Global| Jan 30 2014

Global| Jan 30 2014EU Sentiment Tails as EMU Sentiment Rises

Summary

In January the overall sentiment indicator for the European Union (EU) fell while sentiment indicator for the European Monetary Union (EMU) rose. Still, in the monetary union there were numbers of countries that saw setbacks to their [...]

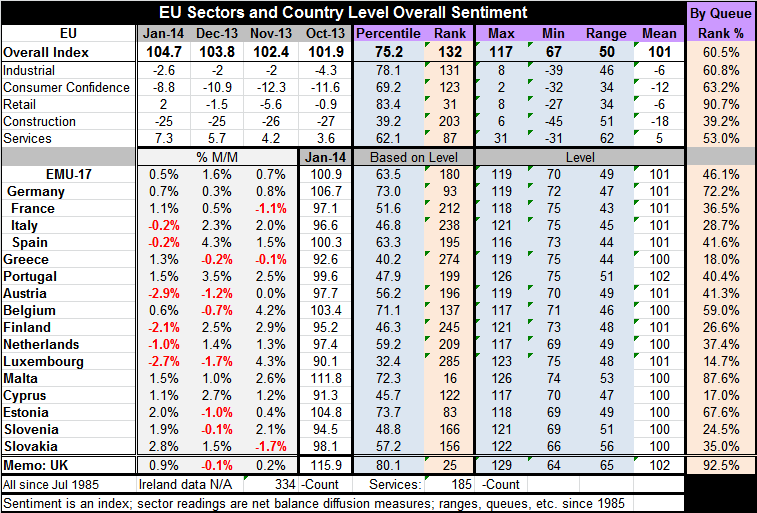

In January the overall sentiment indicator for the European Union (EU) fell while sentiment indicator for the European Monetary Union (EMU) rose. Still, in the monetary union there were numbers of countries that saw setbacks to their sentiment. The largest monthly setback came in Austria with the index falling by 2.9%. In Luxembourg the index fell by 2.7%. In Finland index fell by 2.1%. After that, there were declines of 1% in the Netherlands and 0.2% in Spain as well as in Italy.

In January the overall sentiment indicator for the European Union (EU) fell while sentiment indicator for the European Monetary Union (EMU) rose. Still, in the monetary union there were numbers of countries that saw setbacks to their sentiment. The largest monthly setback came in Austria with the index falling by 2.9%. In Luxembourg the index fell by 2.7%. In Finland index fell by 2.1%. After that, there were declines of 1% in the Netherlands and 0.2% in Spain as well as in Italy.

In terms of the levels of the indices for the EU and the EMU regions, the EU is actually stronger as it sits in the 60th percentile of its historic queue compared to the index for the EMU which sits only in the 46th percentile of its historic queue.

Both the EU and the EMU have a long way to go to get to index levels that are comfortably strong or firm. The current levels, particularly for the EMU, are disappointing.

Turning to the sectors, in January the EU aggregate shows a decline in the industrial sector that is slightly larger than it was in December. We find declines in construction; that metric is the same as it was in December. Consumer confidence is declining slightly less than it was in December. Making gains are the retail sector, with a positive reading up to +2.0 from -1.5 in December and Services at a rather firm-looking at 7.3 reading in January, up from 5.7 in December.

We evaluate the levels of the various sectors according to their respective queue standings. Retailing leads the way by a long shot standing in the 90th percentile of its historic queue of values. In second place would be consumer confidence in the 63rd percentile. After that, the industrial sectors rank in the 60th percentile. Services, despite their stronger-seeming level, are still only in the 53rd percentile of their historic queue. Construction is at the 39th percentile of its historic queue. Only retailing right now is strong. Consumer confidence and the industrial sector are in the 60th percentile range which makes them moderately disappointing but not necessarily weak. The construction sector has not been in a good number for long time and the minus-25 reading, although weak historically, actually reflects some improvement. While services are showing gains, that sector is lagging on a historic basis.

Looking closely at the industry ranking, for the EMU grouping, the queue standing is in the 60th percentile without any particular strong components. The strongest component is employment expectations which is in the 71st percentile of its historic queue. After that, it's export orders which stand in the 57th percentile of their historic queue. If we look at the large countries, Germany has its industrial sentiment indicator in the 74th percentile of its historic queue; it is surpassed by the UK which is not a single currency member; its reading is in the 94th percentile. France's indicator is in the 53rd percentile while Italy and Spain lag with indicators below their respective 40th percentiles.

Consumer confidence in the EMU sits at the 55th percentile of its historic queue. Data for the economic situation over the next 12 months is evaluated in the 72nd percentile of its historic queue and while that is a good ranking, the economic situation over the past 12 months was evaluated as higher, at the 84th percentile of its historic queue. The ability to make major purchases now has a response in the 62nd percentile of its historic queue. Meanwhile, forward-looking the major purchase index is in the lower 15th percentile of its historic queue, a very weak reading. Unemployment expectations fell to 25 from 29. This is an improvement in January compared to December. The January standing is in the 46 percentile of its historic queue, making some progress but it remains pretty close to the middle of the pack in terms of historic readings. On balance, consumer confidence does not appear to have made great strides. There continues to be this divergence within the monetary union with the German figure in the 77th percentile of its historic queue compared to France in the 37th percentile, Italy in the 39th percentile and Spain in the 48th percentile. Portugal has a confidence index in the lower 42nd percentile of its historic queue while Greece is in the lower 16th percentile. By comparison the UK, an economy that has been doing very well, has its consumer confidence reading in the top 8% of its historic queue, a very strong reading.

EU metrics provide readings on a number of different sectors and aspects of the Union. We can look at data for the whole of the European Union or just for the Monetary Union portion. However, when we look at it closely, it is clear that there is a great deal of variation and many differences in momentum among various EU and EMU members. Of course, there is a strong overlap between those two groups. While the EU index shows that there is some backtracking, the EMU index shows that conditions are still advancing. On balance, I think we should be wary of the variation within the Union as well as of the variation among the various key economic sectors. On the whole, the EU and the EMU appear to be making progress. But the progress is slow; it is not monotonic. There are great differences in the way sectors and countries share in the progress of these various economic units.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.