Global| May 13 2016

Global| May 13 2016Euro Area GDP Growth Takes Slight Downward Revision

Summary

Euro area GDP was revised down from a quarterly gain of 0.6% to a gain of 0.5%. The annualized rise is presented in the table at 2.1%. We also show year-over-year results for the last four quarters. The final column ranks each unit's [...]

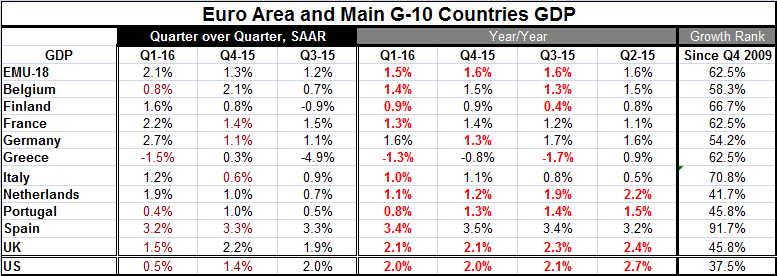

Euro area GDP was revised down from a quarterly gain of 0.6% to a gain of 0.5%. The annualized rise is presented in the table at 2.1%. We also show year-over-year results for the last four quarters. The final column ranks each unit's year-on-year growth on its performance back to Q4 2009.

Euro area GDP was revised down from a quarterly gain of 0.6% to a gain of 0.5%. The annualized rise is presented in the table at 2.1%. We also show year-over-year results for the last four quarters. The final column ranks each unit's year-on-year growth on its performance back to Q4 2009.

Growth rates are still moderate

The perspective of the table's final column shows that EMU growth is now only in the 62nd percentile of all growth rates since end-2009. This has not been a very impressive period for growth and this ranking is not a very impressive ranking in this unimpressive period.

Spain's growth for this period ranks quite high in its 90th percentile. Italy's growth (at 1%) is in its top 70the percentile for the recovery period. Finland, France and Greece (Greece at -1.3%!) post growth rates that lie some in the 60th percentile of their historic queue of data.

Belgium and Germany lie above their median on their 50th percentile scale. The Netherlands, Portugal and the U.K. lie below their median growth rates for this period. For comparison, we present U.S. GDP which has largely outperformed this group in recovery but now has slowed with the U.S. results lying in the lower 37% of its queue of growth rates since 2009 as the Fed ponders a rate hike.

Slowing is widespread

The bold red figures represent period-to-period slowing. We see that slowing is widespread. Quarter-to-quarter GDP trends are mixed as to speed-up or slow-down, but the year-on-year trends show slowing as the predominate trend. Of the 11 countries plus the EMU area in the table, all show year-over-year slowing in Q1 except Germany. Half of the table showed slowing in Q4 2015 and three quarters showed slowing in Q3 2015. The slowing has been in train for a while although it is not a very robust slowing. In some of the cases, the growth rate slowdown does not even register when we print growth rates at the one-digit level of precision (for them there is a technical slowdown).

However, the trends do tell a story of steady to weaker growth. Fiscal policies remain sidelined while monetary stimulus is still being actively fiddled with in Europe with little in the way of demonstrable results.

New reports and trends

There was a breadth of economic data on offer today beyond GDP. Among today's report, we found that European vehicle registrations were strong. In Japan, the services sector index has slowed and dropped in March. In China, bank lending has slowed abruptly. Fortunately there was some good news in the U.S. where vehicle sales also helped to push retail sales up sharply and with some support outside autos for a change. But there is a pall of weakness cast over the day's reports with GDP largely slowing down across Europe and with a sharp lending pullback in China.

The global economy remains importantly linked and we see the synchronous slowing across all economies. Today IMF managing director Christine Lagarde made a more pointed statement about the danger to the U.K. economy were there to be a Brexit. The policy makers seem to be upping their warnings as the date for the U.K. vote draws near. There is an air of economic slowing, stock market prevarication and economic risk about. Globally the auto sector has been a mainstay for growth, but it has been supported in some places by subprime lending, making me wonder if the sector gets more vulnerable later in the business cycle (where we are now). So far, growth remains intact. Economies may cough and sputter and slow, but then they pick back up. Is that why U.S. retail sales are back up and consumer sentiment has revived? Is there economic revival just around the bend?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief