Global| Jul 01 2016

Global| Jul 01 2016Euro Area Improvement Is Loud and Clear...But Will It Endure Brexit?

Summary

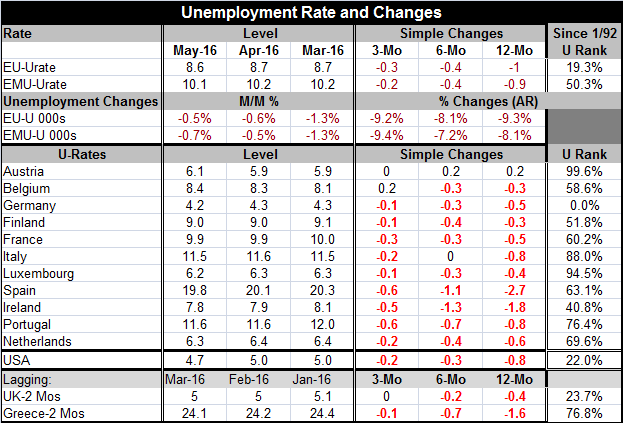

Phillips Curve Busters! Unemployment rates fell in six of 11 of these early-reporting EMU member states in May. Greece, where data lag by two months, shows a decline on that basis as well (making it seven of 12 drops in the `most [...]

Phillips Curve Busters!

Unemployment rates fell in six of 11 of these early-reporting EMU member states in May. Greece, where data lag by two months, shows a decline on that basis as well (making it seven of 12 drops in the `most recent month of data' among EMU members). The month of May saw the unemployment rate tick higher only in Austria and in Belgium.

Unemployment rates fell in six of 11 of these early-reporting EMU member states in May. Greece, where data lag by two months, shows a decline on that basis as well (making it seven of 12 drops in the `most recent month of data' among EMU members). The month of May saw the unemployment rate tick higher only in Austria and in Belgium.

More remarkably, unemployment rates are net lower over three-month, six-month and 12-month for most of the euro area. Nine of 11 countries show a drop over three-months and six-months with 10 of 11 net lower over 12-months. Austria is a persistent exception with a small backtracking in its rate.

The pace of the unemployment decline still appears to be pretty fast in Portugal and Ireland as well as France and possibly (surprisingly) Italy. The question now is what the Brexit process is going to do to all that.

On one hand, we expect `cooler heads to prevail' in actual UK-EU negotiations than what some of the early remarks suggest. However, there is still anger in Europe where the U.K. is viewed as having opened the air lock on a former air-tight ship. Europe has known for quite a long time that much of what it now professes to be surprised about is real: namely that there is a lot of grassroots dissatisfaction with the so-called euro project. Europeans have done all sorts of things to try to keep issues from ever being put to a public vote because what happened in the U.K. is really no surprise. But the U.K. vote has brought that difficult fact to the forefront and now European leaders have had to confront it and to confront the fact of it being not simply a problem in the U.K. Still, there is no sense that the U.K. has triggered the demise of the EMU. It is much a harder for an EMU member country to leave, but that does not mean that it could not be done. And as long and economic times are hard the process of Europeanization is relatively more painful and because of that more at risk.

This brings us to the final reason to worry about the impact of Brexit. It is that the EU leadership wants to send the message that leaving the EU is not painless. There has to be a cost to leaving since there is a cost to membership. That cost has to buy members something special. But what is that? The less good of a deal that Europe cuts for the U.K., the less good of a deal the U.K. will cut for Europe. Europe and Germany do trade a lot, but Germany trades the most with the U.K. among EMU members. And the U.K. is relatively more dependent on exports to the EU than vice versa. Still, there is enough mutuality to make any tie-severing painful and with economic impact.

The big unknown in this whole Brexit process is what will happen to financial services. No one yet has a hint, but Dublin, Paris and Frankfurt are three places hoping to make gains at the U.K.'s expense.

The good news is that the unemployment rates across the EMU are dropping suggests that the EMU is on solid footing as this process of dealing with Brexit unfolds. The release of the manufacturing PMI's from Markit underscores that point as the EMU readings for manufacturing are slightly firmer upon final revision. Italian unemployment surprisingly fell in May. Other Italian metrics have not been so robust recently.

Interestingly, the EMU shows no sign of Phillips curve behavior. As the unemployment rate has fallen so has the inflation rate. There is no sense of falling unemployment driving up prices or labor costs. In most cases we would applaud this result, but since the ECB is trying to get inflation back in the normal zone, this abnormality is still part of its policy conundrum.

In related reports released today, Asia for the most part is still very weak. It is Europe alone that is `outperforming.' China's manufacturing sector was either weak or weaker and shrinking depending on the PMI survey you favor. China's services sector did improve, but it's the manufacturing sector that most directly affects the rest of the world. And there is still not much certainty about the reports concerning China's foreign exchange plans in the wake of several conflicting news reports over the past several days.

On balance, we have a still weak Asia with its economic giant still struggling. U.S. gauges continue to show some weakness growth and we continue to wait on the performance of important new U.S. economic reports day by day. Today U.S. manufacturing sector is looking a bit firmer after the ISM release. Europe is showing some of the best momentum globally, but it will have to face the Brexit challenge. Today the IMF chief economist warned that it might have to reduce its forecasts yet again. BOE Governor Mark Carney asserts that the U.K. will need to cuts rates this summer in the wake of its own Brexit challenge. Despite some good economic news, all scenarios are still in play. To me the extension of weakens seems the most likely one. But there are grounds for greater optimisms if you're so inclined.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.