Global| Nov 15 2016

Global| Nov 15 2016Euro Area GDP Plods Ahead

Summary

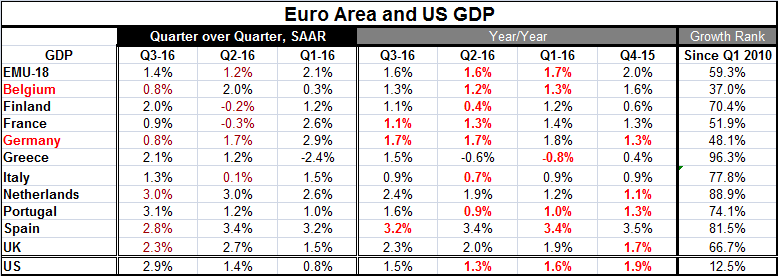

GDP growth plods ahead in the EMU in Q3 2016. Its 1.4% annualized quarterly pace beats the Q2 pace of 1.2%, but year-on-year the growth rate stays at 1.6%. Mixed results Quarter-to-quarter, there are slowdowns logged in Germany, [...]

GDP growth plods ahead in the EMU in Q3 2016. Its 1.4% annualized quarterly pace beats the Q2 pace of 1.2%, but year-on-year the growth rate stays at 1.6%.

GDP growth plods ahead in the EMU in Q3 2016. Its 1.4% annualized quarterly pace beats the Q2 pace of 1.2%, but year-on-year the growth rate stays at 1.6%.

Mixed results

Quarter-to-quarter, there are slowdowns logged in Germany, Belgium, the Netherlands, Spain, and the United Kingdom. Finland, France, Greece, Italy and Portugal show quarterly speed ups. There is a pretty mixed picture. Year-on-year, the metrics favor acceleration more as only France, Germany and Spain show growth at an unchanged pace or slower. Still, those countries are three of the four largest economies in the EMU. That result follows Q2 when eight of 11 of these reporters posted growth rates that that either were weaker year-on-year or dropping. So the comparisons with Q2 is essentially an easy comparison and therefore not as meaningful.

The GDP sideways shuffle

The chart shows that GDP growth rates are basically moving sideways at a moderate pace: the EMU, France and Germany. The far right hand column of the table ranks each country's year-on-year growth rate since 2010, expressing the result as a percentile standing in that queue of data. Only two countries, Germany and Belgium, have growth rates below their medians (50%) on this timeline. But only Greece, the Netherlands and Spain have growth rates in the top 20% of their rankings on this timeline. However, on this timeline the average for growth in EMU has only been 1% so this too is a low hurdle for comparison.

Context: Other reports...

In other reports on the day, the EMU trade surplus widened despite exports falling. That is not a good sign. Expanding the surplus through imports, contracting them faster than exports are falling, is a bad way to make trade progress. In Germany, the ZEW investor confidence index saw its fifth straight rise and despite the weakening German GDP the ZEW financial experts remain upbeat, although ZEW notes that some optimism was trimmed because of the election of Donald Trump in the U.S.

OPEC and oil

Also interesting is the strength in oil prices. Oil has been weak again as the plan to cut oil output by 'OPEC and Friends' has fallen so flat and has been such clear failure. However, another OPEC meeting is planned and OPEC like Lucy and Charlie Brown is going to try and kick that football again. The prospect for a real connection seems about same as for Charlie Brown ever to kick that football in that famous 'peanuts' cartoon strip (Hint: he never does). What is more interesting is that globally bonds have been selling off and yields have risen to within a few ticks of leaving the U.S. 10-year Treasury-note yield unchanged on the year. The Trump political pessimism seems to be an equal match for Trump economic optimism. But today bonds have turned to rally as foreign money is reported to be coming into the now 'high yielding' U.S. bond market. And while there are all sorts of commentary on how U.S. growth will be greater and U.S. inflation higher unlit today there has been no knock on impact on oil. The jolt that oil is getting today is reported to be linked to potential supply reduction. Meanwhile, in the U.S. drilling continues to step up on the back of these already firmer oil prices.

The outlook

It should be clear that nothing is clear. There is a lot of speculation about what the Trump election will means on many fronts. And for now bets are for more (U.S.) growth and inflation and that bias does seem to be about right to me. But it is not clear that markets have not gone way overboard with it all. At the end of the day, the U.S. still has severe competiveness problems and weak productivity trends that are not going to vanish. If the new president were to use tariffs or other trade restrictions to protect U.S. industry (as he has threatened), that would be debilitating to the U.S. economy. The question is whether President-elect Trump can find a way to economic stimulus that avoids that road to perdition. Tax cuts will bring stimulus by themselves but also other problems. The big question to me is whether tax cuts alone will bring investment to the U.S. in the face of still very stiff competition from overseas. Do tax cuts trump competitiveness issues? It is far from clear that Trump has a plan that navigates all these minefields. The Chinese have been cooperative with no one: why will they start with Trump? They have an expansionist plan that will make it hard for them to acquiesce to compromise. As far as the view for more inflation goes, the run up in the dollar militates against that. The global environment is still one with plenty of slack although 'protectionism' would raise a wall of anti-competitiveness behind which inflation pressure could build. That may be the one wall that Trump could build. In short, there are a lot of moving interrelated pieces here that are being assembled into a collage of market outlook way too quickly. Republicans are a triple threat of legislative and presidential power but that party is hardly monolithic. As Trump himself has said, he has a lot of first priorities. What he will do and how soon his policies will have impact and the strength of that impact seems to have been overly discounted and too substantially extrapolated. The world simply has not and will not change all that much at least not so quickly.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief