Global| Jan 18 2017

Global| Jan 18 2017Euro Area Inflation Turns Higher

Summary

The chart features the year-on-year inflation result in the three largest EMU economies as well as the economy-weighted result for the EMU itself. Inflation is turning higher in each of the countries in the chart but at different [...]

The chart features the year-on-year inflation result in the three largest EMU economies as well as the economy-weighted result for the EMU itself. Inflation is turning higher in each of the countries in the chart but at different paces. Ironically, the EMU and Germany are showing a faster pace of inflation than is France or Italy or even Spain. Germany has the second fastest pace of year-over-year headline inflation among original EMU members; only Belgium's gain is faster.

The chart features the year-on-year inflation result in the three largest EMU economies as well as the economy-weighted result for the EMU itself. Inflation is turning higher in each of the countries in the chart but at different paces. Ironically, the EMU and Germany are showing a faster pace of inflation than is France or Italy or even Spain. Germany has the second fastest pace of year-over-year headline inflation among original EMU members; only Belgium's gain is faster.

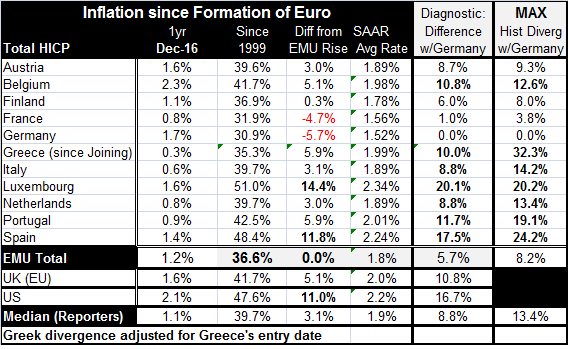

We flagged this tendency last month and continue to believe that faster than EMU German inflation will lead to more discord over policy within the ECB. With German inflation at 1.7% (y/y), it already is above the pace inflation has averaged in Germany since the EMU was formed (1.5%). While the old Bundesbank rule was the same as the ECB rule for inflation of just under 2%, at 1.7% and rising, the Germans will be worried about overshooting. The inflation pace in the EMU is still only at 1.2% over 12 months, but that will be hot enough to worry Germans given the sudden onset of the acceleration and the ongoing push to inflation from oil prices with OPEC's coalition staying intact.

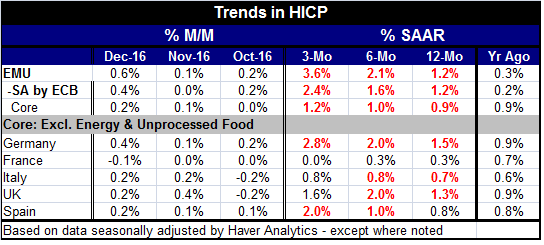

Core inflation, which has no official standing as an inflation target in the euro area, nonetheless is advancing over 12 months at the same pace as the headline. It has a slower pace of acceleration over six-month and three-month, than does headline inflation, however. This slower pace underscores the role of oil as the principal acceleration factor in the headline HICP. However, Germany, which also has the best performing economy in the EMU with the lowest unemployment rate, has a core inflation rate of increase that is accelerating from 12-month to six-month to three-month and is the fastest rising pace among the largest EMU economies. Germany also has the second fastest rising core rate among all the original EMU members in December after ranking third in November with the German pace then only surpassed by Austria and Belgium. In December, Luxembourg has the fastest rising core. Interestingly, in December, the lowest rising core inflation paces over 12 months are in Ireland, Portugal, Italy and Greece; now there's a 180 degree shift for you. And just to stir the pot a bit more on the policy front, these are generally the countries with the highest unemployment rates that will want policy to remain accommodative longer. Unleash the policy Kraken!

Of course, Germany is going to push the argument on inflation with the pace now getting closer to 2% (over the 1% mark at last) and will be looking to end all the special stimulus programs of the ECB. But Germany's own country level predicament is actually more precarious than that for the euro area overall. Although PMI data suggest that EMU-wide growth is picking up and that is true even for France whose economy has been lagging badly, EMU-wide growth is still tepid and inflation is not as threatening in the EMU area excluding Germany as it is in Germany itself.

Although core inflation is not an 'official' metric of the EMU, the fact that the German inflation is stubborn and rising so fast and gaining in its core measure as well is likely to have some impact on the way Germans look at the budding inflation pressures. Even though the German experience does not seem to be representative of inflation in the EMU or in the other large EMU nations, we can expect it to remain a focus for Germans.

The ECB's reaction to this spurt in inflation inspired by oil as the OEPC cartel manages to continue to hang together is going to be an interesting development to watch. The ECB is a single-mandate central bank.

Elsewhere, in the U.S., the rise in inflation is being closely watched as the Federal Reserve has a core PCE measure it tracks, but it continues to focus policy attention on the PCE headline. Policy is going to have to decide how much of this rise in the relative price of oil is an issue to which it needs to respond or not. It also will have to form some judgement about the sturdiness of growth and the economy's ability to withstand any monetary 'shock.' Of course, these are issues in the U.S. and for most other central banks, but the growth/inflation tradeoff will not be a direct issue for the ECB which has only an inflation target. Nonetheless, policy discussions at central banks around the world are going to get more interesting and more contentious. And even if ECB members can't argue this case in terms of growth concerns, those concerns will color how much danger some members see from inflation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief