Global| Jun 16 2016

Global| Jun 16 2016Euro Area Growth and Inflation Send Mixed Signals

Summary

Mixed Grill... Today we pair a table on historic HICP EMU performance with monthly retail and auto sales in the EU. The consumer and the inflation are perhaps the two most critical variables watched by policy makers apart from job [...]

Mixed Grill...

Mixed Grill...

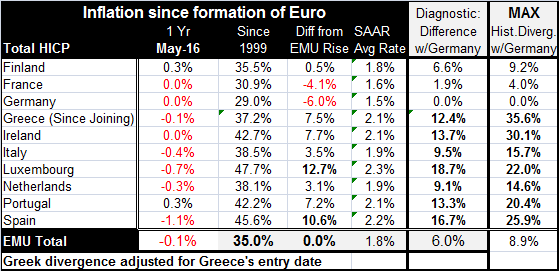

Today we pair a table on historic HICP EMU performance with monthly retail and auto sales in the EU. The consumer and the inflation are perhaps the two most critical variables watched by policy makers apart from job market metrics. The table shows that inflation continues to `way-undershoot' (pardon my use of technical language here) the ECB's inflation goal of a bit less than 2% (at -0.1%). Of course, to Germans, this number is right on target, but nearly everyone else in the EMU sees a considerable shortfall from goal.

Moreover, country by country we see for the earliest members of the EMU that inflation is really undershooting everywhere. It is weak across all of the earliest members of the EMU. The highest year-over-year inflation is 0.3% in Finland and in Portugal. Prices are flat or falling everywhere else.

Divergence in EMU and the flash-freeze process

The table focuses on the price level divergence that has developed in the EMU since its inception. At the formation of the EMU, currencies were carefully ushered into the fold. There was one last (for some investors a devastating) realignment, then rates were flash-frozen into a single block for `all-of-eternity.' This was not an optimum currency area, but it was formed with the benefits of such an area in mind. The euro stitched together countries with very different ideas about fiscal policy and public spending and historic inflation rates. Inflation rates were not fully harmonized ahead of the euro-currency flash-freeze process and many members did not grasp the importance of that omission. While historically high-inflation members did do better, `better' was not good enough.

Price level divergence in EMU

One column of the table shows the compounded inflation rate run by each member since it has been in the EMU. Note that now, after the financial crisis and after some countries have gone through the crucible of austerity, the highest annual inflation rate run is 2.2% in Spain (I omit Luxembourg since as a financial center it is a special case). With the ECB tied to a pace of a little less than 2%, this seems to be good performance. But during this period Germany chose to keep its inflation at 1.5% so that Spain's 2.2% lost 0.7 percentage points of competiveness to Germany each year the EMU was in existence. Spain's pre-austerity divergence culminated in a maximum divergence of Spain's and Germany's price levels of nearly 26 percentage points a mark since reduced to under 17 percentage points courtesy of austerity.

The position of power in a currency union

Germany has always understood how the single currency would work and moved quickly to grab the low ground in order to be the most competitive EMU member. Other countries had different goals. Greece wanted lower borrowing costs and it got those for a time. But that part of the euro was an illusion. All government bonds were not created equal and investors had yet to find that out for themselves. As a result, some countries overspent over inflated and have been pulled back. Price level divergences remain and some are still quite significant, but for the most part the worst of the divergences has been reduced. Germany's price level is nearly 19% lower than Luxembourg's compared to the start of the EMU while Germany's is only 1.9 percentage points lower than France's on that same timeline. The French have understood the game and have kept inflation close to Germany throughout despite having other problems to deal with. French labor laws are in the process of being aligned and the French worker is vociferously resisting. But no Frenchman is an island especially when he is marooned in a currency block with a bunch of Germans and others.

Consumer `recovery'

The consumer side of the EMU showing the performance of auto sales and retail sales volume is also revealed in a chart above. Both series are plotted in their native `level' format instead of the more familiar' percentage change format. What we can see from this treatment is that retail sales are back to 2007-2008 pre-crisis levels of sales. While that is good news, it means that during that 8-9 year period the sales level has not grown. Of course, it had fallen. Sales had contracted and now the old level for sales is restored, but there should be much less of sense of being back to normal since over this period population has grown and all sorts of other things have changed.

Vehicle sales make progress

Vehicle sales are back around their 2011 level. If we rank the level or pace (millions of units at an annual rate) of auto sales since 2007, we find sales are at their 74th queue percentile. Sales since 2007 have been better than this pace only about 25% of the time. If we compare sales back to 1995, we find sales have been stronger than this nearly 60% of the time. While auto sales have made a steady recovery in the EMU, they have not come all the way back either. The progress is impressive but incomplete.

What EMU members face

In trying to understand what central banks face, we need to understand these metrics. While the sales of autos and of goods at other retail establishments are doing better, Europe is still struggling. There is more price level divergence than when the EMU was formed despite the progress made under austerity. And that process of force-feeding austerity has cost the euro area a lot of `good will.' Germany is still by far the most competitive EMU member. Countries that have suffered under austerity and do not see a clear bright light at the end of the tunnel are only experiencing the new reality. It is the new way of the world, a world they signed onto when the EMU was formed whether they knew it or not. Now they know. As much austerity as they have suffered, they need more to realign relative to Germany in the EMU. In a better-growing global economy, this might not matter. But in a world where everyone is fighting over table scraps of domestic demand, competitiveness is critical.

The challenge ahead: understanding

Substantial challenges lie ahead. Just yesterday we witnessed a watershed policy change by the Federal Reserve that finally has admitted to a new reality - one different from what it had previously been assuming. We face the risk of Brexit with new polls showing the `leave' faction gaining momentum - if we can believe it. We face central banks increasingly be criticized by even high profile investors as losing control, something that can't be good for central bank credibility. And we have bond yields the likes of which no one ever expected to see on a global basis. There is no agreement on what has gone wrong or how to fix it. And that should be the most disturbing part of where we are (which is lost!). Only the Germans think they know what to do and I don't think following their advice is a good idea. The Fed has jumped off of its multiple rate hike bandwagon. But it has not reported a new paradigm for policy. It has just slowed the anticipated pace of rate hikes without much change in the underlying outlook. In the end we do not get much clarity out of the Fed's policy switch. Meanwhile other central banks are staying their respective courses running their own experimental policies. Everyone is holding on, waiting for the Brexit vote and hoping that even though they continue doing the same thing someday there will be a different result. Does that seem likely?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief