Global| Aug 30 2016

Global| Aug 30 2016Euro Area and EU Indices Fall; No Longer Firm Readings- Be Afraid?

Summary

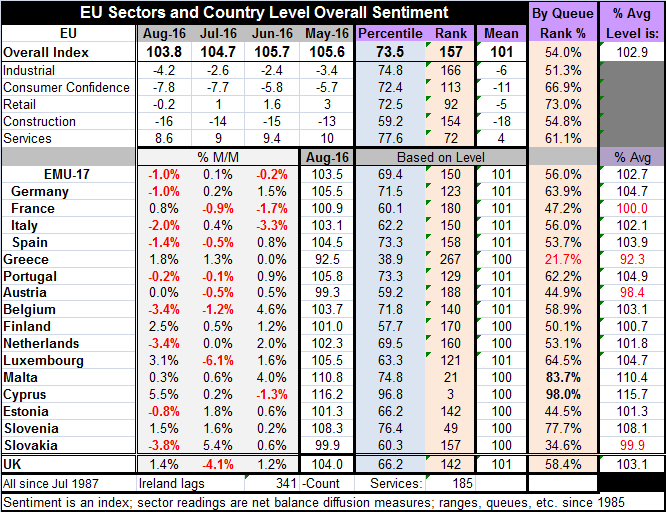

The EU Commission indices for the EU and EMU fell hard in August. Their slippages have been ongoing. There are no more truly `strong sectors' in the EU, but the EMU is faring slightly better on that front. The strength in services and [...]

The EU Commission indices for the EU and EMU fell hard in August. Their slippages have been ongoing. There are no more truly `strong sectors' in the EU, but the EMU is faring slightly better on that front. The strength in services and in retail has evaporated. The Big Four economics have very middling rankings in their historic queues of data. There is no `strong' economy anymore. And do not -NOT- blame it on Brexit. The slippage dates from a peak reading in December 2015 of 108.5 for the EU and a peak reading of 106.6 for the EMU at the same time. Europe is eight months into this new cycle of slippage. And these recent cycle `peaks' compare to pre-recession and pre-financial crisis readings of 114.5 for the EU and 113.2 for the EMU (both May 2007).

The EU Commission indices for the EU and EMU fell hard in August. Their slippages have been ongoing. There are no more truly `strong sectors' in the EU, but the EMU is faring slightly better on that front. The strength in services and in retail has evaporated. The Big Four economics have very middling rankings in their historic queues of data. There is no `strong' economy anymore. And do not -NOT- blame it on Brexit. The slippage dates from a peak reading in December 2015 of 108.5 for the EU and a peak reading of 106.6 for the EMU at the same time. Europe is eight months into this new cycle of slippage. And these recent cycle `peaks' compare to pre-recession and pre-financial crisis readings of 114.5 for the EU and 113.2 for the EMU (both May 2007).

Since the sentiment indices for the EU and EMU peaked, the EMU has fallen by 3.1 points with Germany falling by 1.3 points, France shedding 1.1 points, Italy losing a whopping 6.1 points and Spain dropping fully 7.4 points. On this same horizon, the U.K., which has gone through trial by Brexit, has lost 6.1 points from its overall sentiment gauge.

Eight of 16 reporting EMU members have seen their economic sentiment indices fall in August; of these eight, six have drops of one percentage point or more.

Sector ranking

The EU sector performance is poor with slippage across the board on all five measures. Four measures the industrial sector, consumer confidence, retailing and construction now have outright negative readings. Only services still has a positive diffusion score (up minus down net). The overall EU sentiment gauge has a 54th percentile queue standing while the EMU's gauge has a 56th percentile standing. The queue percentiles have their median scores at a level of 50 by construction. Their rankings tell us where this month's index sits in an ordered queue of data. For example, the EU index is lower about 54% of the time and higher about 46% of the time. Its reading is a decidedly neutral reading; the same is true of the EMU. The strongest EU sector on this relative scale is retailing at a 73rd percentile standing followed by consumer confidence at a 66th percentile standing and by services at a 61st percentile standing. The industrial standing is barely above its median with a 51st percentile standing; construction has a 54th percentile standing. The EU sector mantra in August is mediocrity.

Sector raw scores

Let me be clear about why I prefer the queue standings to evaluate these data. The raw diffusion scores show you what the sectors are doing in absolute terms. The raw score ordering is (1) services, (2) retailing, (3) industrial, (4) consumer confidence and (5) construction. This is different from the ranking based on queue values (retailing, consumer confidence, services, construction, and industrial). I prefer the queue rankings because they normalize each sector for its usual performance -and sector wide norms are extravagantly different. What we see in evaluating sectors (or countries) by queue standings is how each measure is doing relative to its own historic norm. That permits us to compare across sectors as well...which index is doing relatively better than it usually does? For example, consumer confidence has negative raw-score readings 97% of the time. Construction is negative 90% of the time. But the services sector is only negative 15 % of the time. Clearly, there is something idiosyncratic about each sector's evaluation that makes each sector not directly comparable to other sectors. This means that the relative scores of queue standings give us a better gauge for comparisons and useful context in a simple scalar value. Services, construction and industrial sectors are the most volatile by standard deviation measures with services and construction the most volatile by a good measure. Also services takes on values ranging over 63 integer values, compared to a range of 49 for construction, 45 for the industrial sector, 35 for retailing, and 34 for consumer confidence.

Country rankings

If we rank all of the countries in their respective historic queues then take the standard deviation of these rankings and average the result over one year, we find that the current smoothed rankings have some the lowest dispersions we have since late 1990 (lower only in 2007 and 1995). This means that most EMU countries are in the same phase of their respective business cycles and usually that is bad news. Cycles tend to be the most synchronized at the bottom of a cycle.

The EMU has a 56th percentile ranking with Germany, among the Big Four economies, with the highest percentile ranking at its 63rd percentile. There are not many countries with extremely low rankings. The unweighted country average ranking is in the 57th percentile, not too far for the EMU (weighted) gauge at 56%.

EMU sectors

In the EMU, the services sector has a 74th percentile standing with Germany at an 83rd percentile standing and having the strongest relative services reading among the Big Four EMU economies. France at the 53rd percentile has the weakest service sector score. Retailing in the EMU has an 84th percentile standing, much better than the standing for all of the EU. Spain has the highest percentile standing at a 93rd percentile with France at the lowest in its 57th percentile. Consumer confidence has an EMU-wide standing in its 74th percentile (also better than in the EU) with Spain having the strongest reading among the Big Four economics and Italy at a 68th percentile having the lowest. The consumer confidence rankings are more tightly clustered and at uniformly higher levels than for most other sectors. The industrial sector has a 58th percentile standing in the EMU, also a little better than for the EU, with Germany having the top standing among the Big Four economies (although at a very modest level) at its 57th percentile; both France and Italy show standings in their respective 45th percentiles below their median values. Spain at 51 is just a tick above its median value. The industrial sector is hurting in the EMU as well as globally and the weak euro has not helped it all that much. For the EMU, construction is at its 53rd percentile standing. Among the Big Four, Germany's 99th percentile reading is clearly the relative strongest with Spain's 15th percentile standing the lowest. France is at its 36th percentile, well below its median. Clearly, Spain's construction sector bust is very slow in recovering.

Summing up

There is a lot of weakness in the EU area in August. Both the EU and EMU are showing withering readings and losing momentum on a broad-based front. Indications of a more synchronized cycle raise a warning flag of sorts, but the individual country measures are still clustering above their respective medians. There is no disaster, but there is fellowship in mediocrity and slippage. That is worrisome enough, especially with ECB policy showing no signs of generating traction.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.