Global| Jun 23 2016

Global| Jun 23 2016Euro Area Flash PMI Steps Back on Weak Services

Summary

The chart is clear. The manufacturing sector stepped up in June while services stepped back. The two sectors now have nearly the same raw PMI score, but their queue standings are wide apart. The services sector usually is expanding [...]

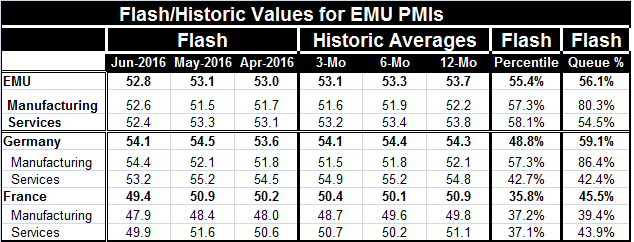

The chart is clear. The manufacturing sector stepped up in June while services stepped back. The two sectors now have nearly the same raw PMI score, but their queue standings are wide apart. The services sector usually is expanding and its PMI values tend to be higher than in manufacturing. As a result, at the same raw score, the service sector PMI will be weaker. And that is the case this month. The EMU manufacturing gauge is in its 80th queue percentile standing (higher only 20% of the time) while the services index stands in its 54th queue percentile (higher about 46% of the time). These are very different relative standings. The overall EMU result is dominated by the services sector as the lower EMU standing in its 56th percentile shows us.

The chart is clear. The manufacturing sector stepped up in June while services stepped back. The two sectors now have nearly the same raw PMI score, but their queue standings are wide apart. The services sector usually is expanding and its PMI values tend to be higher than in manufacturing. As a result, at the same raw score, the service sector PMI will be weaker. And that is the case this month. The EMU manufacturing gauge is in its 80th queue percentile standing (higher only 20% of the time) while the services index stands in its 54th queue percentile (higher about 46% of the time). These are very different relative standings. The overall EMU result is dominated by the services sector as the lower EMU standing in its 56th percentile shows us.

Germany is mixed

Germany has sector relationships much like the EMU. The two sector standings are similar with manufacturing stronger and with their relative queue standings quite different and even more skewed than for the EMU as a whole. The German manufacturing sector has an 86th percentile standing (higher only 14% of the time) while its services sector standing is at its 42nd percentile, below its median and higher about 58% of the time.

France is weak

France is once again off on its own with weakness all around. The French overall PMI standing is in its 45th percentile, below its median since 2011. France's service sector raw score is higher than its manufacturing sector raw score, but its percentile standings for services and manufacturing each are below their respective medians with manufacturing in its 39th percentile and services in their 43rd percentile.

Momentum is sideways

The moving averages of PMI values shows the EMU, German and French private sectors are moving mostly sideways over the last 12 months at relatively weak readings. In France, services have skated just above the 50% breakeven line with manufacturing usually just below it. In Germany, services have been relatively firmer with manufacturing weak until this June report. June gives the strongest German manufacturing reading since February 2014. Similarly in the EMU, the last two higher manufacturing readings were in December and November 2015, but then one must go back to April 2014 to find a higher one. Germany must not be alone in showing a better manufacturing performance in June. However, EMU services are weak already and last weaker in January 2015. French services were last weaker as recently as February 2016, but then one has to go back to January 2015 to find a weaker reading than June.

Once again the chart tells a pretty good story of the trends. Manufacturing is gaining some purchase, but services are weakening and losing momentum in the EMU.

Brexit EU and EMU

Against this background, of course, we have the `news of the day' playing out which is the U.K. vote on Brexit. No matter which way the vote goes, Europe will be forever be changed. Europe's leaders now recognize that their zeal for further integration is not shared by their local citizenry in many places, not just in the U.K. The U.K. may still vote to stay, but the vote appears as though it will be close - hardly a ringing endorsement in either direction for a course that will be set for some time to come. Politicians will be on tenterhooks. It could embolden others to test the stay-or-go waters, too.

The U.K. is a special case as it's the third largest European Economy and the largest EU non-EMU member. For the non-EMU EU members to lose the U.K. as a fellow member, it would mean that their influence would shrink markedly forever. It could push some of these nations to rethink their attachment to either swing to full EMU membership or to themselves consider an independent stature. Whichever way the U.K. vote plays out, it would seem that the representatives in Brussels are getting a wake-up call on displeasure with bureaucracy and a call to pay attention to how they harmonize rules.

At the end of the day, the Europeans seem to have an affinity for being `European' and love some of the special features of EU membership (like Schengen) but remain much more fully identified with their nation of birth and the one where people speak their national language. No surprise there?

It is also clear that to see some euro-members using EMU and EU rules force polices on other countries and to impose their values on them based on the unique circumstances of poor economic times globally may have made EU/EMU membership more distasteful. For the first time since the EMU was formed, countries are seeing the real downside to membership. And this is not just Greece. There are austerity programs in play and outright fighting over how the ECB will be run. The Germans are sticklers over operating policies even though the ECB is nowhere close to hitting its single policy-mandated target. And there is no release valve for such a situation, so very move is a fight and that delays action making it less effective. It would not be surprising if that led to second thoughts about membership. In the EU there are concerns too, about the common migrant policy- some have simply unilaterally opted out of that.

Pandora's box...

It should now be clear to all members in the EMU that being in the single currency area will have at least as many responsibilities as benefits. Indeed, the responsibilities may outnumber the benefits. As an independent country, a nation might choose to thumb its nose at German rules and to a run a higher inflation rate, let their currency depreciate and to have a different set of social welfare preferences. But as an EMU member, such behavior is nearly impossible and will lead to consequences and very unpleasant ones. It would not be surprising to find that revelation also has consequences. The U.K. is only considering an opt-out of the EU, but its rethink could have much broader repercussions whatever the outcome of its vote. Pandora's box is officially open.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief