Global| Nov 12 2015

Global| Nov 12 2015Euro Area IP Falls for Second Straight Month

Summary

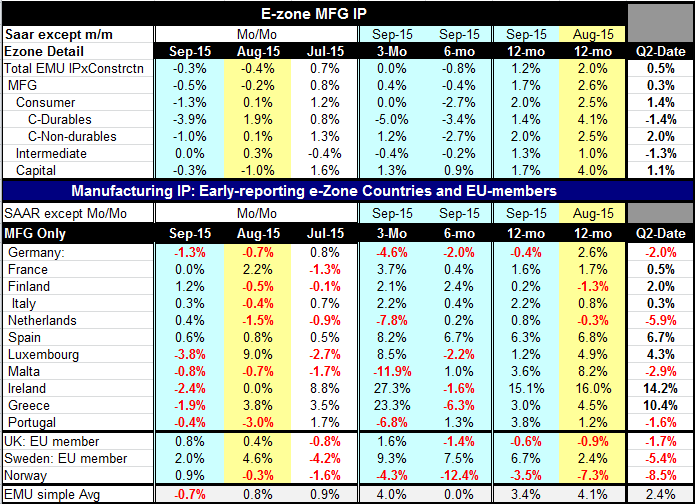

Euro Zone IP fell by 0.3% in September after dropping by 0.4% in August. Manufacturing IP also has been falling for two consecutive months. Although the EMU-Area MFG PMI is above the "boom-bust- line" of 50, IP in the Zone is falling. [...]

Euro Zone IP fell by 0.3% in September after dropping by 0.4% in August. Manufacturing IP also has been falling for two consecutive months. Although the EMU-Area MFG PMI is above the "boom-bust- line" of 50, IP in the Zone is falling.

Euro Zone IP fell by 0.3% in September after dropping by 0.4% in August. Manufacturing IP also has been falling for two consecutive months. Although the EMU-Area MFG PMI is above the "boom-bust- line" of 50, IP in the Zone is falling.

Overall IP growth is flat over three-months and falling at a pace of -0.8% over six months. It is rising by 1.2% over 12-months and is snaking higher at a 0.5% pace in the just-completed third quarter.

In manufacturing industrial output continues to be underpinned by the capital goods sector where output is rising all horizons from 12-mo to 6-mo to 3-mo, even though it has fallen for two consecutive months. Capital goods IP has decelerated from a 1.7% pace over 12-months to 1.3% over three-months. Consumer goods output is up by 2.7% over 12 months but is flat over three months and falling over six months. Both durable goods and nondurable goods show erratic trends for consumer goods output. Intermediate goods output is clearly decelerating and is contacting on balance over both 6-months and three-months. EMU seems to have nearly all its eggs in its capital goods basket.

Germany is not providing leadership except in the direction of weaker. German IP is decelerating on a clear path from 12-mo to 6-Mo to 3-Mo with output falling at a 4.6% pace over three months and falling at a 2% pace over six months and dipping by 0.4% year-over-year.

Spain, the fourth largest EMU economy, is the only one showing a steady acceleration in output. But France, Italy, Finland, Ireland and Greece show gains over 12-months and stronger growth over three months albeit with some weakness in between.

Germany is the only country with MFG IP falling over 12-months. Over three-months and six months only four countries show IP declines- and one of them is always Germany.

The recent weakness in IP is undeniable and much of it is in the manufacturing sector despite a highly competitive euro exchange rate. Germany, which traditionally is the strong economy of EMU, is now a sinking force, pulling down overall IP growth in EMU. The weakness in China has greatly affected German exports and output. Now Germany needs to brace for the shock of the future as Volkswagen will have to survive some very harsh medicine from various global authorities where it has flaunted environmental rules.

In a global environment where growth is so weak it is fair to wonder how long the EMU capital goods sector can remain that strong. With weak growth there will not be the same pressure to expand and add to add capacity. Capital goods demand could wither. Just today U.K. aerospace giant Rolls Royce announced a sharp drop in demand that would necessitate cut backs there. For now the capital goods sector is still the backbone of EMU manufacturing output. While some speak of a Europe that is gaining strength, we do not see it here. The sense of improvement in EMU has been limited. While growth is still "hanging around" there is precious little sign of any acceleration. The manufacturing sector is weak and the economy is being supported by its service sector. And there are further shocks to come. This is a less than dynamic situation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief