Global| Apr 14 2021

Global| Apr 14 2021Euro Area IP drops in February

Summary

Industrial production fell by 1% in February in the euro area. Consumer goods output ticked higher while the output of capital goods and intermediate goods fell. Of the 12 early-reporting EMU countries listed in the table, seven [...]

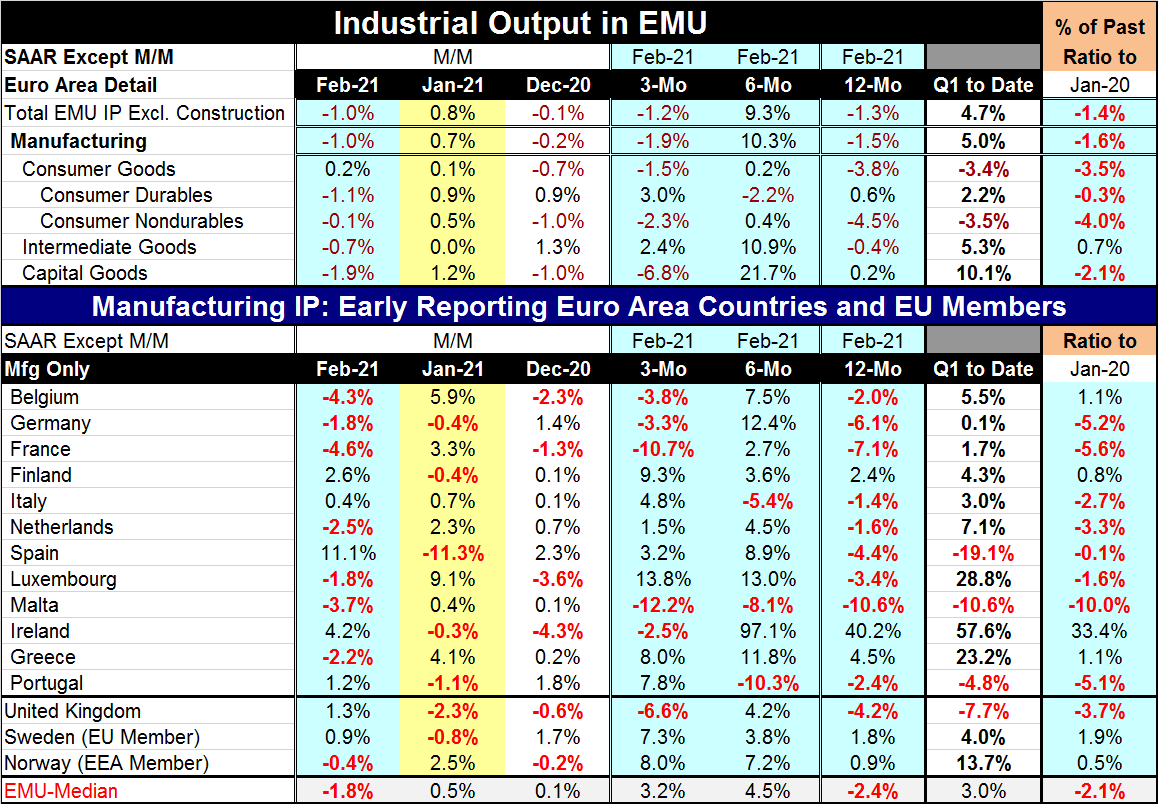

Industrial production fell by 1% in February in the euro area. Consumer goods output ticked higher while the output of capital goods and intermediate goods fell. Of the 12 early-reporting EMU countries listed in the table, seven posted declines in manufacturing output in February. The median change in IP among members was -1.8% month-to-month. However, the average drop among the seven countries with IP dropping was -3% on the month; the average gain among the five countries with IP rising was 3.9%. In truth, although manufacturing output in the EMU (which is size-weighted by country) shows a drop of 1%, there exists a real mixture of solid ups and downs for IP among these reporting EMU members in February.

Industrial production fell by 1% in February in the euro area. Consumer goods output ticked higher while the output of capital goods and intermediate goods fell. Of the 12 early-reporting EMU countries listed in the table, seven posted declines in manufacturing output in February. The median change in IP among members was -1.8% month-to-month. However, the average drop among the seven countries with IP dropping was -3% on the month; the average gain among the five countries with IP rising was 3.9%. In truth, although manufacturing output in the EMU (which is size-weighted by country) shows a drop of 1%, there exists a real mixture of solid ups and downs for IP among these reporting EMU members in February.

Over three months these metrics are reversed in some sense as five countries show declines while seven show output increases. But since the declines are lodged in the large countries overall IP and manufacturing IP for the euro area still decline at a 1.9% annual rate over three months. Over six months only Italy, Malta and Portugal show output drops with the rest showing increases; as result EMU manufacturing IP rises at a 10.3% annual rate over six months. The 12-month change takes us to February 2020 as a base for the calculation, just before the virus struck. Relative to that position, IP is lower in all countries except Finland, Ireland and Greece. Manufacturing IP in the EMU is lower over 12 months by 1.5%.

By sector, consumer goods output is lower over 12 months by 3.8% with intermediate goods output lower by 0.4% and capital goods output a few ticks higher rising by 0.2%.

Data are for February; this brings us to the two-thirds mark for the quarter. The quarter-to-date annualized growth rates show IP up at a 4.7% growth rate and at a 5% pace for manufacturing. Consumer goods output is falling at a 3.4% annual rate led by weakness in nondurable goods output. Intermediate goods output is rising at a 5.3% annual rate with capital goods output rising at a 10.1% annual rate.

Among EMU members the QTD median growth rate is 3%. Despite ongoing problems with virus infections and issues surrounding some of the vaccines that Europe has leaned on, output has been recovering in Q1 2021. Only Spain, Malta and Portugal show manufacturing output declining on a QTD basis.

The bottom line is that it is the same old story. Except I still don't know which story to tell. As the data show, there has been an ongoing recovery. But output is still not yet recovered to its pre-virus levels. And once it gets back to that, it has to rise enough to get back on its former growth path (if it can) to be called normal. Economic sectors and businesses have to be reinstalled in the economic matrix of life. In short, there is still a long way to go - much longer than what a 1.3% drop in year-over-year output speaks to. And then there is the question of how to get there with two vaccines currently in abeyance because of dangerous side effects. There are also variants of the virus in play, some of them quite dangerous and, given the way this virus has spread, potentially able to recirculate and wreak more havoc. We simply do not know. The economy is split between epidemiologists who seem to always fear the worst and those who think they see the light at the end of the tunnel and return to normalcy as imminent. Reality is bounded by these two views and for now we are not sure where it lies. February's IP report is a warning. January's report was a slice of hope. We can't be sure what March will bring, but lockdowns are being dismantled in April and time will tell how that works out.

There is a great deal of hope especially in the U.S. with a massive stimulus being launched there. But in Germany, the outlook by the research institutes has just been scaled back. According to a news report, Germany's economic institutes will cut their joint 2021 growth forecast for that country to 3.7% from 4.7% previously, due to a longer than expected covid-19 lockdown. This decision is being reported, but it has not yet been formally announced. While there is optimism, there is also some back-tracking and clearly a sizeable dollop of risk. Planning for the period ahead remains difficult. The future remains as elusive as ever.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief