Global| Oct 05 2016

Global| Oct 05 2016Euro Area Composite PMI Dragged Down by Services

Summary

German service sector weakness clobbers the EMU readings The long slow erosion, depicted in the chart of the EMU region's services PMI, stepped up in September as the EMU service sector index slipped by 0.6 points on the month, its [...]

German service sector weakness clobbers the EMU readings

German service sector weakness clobbers the EMU readings

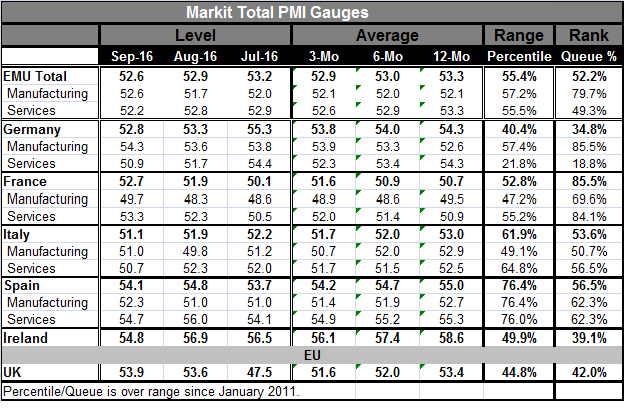

The long slow erosion, depicted in the chart of the EMU region's services PMI, stepped up in September as the EMU service sector index slipped by 0.6 points on the month, its largest month-to-month drop since January. Germany's service sector contributes importantly to the demise of the EMU services and overall reading. The German service sector which saw its index drop by 2.7 points in August fell by another 0.8 points in September. This two-month drop is the largest since May 2015 and its two-month performance ranks in the bottom 12% in its historic queue of data. The sector is still expanding, but at a reading of 50.9, it is the weakest German service sector performance since June 2013. The German service sector has a queue percentile standing since January 2011 that has been weaker only about 19% of the time- and this is for what has been the strong economy in Europe. That's not good news.

EMU Details

On this German weakness, the EMU composite index is lower to 52.6 in September from 52.9 in August. EMU manufacturing is stronger with a diffusion reading at 52.6 up from 51.7, a nice bump up. Service slips to 52.2 from 52.8. The EMU composite index stands in the 52nd percentile of its historic queue of data (back to January 2011) with a queue standing in the 79th percentile for manufacturing and in the 49th percentile for services...below its historic median. Here we see the knock-on effects from the Germans service sector whose metrics are chilling.

Changes in Manufacturing

Manufacturing improved in each of the four largest EMU economies. France, however, still has a contracting manufacturing sector; Italy swung from contraction to expansion on a month-to-month gain of better than one point. However, only Italy has a manufacturing reading for September that is weaker than its level in July.

Changes in Services

As for services among the Big-Four EMU economies, only France has a service sector improvement in September. No other Big-Four economy has two consecutive slowdowns in their respective service sectors. However, both Germany and Italy are on balance showing weaker service sectors in September than they showed in July.

Manufacturing Levels

Looking at the standing of the manufacturing sectors' levels, manufacturing stands at its 79th percentile for all of the EMU. Of the Big-Four economics, only Germany and France have higher manufacturing percentile standings than the EMU with both France and Germany at their respective 85th percentiles. Italy has a much weaker diffusion percentile standing for manufacturing. France gets a strong reading on its relative position because it has been so weak not because it is strong in September. Spain logs a steady, but not impressive, 62nd percentile standing.

Services Levels

The services percentile standing for the EMU is below its median at its 49th percentile. This is mostly the result of Germany's drop to its 18th percentile, dragging down the EMU aggregate. France's service sector is up again in September and stands at its 84th percentile. Spain stands at its 62nd percentile and Italy stands at its 56th percentile.

Composite Indices

Italy has consistent near median readings for its composite manufacturing and services with low-to-medium 50th percentile standings. Germany has the weakest composite despite a strong manufacturing reading because of the super-weak service sector. France shows some variation among its sectors as well with services strong and manufacturing more on the firm side, but that's enough to boost its composite to a high 85th percentile standing, the best of the lot despite having the third weakest raw diffusion score among the Big-Four economies. So France, an economy that has been struggling, is now beginning to show some life and in relative terms that shows up as strength. Spain's composite is in the mid-50th percentile despite having two components that each rank in their respective 62nd percentiles.

Not Just Euro-Confusion

Europe is confusing in September with the extreme German slowdown and surprising ongoing service sector weakness. But on the new data in the U.S. from the ISM (not so much from the Markit data, however) the U.S. services sector also is acting very flaky as it was very weak in August and shot back up to a strong reading in September. It's hard to know what that means.

Summing Up

On balance, we see the U.S. is off on its own again. EMU shows a weakening service sector and while Germany is a big part of it, it is not the whole of it. Globally service sector reports are generally weaker in September as well. That sector tends to be the backbone of growth since it is less volatile. It can act as a shock absorber. Like any shock absorber, if you stress it too hard or too often, it may not hold up. This encroaching weakness in the service sector (less strength and diminishing momentum) will leave the global economy more vulnerable especially if there are any shocks that could impact manufacturing. September was not a good month for global growth even though manufacturing generally improved.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief