Global| Dec 02 2015

Global| Dec 02 2015Euro Area Inflation Is Still Weakening

Summary

The preliminary HICP inflation rate for November was reported at a 0% rise month-to-month and as a skinny 0.1% gain over 12 months. The core rate fell by 0.1% month-to-month and is higher by 0.9% year-over-year. These trends are not [...]

The preliminary HICP inflation rate for November was reported at a 0% rise month-to-month and as a skinny 0.1% gain over 12 months. The core rate fell by 0.1% month-to-month and is higher by 0.9% year-over-year. These trends are not only weak but moving in the wrong direction. The ECB targets inflation just below 2%. The HICP report is preliminary and much of its detail is not yet released. But there is a supporting report on PPI inflation that has just finalized for October; it shows that at the producer level the downward pressure on inflation is still intense.

The preliminary HICP inflation rate for November was reported at a 0% rise month-to-month and as a skinny 0.1% gain over 12 months. The core rate fell by 0.1% month-to-month and is higher by 0.9% year-over-year. These trends are not only weak but moving in the wrong direction. The ECB targets inflation just below 2%. The HICP report is preliminary and much of its detail is not yet released. But there is a supporting report on PPI inflation that has just finalized for October; it shows that at the producer level the downward pressure on inflation is still intense.

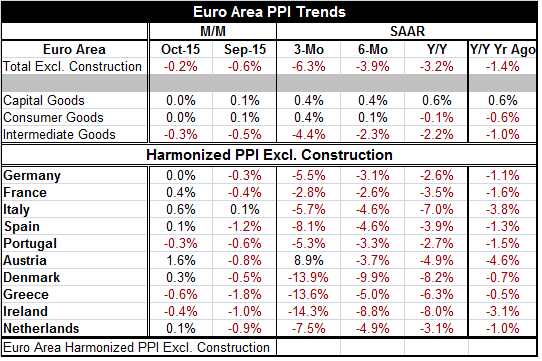

PPI price fell by 0.2% month-to-month in October after a 0.6% decline in September. Thus, producer prices excluding construction are lower by 0.8% in just the last two months. And the overall deceleration of headline producer prices is stepping up its pace of decline from 12 months to six months to three months. Downward price pressures at the PPI level have become more intense.

Disinflation is still lodged mostly in intermediate goods where the less processed goods reside. Intermediate goods prices fell by 0.3% month-to-month in October after dropping by 0.5% in September. Their pace of decline has stepped up from -2.2% over 12 months to -2.3% over six months to -4.4% over three months.

This deceleration is not a characteristic of either consumer goods or capital goods prices. Consumer goods prices actually show a very slight tendency to accelerate as their -0.1% drop over 12 months rises to a 0.1% gain over six months and a 0.4% rise over three months. But that trend is muted. Capital goods prices have a hint of deceleration in them but are best descried as hovering about a 0.5% pace over most horizons.

Producer prices show lots of weakness although the primary source of price weakness still appears to be in intermediate goods where commodity prices hit the index hardest. But ongoing price weakness is still reflected in capital goods and consumer goods prices apart from the weakness in intermediate goods.

Trends by country are still overwhelmingly weak. Prices are falling over 12 months and over six months as well as over three months for every country in the table with the lone exception of three-month prices in Austria. Of the 10 countries in the table, price declines accelerated for nine of them from six months to three months.

Clearly the ECB is facing stiff resistance in trying to get prices expanding again at a nearly 2% pace. However, in October, PPI prices did show some broad-based price pressure. Only three of the 10 countries in the table reported that PPI prices fell month-to-month. Germany saw flat prices and two counties, the Netherlands and Spain, saw increases of only 0.1% on the month. But four of 10 countries saw noticeable upward price pressure in October; they are: France, Italy, Austria and Denmark. Two of the four largest EMU members, France and Spain, are seeing some PPI price strength in October.

Still, the overall PPI numbers for the EMU in October remain weak. The monthly country-level reports suggest that there may be some upside to prices ahead. But don't count on that too much. What we see in the HICP, which already has a preliminary reading for November, is that price weakness has not suddenly gone away; in fact, prices got weaker in November.

On global markets, oil prices continue to bounce around in their $40/bl to $50/bl range like in some video game. But the oil surplus is still acute and global growth is not catching on. Commodity price weakness is going to be with us for some time to come. But commodity prices cannot continue to fall as they have been falling unless a global recession kicks in. The ECB, the Federal Reserve, the Bank of England and the Bank of Japan all are undershooting their respective inflation targets. And there is nothing afoot to suggest that these misses are only temporary.

All eyes are going to turn to the U.S. soon where one of the Fed's eight yearly meetings is scheduled. The Fed has pointed to the prospect of a rate hike by yearend and in mid-December the Fed will have its last meeting of 2015. U.S. growth continues at a moderate pace; yet it has been enough to drop the U.S unemployment rate. Below target inflation persists in the U.S. Its manufacturing sector is now in a state of decline according to the ISM diffusion index. The question is whether the Fed will press ahead amid a mixed domestic situation and conditions of weak global prices and weak growth to hike rates in the U.S. If it does that, what will be the impact on the rest of the world and on commodity prices that are traded worldwide in dollar terms? Will a Fed rate hike spur a stronger dollar and put more downward pressure on commodity prices and export disinflation to the rest of the world making the ECB's job even harder? Enquiring minds want to know.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief