Global| Mar 05 2020

Global| Mar 05 2020Euro Area Inflation Remains Controlled

Summary

In the euro area inflation remains well under the ECB’s just-less-than-2% objective. Globally inflation has been tame as the economic outlook has been pulled back. Oil prices have pulled back as well as the OPEC is resorting to some [...]

In the euro area inflation remains well under the ECB’s just-less-than-2% objective. Globally inflation has been tame as the economic outlook has been pulled back. Oil prices have pulled back as well as the OPEC is resorting to some draconian output cuts to try to hold the line on weak and weakening oil prices.

In the euro area inflation remains well under the ECB’s just-less-than-2% objective. Globally inflation has been tame as the economic outlook has been pulled back. Oil prices have pulled back as well as the OPEC is resorting to some draconian output cuts to try to hold the line on weak and weakening oil prices.

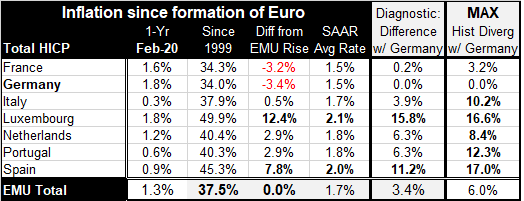

Among the early-reporting EMU nations, Germany has the highest inflation rate along with Luxembourg. Luxembourg’s inflation has long been excessive. For Germany, having an inflation rate near the top of the heap is a relatively new experience. Germany has the lowest unemployment rate in the EMU and that helps to stoke inflation pressures. Yet, Germany has been running fiscal surpluses and those surpluses should help to offset price pressures.

Germany has consistently been the low inflation EMU country as the second from-the-right column shows. France has stuck close to the German inflation result having had nearly the exact same rise in its price level as Germany. However, Italy, Portugal, and Spain that have been traditionally high inflation countries are now bringing inflation in on the low side.

The new inflation dynamics are the result of the last financial crisis and the austerity Germany helped to enforce as the EU Commission suddenly began to strictly monitor Maastricht rules and to force countries to toe the line or face consequences. That enforcement broke long-standing inflation habits in the Mediterranean European economies. However, Italy show signs of wanting to back track as it has wanted to reengage fiscal stimulus again for some time. Now, with the coronavirus greatly impacting the Italian economy, Italy again wants to unlock a fiscal solution.

In Germany, the Bundesbank already has suggested that Germany switch over to use fiscal stimulus. And apparently this is now being seriously albeit as a temporary program. Finance Minister Olaf Scholz told lawmakers on Wednesday that Germany would have “all the strength” needed to counter the impact of the coronavirus if the epidemic plunged the world economy into a crisis. He spoke of timely temporary and targeted stimulus. Crises of various sorts are an opportunity to change policies. For Germany, it’s a chance to get off the austerity kick it has been on. For Italy, there may be a brief opportunity to mobilize some fiscal spending, but not for the sort of ongoing program of spending that Italian politicians have been seeking under the Five Star Movement or the Northern League.

The facts on the ground now simply call for more fiscal stimulus because monetary policy is tapped out. Inflation is going to continue to skim under the ECB target as growth eases under the impact of bringing the coronavirus to heel. However, the long simmering disputed views over what monetary policy should be and how fiscal policy should be used will remain unaltered. The divisions on these issues among EMU members remain. Even as the U.K. leaves the EU over differences over the right role of the central authority in the EU remaining members continue to have very different approaches. Conflicts internal to the EMU are there even if voices of dissent are muffled. Leaving the EMU now seems impossible after what we have seen the U.K. go through to leave a far looser confederation, the EU that’s a much lower hurdle and still it was quite hard to arrange. It would seem that what the countries of the EU and EMU have yet to do is to settle on what their shared values and approaches to policymaking will be rather than to try to periodically use brute force to engage one sort of policy over another.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief