Global| Sep 23 2016

Global| Sep 23 2016Euro Area Composite PMI Weakens; Trends Diverge

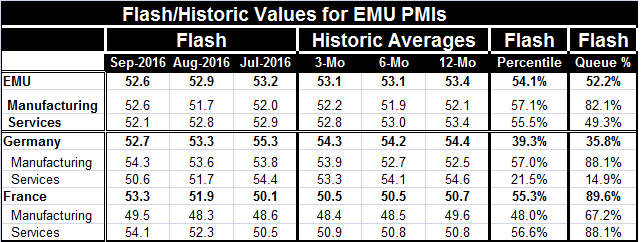

Summary

The EMU composite (private sector) index has fallen in September to a diffusion reading of 52.6 from 52.9 in August. It is the weakest reading since January 2015. This overall PMI gauge is now in the 52nd percentile of its queue of [...]

The EMU composite (private sector) index has fallen in September to a diffusion reading of 52.6 from 52.9 in August. It is the weakest reading since January 2015. This overall PMI gauge is now in the 52nd percentile of its queue of data back to January 2011. The month's drop in the composite index is driven by weakness in services which fell to a diffusion reading of 52.1 in September from 52.8 in August.

EMU services

The monthly service sector index has dropped more sharply month-to-month since January 2011 only 14% of the time. The level of the service sector index stands in the 49th percentile of its historic queue of data, below its midpoint since January 2011. At a level of 52.1 in September, the service sector index is below its 12-month average of 53.4.

EMU manufacturing

In contrast, manufacturing improved in the EMU this month. The manufacturing gauge rose to 52.6 in September from 51.7 in August. Manufacturing was last stronger in June 2016 and in December 2015 before that. The manufacturing index stands in the 82nd percentile of its queue of readings since January 2011. At 52.6, it is slightly above its 12-month average of 52.1.

Manufacturing compared

There is some degree of pick-up in French manufacturing. For France a series of seven consecutive manufacturing readings below 50 is now being `challenged' by the bump-up this month to 49.5. France is a curious case; its manufacturing sector has been moribund and mildly shrinking for the last one-half year. And while there is some bounce in September, the sector is still on balance shrinking. Against the background, the sudden pick-up in service sector activity is hard to explain. Germany is advancing toward its peak manufacturing reading in this recent mini cycle. For Germany, manufacturing is sort of back in gear but these are still historically weak readings for Germany despite the fact that they rank relatively high among the group of readings since January 2011. German export orders perked up in the September PMI survey. The EMU manufacturing reading is rising on the month but may still be locked in an eroding trend.

France goes its own way in services

The charts and table tell a story of a services sector that is withering -except in France. The French pick-up is strong and surprising. Services are improving sharply in France which reports a solid increase in new business. Staffing was increased in the French services sector, the opposite from manufacturing where levels of employment were cut. The pick-up comes out of the blue.

Das services

The German services situation is somewhat disturbing. To this point, the German retailing sector had been one of the very strongest aspects of the German economy, according to the EU Commission indices. While there are no data to confirm or even commentary from Markit on this month's service sector sudden deflation, I have to speculate. I wonder if the migrant issues in Germany are weighing on German consumers. Is there a safety and soundness issue that has held back service sector activity because of concerns for personal safety? Again this is pure speculation on my part. But the service sector weakness is going begging for some answers. The services sector should not be so volatile. The German services sector had some `similar' stand-alone weakness from 2014 to 2015, but that time the manufacturing sector also weakened slightly and it had been weaker than services to begin with; thus, making the services drop look like it was just catch-up. In this episode, German services are unraveling with manufacturing gaining momentum. It's a disconnect.

One of the daily themes today is cross-currents

We see Germany and France with different trends and we see manufacturing and services moving in different directions. France also has cut its Q2 GDP estimate today to show a small decline instead of flatness. In Japan, there are cross-current as its Markit manufacturing gauge switched to expansion crossing over the 50 line but Japan's own all-industries index deteriorated.

Gear shifting?

When the data emit inconsistent signals, it is hard to make sense of them. But it is also true that we get this sort of thing most frequently when the economy is changing gears. Is Europe changing gears? And if it is, is it upshifting or downshifting?

Different strokes for different folks...yes but...

The ECB has just issued a statement reminding us that it is wary of continued downside risks and is vigilant with policy. In the U.S., the Fed Chair has just said that the U.S. economy is closer to conditions that justify a hike in rates. This is with the two longest-standing purchasing manager surveys from the ISM weak. The ISM manufacturing gauge for the U.S. is below 50 and the services gauge is on a 79 month low (six and one half year low!). Certainly, the U.S, and Europe are experiencing different business cycle effects and positions, but the Fed's insistence that it is close to conditions that call for a hike in rates does not seem well-supported by the facts. The just-released Markit flash manufacturing index for the U.S. in September just notched lower, falling to 51.9 from 52.1 in August; that index is signaling continued if unremarkable expansion (a lower 10th percentile standing in its historic queue of data).

Who's in first?

Data like this will make for sleepless nights and policy disagreements. But the arguing is about the future and where things are going since the present clearly is still weak. If one of these monthly bounces in the data is going to grow into something much stronger and sustainable, we have yet to see any reliable evidence that it is so. For now all the concern about the future stems from the minds and the economic beliefs of the policy-making forecasters themselves- and they have been so consistently and so thoroughly wrong. Nevertheless, as we know, at some point they won't be. Economics is one of the few places where you can be wrong 95% of the time but then smugly assert `I told you so' by being right 5% of the time. Still, there is no telling that we are anywhere close to that being true either in Europe, the U.S., Japan or China. All are still stuck in first-gear mode with fears of downshifting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief