Global| Nov 23 2009

Global| Nov 23 2009Euro Area Flash PMIs

Summary

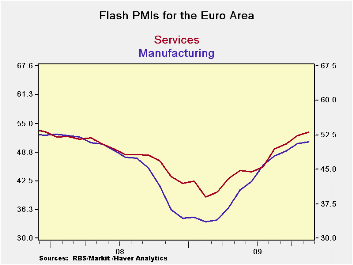

The Euro Area FLASH PMIs are on the rise in November. The flash Services reading is at its highest reading since November 2007. The MFG index is at its highest since March 2008. It is the second consecutive MFG reading above 50 and [...]

The Euro Area FLASH PMIs are on the rise in November. The

flash Services reading is at its highest reading since November 2007.

The MFG index is at its highest since March 2008. It is the second

consecutive MFG reading above 50 and the third consecutive reading

above 50 for services. Readings above 50 indicate expansion.

However, the percentage increase in the Yr/Yr readings for MFG and for

services each have receded for two months running as the pace of the

recovery’s improvement is slowing.

Since March of 2009 the MFG index has improved by 2.4 points per month

on average. Each monthly increase has been a gain of one point or

better until this month, November 2009, when the improvement was just

0.32 points.

Over this same span the services index averaged a monthly increase of

1.66 per month. However, in June of 2009 the e-Zone Services measure

did decline by 0.17 points interrupting a string of increases. Except

for that drop this month’s rise of 0.82 is the weakest since March of

2009.

Both services and MFG sectors continue to increase but are doing so at

increasing slower rates. This is despite the fact that they reside only

in the mid to low 60th percentile of their respective ranges, ranges

that extend back to July of 1998 for both of them (the MFG range does

have a bit longer history, however0.

Manufacturing stands at a flash reading of 50.98 compared to an average

reading of 51.09 since July of 1998. For services the current 53.17

reading compares to an average reading of 53.69. Both readings are

slowing their pace of increase while still below their respective cycle

averages. This is not good news if there is any expectation of strong

recovery in Europe. Germany may be contributing to the slow down since

its own program to stimulate car purchases has wound down. Other

nations also had a car sales promotion programs that have wound down.

So maybe some of the slowing can be explained away. But that still

leaves a question about what will speed the pace of recovery back up.

If the answer is ‘nothing,’ then the caveat does not amount to much.

For now recovery remain is gear but it is slowing.

| FLASH Readings | ||

|---|---|---|

| Markit PMIs for the Euro Area | ||

| MFG | Services | |

| Nov-09 | 50.98 | 53.17 |

| Oct-09 | 50.73 | 52.58 |

| Sep-09 | 49.29 | 50.86 |

| Aug-09 | 48.24 | 49.92 |

| Segment averages | ||

| 3-Mo | 49.42 | 52.04 |

| 6-Mo | 46.30 | 49.29 |

| 12-Mo | 40.50 | 45.59 |

| 136-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| % Range | 64.7% | 60.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief