Global| Aug 14 2015

Global| Aug 14 2015Euro Area GDP Simmers As Do Troubles

Summary

In the European Monetary Union, growth continues to be sluggish. Overall EMU-18 growth slipped to 1.3% (annualized) in Q2 from 1.5% in Q1. The year-over-year growth rates, however, have progressed, rising to 1.2% in Q2 from 1% in Q1, [...]

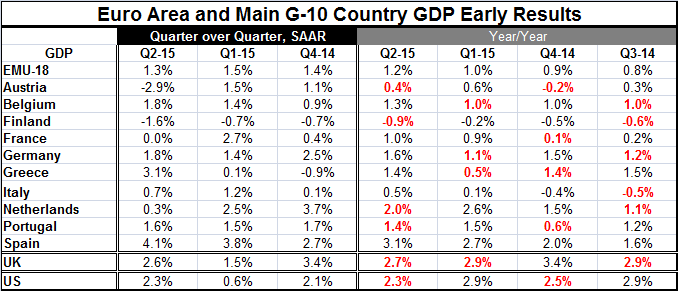

In the European Monetary Union, growth continues to be sluggish. Overall EMU-18 growth slipped to 1.3% (annualized) in Q2 from 1.5% in Q1. The year-over-year growth rates, however, have progressed, rising to 1.2% in Q2 from 1% in Q1, and have steadily- if slowly- been improving.

In the European Monetary Union, growth continues to be sluggish. Overall EMU-18 growth slipped to 1.3% (annualized) in Q2 from 1.5% in Q1. The year-over-year growth rates, however, have progressed, rising to 1.2% in Q2 from 1% in Q1, and have steadily- if slowly- been improving.

In the quarter, five of the 10 EMU nations listed in the table had slower rates of growth quarter-to-quarter. The EMU itself slowed as relatively more of the weakness was in large countries. France, Germany and Italy slowed.

Italy has the weakest year-over-year growth among the four largest countries at 0.5%. But France is only up by 1%, Germany by 1.6% and Spain by 3.1%. Growth in these big-four economics is steadily accelerating except for Germany.

Finland is doing particularly poorly as it is the only country in the table with year-over-year GDP lower, falling by 0.9%.

Among the Mediterranean countries whose growth is captured in the chart, only Spain has consistently strong acceleration in gear. However, all are posting positive rates of growth and that represents some improvement.

With China's yuan sharply depreciating and thereby signaling that its leaders have lost faith in their ability to initiate reforms fast enough to hit their growth targets, the world economy has become a weaker place and an area with stiffer competition. Oil prices are sliding; an Iran nuclear deal could accelerate that. Japan could add to oil surplus pressures as it has started to reopen its mothballed nuclear plants. While everyone has been waiting for more growth to emerge and for prices to firm, instead there are still more forces of weakness and of deflation in train.

All countries will find this a more hostile environment although net oil importers will get some budgetary relief. Oddly the WSJ reports that economists expect the Fed to hike rates in September. Surely growth is solid enough, but the price environment leaves the Fed wanting for its price goals and the price weakness is so pervasive the Fed could hardly say it sees itself hitting its target in the intermediate term. Being sure of hitting its price target is a pre-condition for a Fed rate hike. And one simply wonders how the global economy would react to even a small rate hike. After all, markets extrapolate and form expectation. The Fed's own forward guidance expressed in terms of Fed funds rate `projections' offered by FOMC members seems to point to a period of relatively fast rising rates regardless of what Janet Yellen says.

While we hoped to be embarking on a period of more solid growth by this time, it is unclear the extent to which the global economy has made the right turn or the wrong one to go deeper into the trouble zone. For now, growth prevails and there are signs of progress in Europe, albeit slow progress. Yet, there are still plenty of problems areas some of which have gotten worse, China being an example. Risks remain in force and I have not even discussed the geopolitical tensions that simmer.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief