Global| Jan 20 2021

Global| Jan 20 2021Euro Area Inflation Persists in Negative Territory

Summary

Euro area inflation is negative on a year-over-year basis for five months in a row. On a monthly basis, EMU inflation has fallen in only five of the last 12 months, but the balance between the size of the gains vs. the size of the [...]

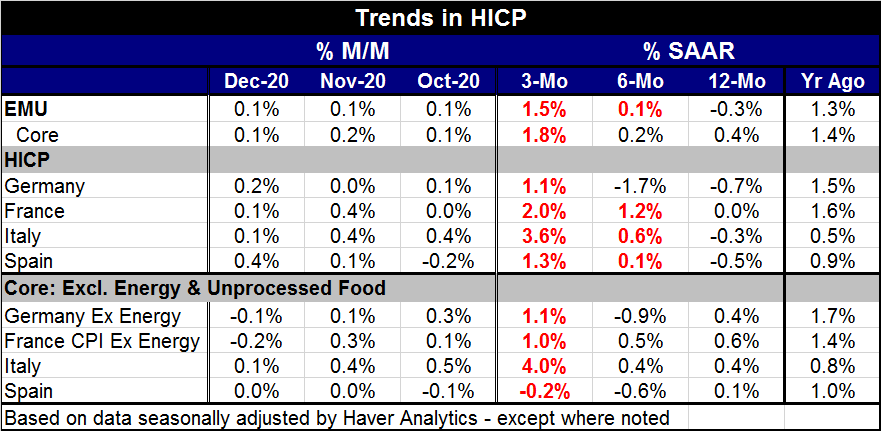

Euro area inflation is negative on a year-over-year basis for five months in a row. On a monthly basis, EMU inflation has fallen in only five of the last 12 months, but the balance between the size of the gains vs. the size of the drops has been skewed enough to keep the 12-month change negative. However, month-to-month headline HICP inflation has now been positive for three months in a row.

Euro area inflation is negative on a year-over-year basis for five months in a row. On a monthly basis, EMU inflation has fallen in only five of the last 12 months, but the balance between the size of the gains vs. the size of the drops has been skewed enough to keep the 12-month change negative. However, month-to-month headline HICP inflation has now been positive for three months in a row.

Sequential growth rates show that inflation is accelerating as six-month inflation is higher than 12-month inflation and three-month inflation is higher than six-month inflation. However, over three months, the annualized inflation gain is still only 1.5% annualized. And inflation still rides on the back of oil price cycles.

Core EMU-wide inflation shows a bit more of a pickup over three months to a pace of 1.8%, but it is not so clearly sequentially accelerating as core inflation weakens over six months compared to 12-months.

Large country trends

Country level data show inflation is accelerating from 12-months to six-months to three-months in France, Italy and Spain. Germany is an exception with prices falling at a 1.7% annual rate over six months, a faster drop that over 12 months. However, annualized three-month inflation in the four largest EMU economies shows inflation’s pace bounded by 1.1% and 3.6%. Still, three of these four countries show inflation is still negative over 12 months. France is the exception with inflation flat over 12 months. German inflation falls the fastest over 12 months among the four at -0.7%. Spain’s pace is -0.5% and Italy’s is -0.3%.

Core or ex-energy trends

The core or ex-energy measures by country show inflation’s uptick to be a recent phenomenon, a product of the last three months. Core inflation is positive year-over-year in each of the four largest economies at a pace ranging from 0.1% to 0.6%. But over six months, inflation weakens in each of these EMU members. It turns negative in Germany and in Spain over six months. Core or ex-energy inflation then accelerates in all four members over three months with Spain still seeing prices decline by 0.2%, but that is a decline smaller than what it posts over six months and it still counts as acceleration. In France, the core accelerates to a 1% pace. In Germany, it accelerates to a 1.1% pace. In Italy, it leaps to a 4% pace.

IMF outlook & the virus

Meanwhile, virus issues continue to dog Europe. Italy is even having governmental votes of confidence over the issue of who will decide how funds from the EU will be used to cushion the blow from the virus. Germany is still looking for a successor to Angela Merkel. In many places, the virus seems to have spawned or widened political divisions instead of being fought by a consolidation of national unity. In that sense, the virus has been even more destructive.

The IMF predicts stagnant growth for Germany in Q1 with growth picking up and reaching 3.5% for 2021 as a whole. That would follow a contraction in 2020 estimated at -5%. The IMF does not see GDP restored to its pre-covid-19 level until 2022. The IMF projects France to log growth of 5.5% in 2021. The IMF continues to see risks the forecast as large and, of course, dominated by the dynamics related to the virus. As rule the IMF generally is recommending more stimulus and not less (err on the side of doing too much, not too little). There is little concern about inflation. It projects French inflation below 1% in 2021. It also projects German inflation low at 1.2% in 2021. Clearly, the IMF is worried about growth and the impact of the virus ahead of everything else. It has been that way now for nearly a year. A lot depends on the effectiveness of the vaccines and the speed of their rollout.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief