal, Finland and Italy each has stronger 12-month gains in output than Germany and Germany is one of only four countries in the table with output declining over three months on balance. As the usual strong economy of Europe, Germany is not pointing to any breakout although growth is still in gear. Europe appears to continue to muddle ahead without a clear sector or country leading it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief