Global| Oct 11 2013

Global| Oct 11 2013Euro Area Inflation Trends and What They Really Mean

Summary

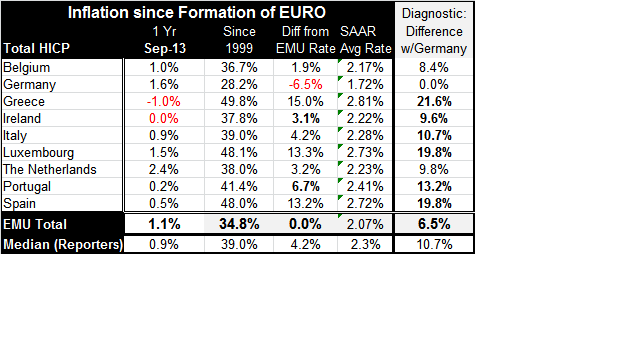

The inflation situation in the European Monetary Union tells a lot about the ongoing stresses and strains in the system. The chart on the left shows the inflation performance for a group of countries that have had economic [...]

The inflation situation in the European Monetary Union tells a lot about the ongoing stresses and strains in the system. The chart on the left shows the inflation performance for a group of countries that have had economic difficulties. We call this group `troubled borrowers.' It consists of Greece, Portugal Spain and Ireland.

What the dropping inflation data tell us is how much stress has been mounted in these regions to knock inflation off its previous trajectory. It is quite hard for a country to reduce its inflation rate in a short time without adverse effects on growth. What we see in the chart, is how much the troubled European economies in EMU are still struggling. There is some revival in their economies as we can see by recent PMI data. But, for these countries, PMI readings are still weak, even if they are improving.

The chart on the right notes that the drops in inflation in the larger countries are significant but are not form the same levels as the troubled borrower nations. Italy's inflation has fallen from a peak of about 4% to below 1%. France has seen its rate fall form about 2.75% to about 1%. In Germany inflation peaked briefly at 2.9% and has fallen to a year-over-year pace of just 1.4%.

The Netherlands and Germany have seen inflation drop from its peak year-over-year pace by just 1 percentage point to 1.3 percentage points. Greece has seen inflation drop from its peak by 6.8 percentage points and Portugal by 3.8 percentage points. These drops can be seen as indicators of stress. Of course, they reflect inflation progress, but they also reflect a price paid in terms of stress.

One aspect of Europe's situation is that Germany has gone from being the country with the lowest inflation rate to having the second highest year-over-year inflation pace in this group of nine countries as of September 2013. Germany's pace is above that for EMU as a whole and above the median for this group. But Germany's inflation rate of 1.6% is still below its average annual rise since EMU was formed (a gain of 1.7% per year).and that average is the lowest of any country in EMU. Germany is not really doing anything differently than before. It has become one of the high inflation countries because inflation in its fellow members has fallen so rapidly and so dramatically. And, might I add, so unsustainably.

Does anyone think that this is a new reality or that it can continue?

Greece, Luxembourg and Spain have run inflation excesses with Germany resulting in price levels that are now about 20% higher than those in Germany compared to when EMU was formed. Despite all their recent hard work, these nations -and others, have accumulated a severe competitive disadvantage vis-a-vis Germany. Since Luxembourg is a financial center its competitiveness loss is probably not a problem. But for Greece, Spain and others competitiveness remains an issue. These nations have suffered enormously under the yoke of austerity to make the meager progress that they have made. While it is clear that they have interrupted their respective inflation dynamics, we can't be sure what inflation would be across the eurozone if `things went back to normal.' What is the new normal for inflation in the eurozone? It's not with Germany as the high-inflation country! What sort of configuration of growth will emerge? What about the he local rates of unemployment? How soon will those be dissipated? How long can these extreme differences in unemployment rates endure? These are the unanswered questions. Progress has been achieved using austerity. But that progress has come at a terrible cost in some nations. The euro-banking system is still damaged. And there is no fiscal union or mechanism to deal with the mal-distribution of the costs on monetary unionization.

Although inflation difference in the eurozone have been significantly reduced- for now- there is still a question about how long that will remain and of what sort of growth can emerge from the ashes of austerity. These are the reasons to remain suspicious, guarded, and skeptical about where EMU is going.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief