Global| Sep 15 2016

Global| Sep 15 2016Euro Area Auto Registrations Flatten

Summary

Europe's passenger car registrations rose by 10.3% month-to-month after a 9.7% drop in July. The welcome bounce back leaves registrations higher by 9.7% year-over-year. The sequential growth rates for registrations are not very [...]

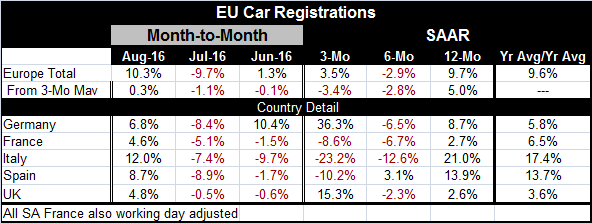

Europe's passenger car registrations rose by 10.3% month-to-month after a 9.7% drop in July. The welcome bounce back leaves registrations higher by 9.7% year-over-year. The sequential growth rates for registrations are not very illuminating about developing trends. The country level growth rates for activity are markedly different. France, Italy and Spain show sharp pullbacks in registrations over three months. For France and Italy, the pullback extends over six months as well. Italy and Spain still log substantial year-on-year gains while the U.K. and France have modest gains of about 2.5% over 12 months; Germany is stronger.

Europe's passenger car registrations rose by 10.3% month-to-month after a 9.7% drop in July. The welcome bounce back leaves registrations higher by 9.7% year-over-year. The sequential growth rates for registrations are not very illuminating about developing trends. The country level growth rates for activity are markedly different. France, Italy and Spain show sharp pullbacks in registrations over three months. For France and Italy, the pullback extends over six months as well. Italy and Spain still log substantial year-on-year gains while the U.K. and France have modest gains of about 2.5% over 12 months; Germany is stronger.

The averages data which looks at the last 12 months of registrations over the previous 12 months is a more lagging and stable calculation, but it also shows wide differences among these EU member countries with Italy and Spain the relative strongest and Germany, France and the U.K. at more modest levels of gains.

The chart may be the most telling, however. It shows that retail sales volumes continue to move higher and are still advancing nicely in recent data. But it also shows that auto registrations have been moving sideways with some volatility for some months. The chart, which is a less familiar one, plots the levels of the variables instead of growth rates. But in this form, it illuminates the trends at least in this situation much better. We can see that because of the choppiness why calculations over various short-term horizons might be unstable. We can also see that despite the sharp year-over-year gain registrations have been `moving sideways' since peaking in the December to February period of this year. Year-on-year calculations are still elevated because sales currently are higher than they were prior to December. But unless registrations step up their pace, there will be no year-on-year growth as we get to the end of the 2016.

This pattern of auto registrations mirrors the performance in the U.S. where Ford is already on record as saying that auto sales have passed their peak. A number of factors in the post financial crisis period have given vehicle sales and registrations a boost, factors ranging from an aging fleet on the road, demographics, the liberal use of subprime credit (even when it was not being used elsewhere-as in housing), sporadic government support programs, lower fuel costs and a shift up in demand by consumers eager to get the newest technology in their vehicles at a time that that automotive technology has been changing fast.

In yesterday's report, I flagged the weakness in capital goods output (euro area industrial production report) as a potential issue. Here again it's important to see the potential consequence of slowing auto sales in tandem with capital goods output lethargy. If both these sector in Europe go flat at the same time, it could be a lethal blow to European growth. Global trade is still weak so there is little chance of replacing failing domestic demand with exports. We do see one bright spot here: that despite the flatness in vehicle registrations, retail sales volumes are continuing to power ahead. That's the good news. For now there may not be much risk to growth. But whether there is or isn't a threat seems to depend very importantly on non-auto retail spending. And retailing has been a strong sector in this recovery period in Europe. But in the broad EU and EMU targeted European Commission index framework, there has been slowing in retailing in recent months. We should keep a very close eye on European growth data and not just the factory reports which have been weak for some time. There does seem to be a thinner reed that growth is clinging to at the moment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief